Contract Surety Bonds are underwritten on the “3Cs”. What does that mean and how understanding the “3Cs” can make it easier for contractors to obtain construction surety bonds.

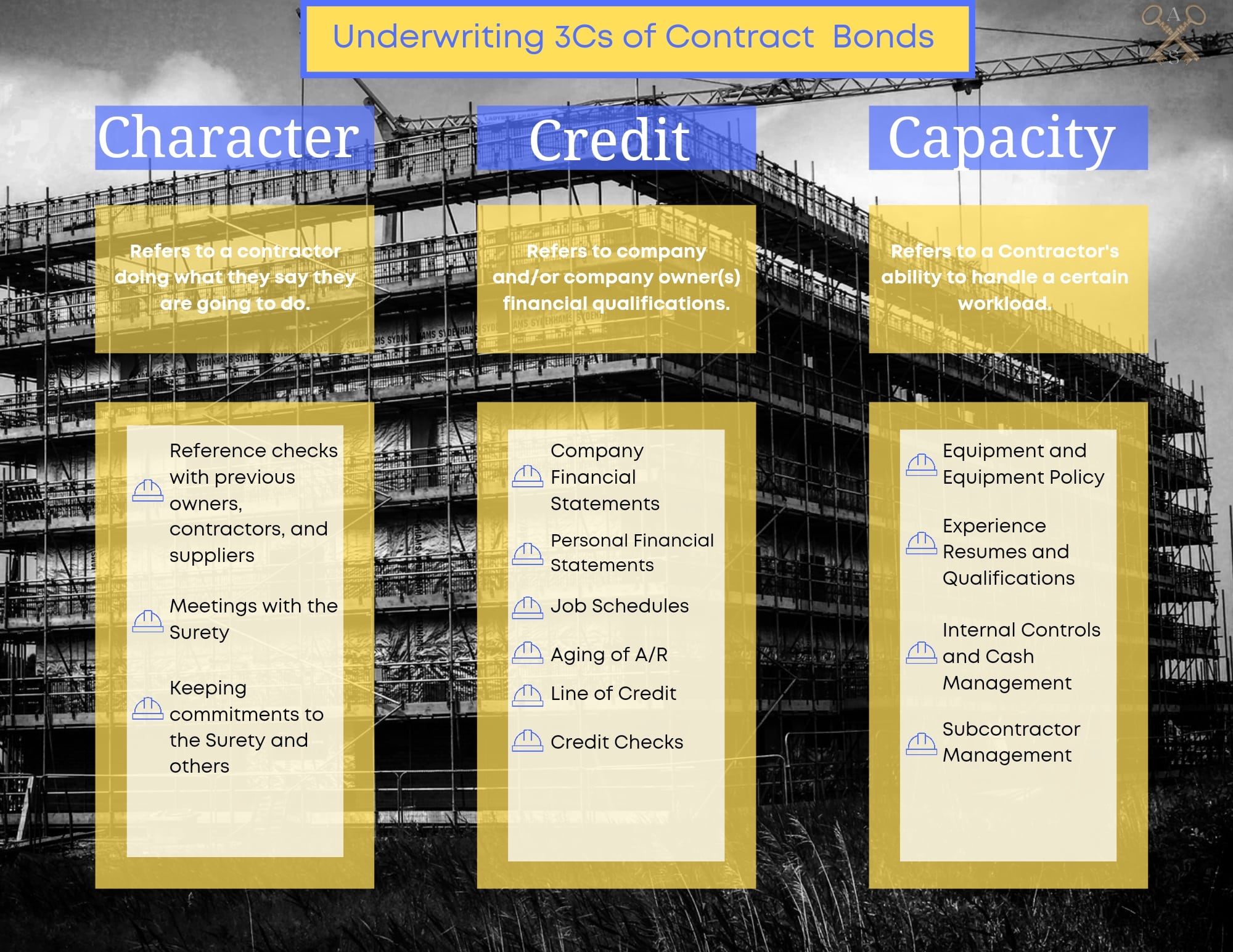

The 3Cs are an acronym for Character, Credit, and Capacity. Together they make up the three distinct categories that contract Surety bond underwriters look at before issuing bonds such as bid bonds, Performance Bonds and payment bonds.

Character in bond underwriting refers to a contractor doing what they say they are going to do. Many underwriters will tell you that Character is the most important aspect of the 3Cs. After all, a bond underwriter wants to know that a contractor will complete their obligation and fulfill their commitment to reimburse the bond company if they cannot. No amount of money can make up for bad character.

Character may also be the most difficult of the 3Cs to underwrite. Surety bond underwriters judge Character in a number of ways. They may contact contractors, owners and suppliers the contractor has worked with in the past. The underwriter is trying to see how the contractor deals with others to get an indication on how they may deal with the Surety and the other parties on projects they may bond.

Another way that surety bond companies underwrite character is by having annual meetings with the Contractor’s owners and key people. An underwriting meeting is important for a surety bond company to hear about a contractor’s background and plans. It also gives the Surety a chance to set expectations. A contractor that upholds its commitments is considered to have good character while the opposite can also be true.

An example of this would be if a contractor commits to providing timely financial statements or obtaining bonds from Subcontractors, and does not do so, it could be looked at negatively by a surety bond company.

Credit in surety bond underwriting refers to company and/or company owner(s) financial qualifications. Surety bond companies look at many items to assess a company’s credit.

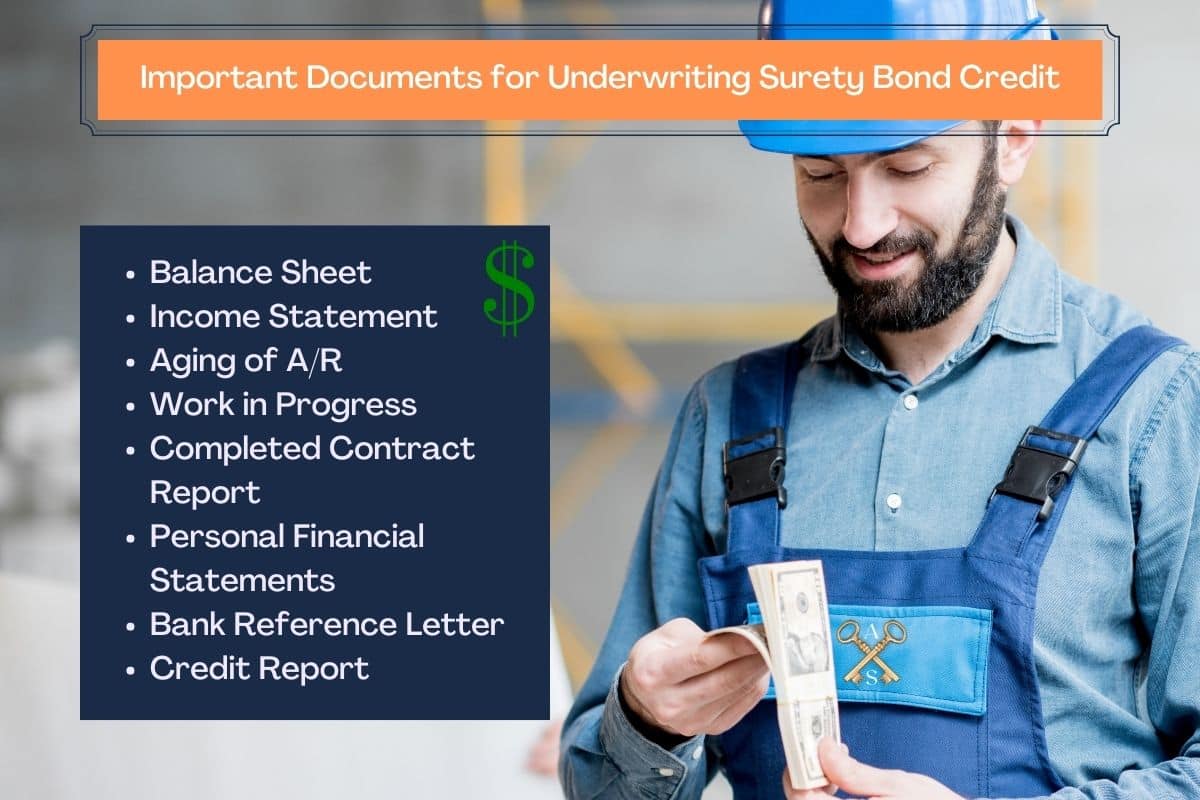

Contract Surety Bond companies usually want to see the company’s most recent three years of financial statements. Depending on the size of bond Capacity desired, these statements usually need to be CPA prepared. The Surety is looking for statements that include a balance sheet, income statement, statement of cash flows, work in progress schedule, completed contract schedule, and notes to the financial statements. Additionally, the bond company will want to see an aging of accounts receivables. You can read more about financial statements for Surety bonds here.

The Surety bond company is very interested in the company’s balance sheet. They want to see how much liquidity a company has. This is often measured through a company’s working capital. They are also very interested in a company’s net worth. A Surety wants to see how much debt a contractor has and normally wants to see debt much less than 4 to 1 when measured against net worth.

Other things Bond underwriters look for on a balance sheet are a company’s fixed assets and their depreciation, inventory and related party transactions.

Finally, a balance sheet shows the Surety company how much money a company has retained.

A Contractor’s income statement shows the Surety underwriter if a contractor is profitable. Underwriters are also interested in the company’s general and administrative expenses (also referred to overhead). Knowing a Contractor’s historical overhead can give insight into how much work a contractor will need to obtain to be profitable in the future.

A Contractor’s job schedules are another valuable tool for Surety bond companies to underwrite a contractor’s credit. Underwriters look at these schedules for trends. Do projects maintain the expected gross profit, or do they tend to fade? An underwriter can also see if a project is headed for problems and if a contractor needs more work. You can read more about how surety bond underwriters look at Work in Progress Reports here.

Surety underwriters look at an Aging of Account Receivables to determine if Receivables are collectible and if there are any potential problems. Old Receivables are harder to collect, and surety bond companies exclude Receivables 90 days and older from their analysis. The exception to this rule is retainage, but contractors need to be able to separate that in their aging reports.

Another valuable tool for underwriting credit is personal financial statements on company owner(s). These give insights into what resources may be available to the contractor if the business needs it.

Personal Financial Statements also give surety bond underwriters insight into what the owner(s) need to take out of the business to cover personal expenses. The larger the personal expenses, the more pressure on the business to generate profits to cover those expenses.

Surety Bond companies also use credit reports to determine a contractor’s bond credit. These reports are mostly used to see if there are liens, judgments, or litigation that impact the credit decision.

Capacity in surety bond underwriting refers to a contractor’s ability to handle a certain workload. To evaluate Capacity, a surety bond company commonly looks at the following:

A Contractor’s Equipment and equipment policy is a key consideration. Does the contractor have the necessary equipment for their workload? Will they have to buy or rent additional equipment? All of these factors into how much work a contractor can handle.

Another consideration for Capacity is the Contractor’s people and their experience. Do they have enough supervision to handle a certain workload? Do those people have experience on large projects or in a specialized sector?

Internal controls and reporting are one of the most important and often overlooked factors in underwriting capacity. Managing bigger workloads involves more cash management. Surety underwriters want to make sure Contractors have sophisticated systems and practices in place to track cash, project performance and financial reporting. Contractor’s without such systems may have their capacity limited.

Subcontractor default poses a major risk for most contractors. The bigger workload, the bigger the risk. Surety underwriters want to make sure that Contractors have a Subcontractor management plan. Usually this includes getting Subcontractor bonds or Subcontractor Default Insurance for some of their Subcontractors.

There are even more details that go into the 3Cs of Contract Surety Bond Underwriting. However, having an understanding of what bond companies look for can help contractors make themselves more bondable. You can also view our surety bond FAQs to learn more. Contact us anytime

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.