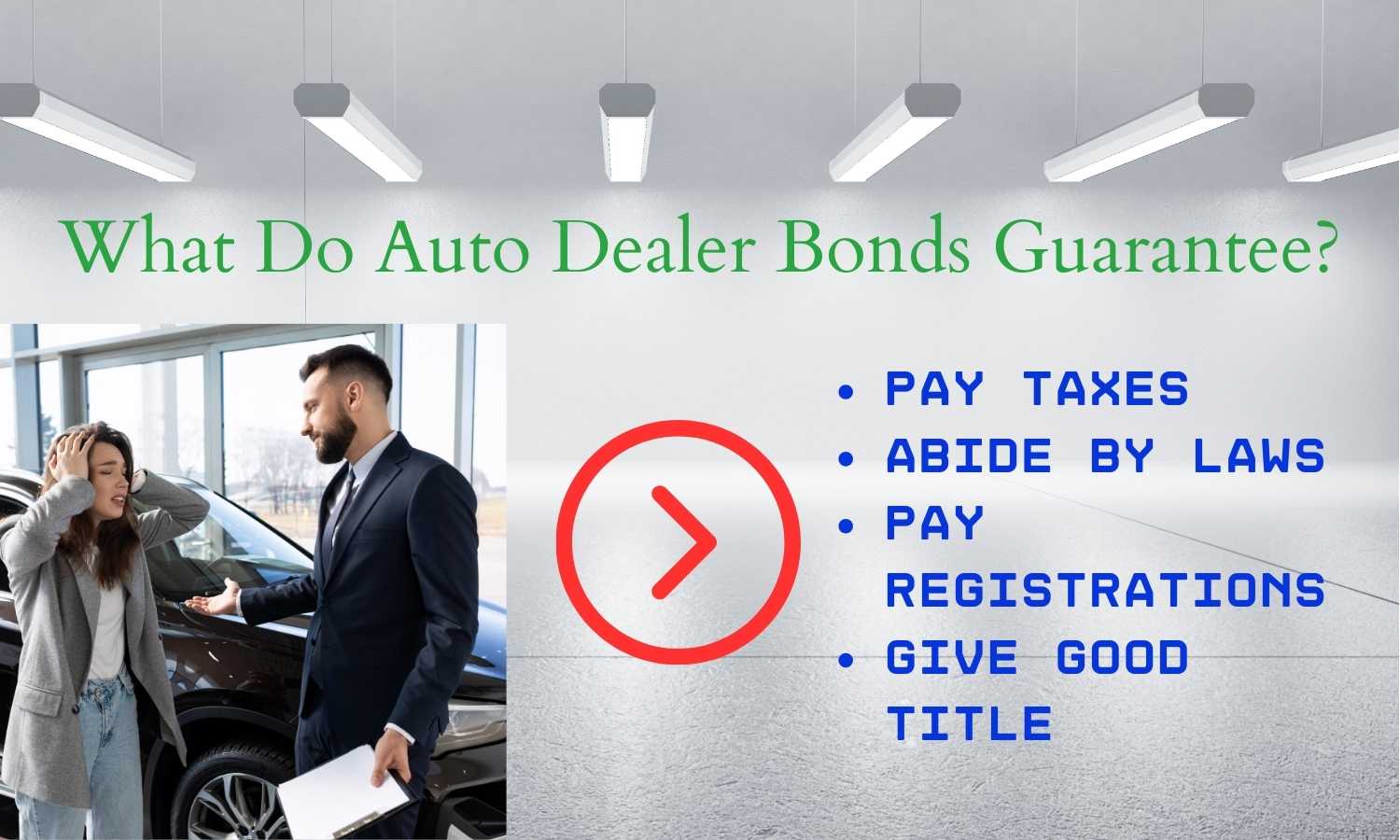

Auto Dealer Bonds are a requirement in many states in order to become and remain a licensed auto dealer. Learn more about what these bonds guarantee, how to get one and how much they cost.

An Auto Dealer Bond is a type of license surety bond for auto dealers. These bonds guarantee that an auto dealer will follow local laws, act in an ethical and fair manner, and handle down payments, taxes and registration fees appropriately. Should an auto dealer not comply, a claim could be made against the Auto Dealer Bond. These bonds are also called Motor Vehicle Dealer Bonds, and Car Dealer Bonds as well.

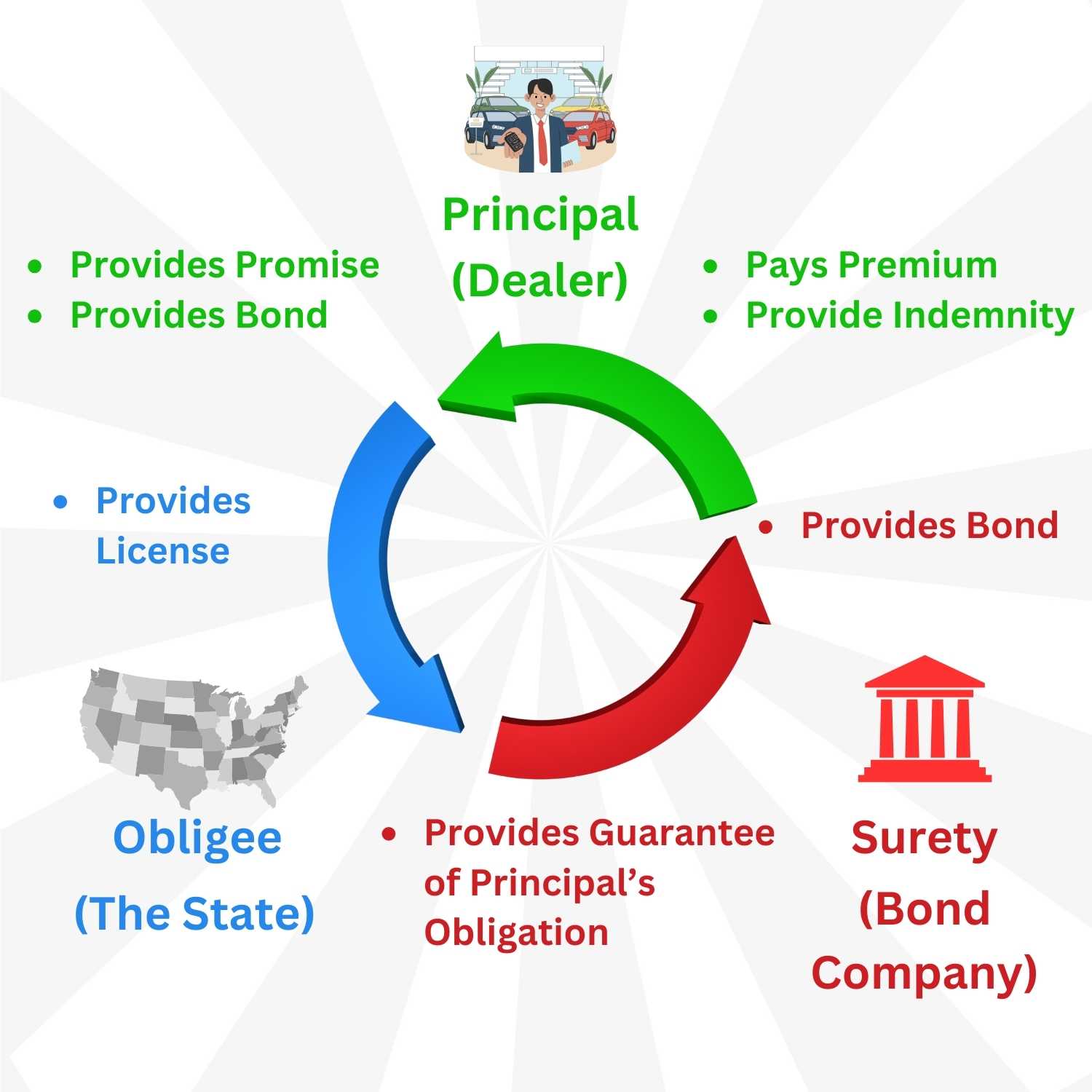

An Auto Dealer known as the principal pays a fee to Surety Bond Company. In return, the Surety Bond Company provides a financial guarantee to a State, Municipality or other jurisdiction, referred to as the obligee, that the Auto Dealer will comply with the laws and regulations of that State or jurisdiction. Should the Auto Dealer not comply, a claim can usually be made with the State, jurisdiction or directly with the Surety Bond Company.

A surety bond for an auto dealer is a type of financial guarantee that is designed to protect consumers from any fraudulent or dishonest practices that an auto dealer may engage in. The surety bond is a form of protection for the consumer in the event that the auto dealer fails to fulfill their obligations as outlined in their contract with the consumer.

Most states require businesses selling vehicles to consumers to provide Auto Dealer Bonds. Many states require bonds for both new vehicle dealers and used vehicle dealers. Some states also require dealers of specialty vehicles such as heavy equipment and trucks to provide vehicle dealers bonds as well. Check your state requirements or with our experts to determine if your dealership needs to be bonded.

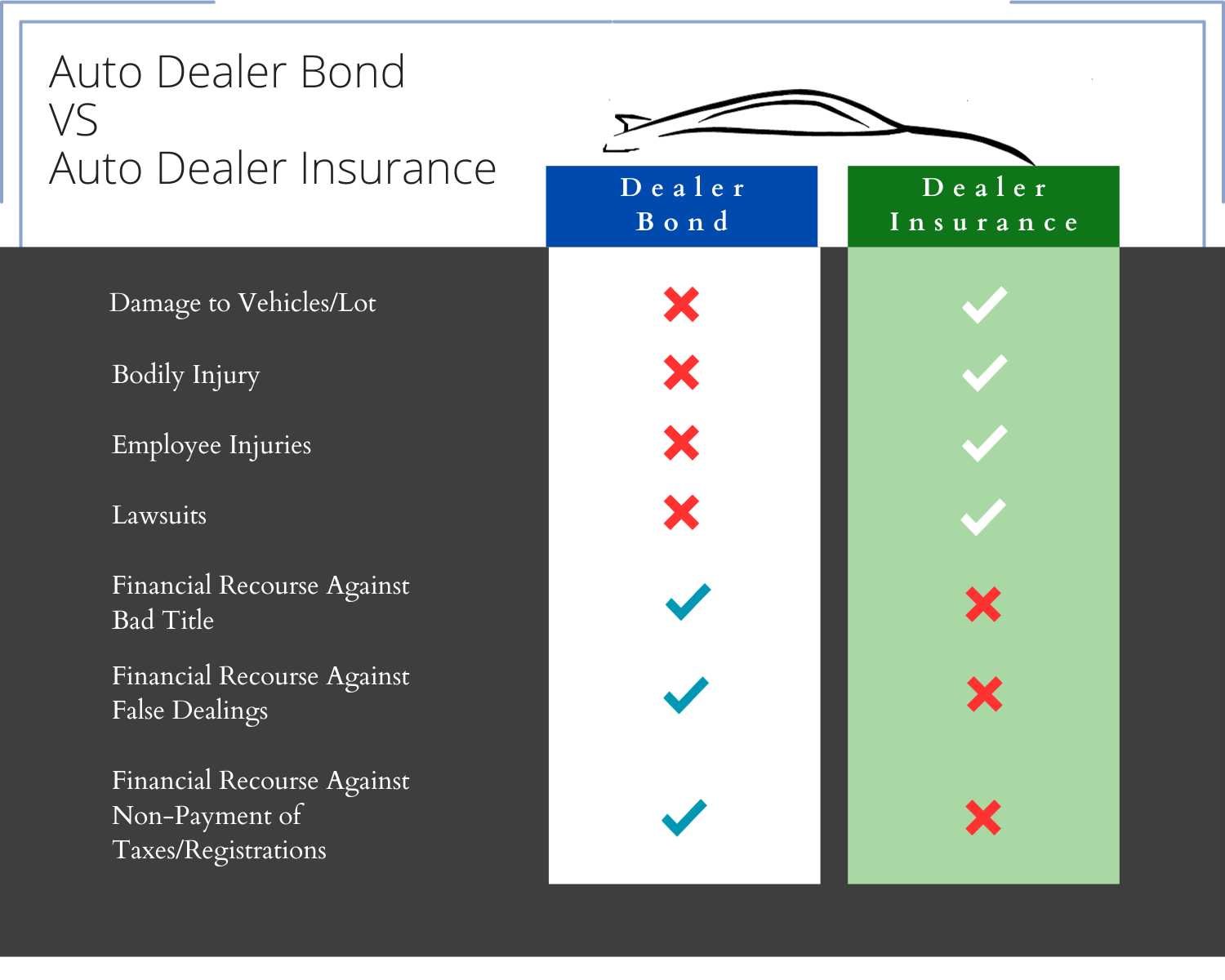

Auto dealers typically need both auto dealer bonds and auto dealer insurance. However, these are two very different products that dealerships should understand.

Auto Dealer Insurance is a type of property and casualty insurance that covers things like property damage, bodily injury, workers compensation and other damages caused by the dealership and their employees. This insurance is two party coverage. The dealer pays the insurance company, and the insurance company pays losses caused by dealership. If a loss occurs, the dealership is generally only responsible for a deductible and possibly coinsurance. Common Auto Dealership Insurance Coverages are below:

Open Lot Coverage provides protection to the dealer's vehicles, whether they are on the lot, loaned out, or driven by potential buyers. Open lot coverage is important since many vehicles may be stored outside and exposed to damage against things such as wind, hail, and theft.

General Liability insurance protects the dealership against property damage and injuries to other parties. For example, a customer slips and falls on the showroom floor. If they are injured and sue the dealership, this would be covered under the general liability policy.

This coverage is required by most states and provides coverage to workers that may be injured on the job while working for the dealership.

Many dealerships have garage operations and will need this coverage. It covers damage to customer vehicles, injuries and other damages while the vehicle in in the dealer's garage being serviced or getting repairs.

Alternatively, Auto Dealer Bonds are a three-party contract. They are written between the dealer and surety bond company, but it is the state that is the beneficiary. The state does this so that an affected customer does not have to go through the legal process. They can simply make a claim against the bond. Unlike insurance, a bond is more of a credit product. Instead of being responsible for only a deductible, the dealer will be required to reimburse the surety bond company for the entire amount of the claim.

Because of the way these products are handled, they can be priced accordingly. For example, insurance assumes that the dealership will have some losses according to industry averages, and those expected losses are priced into the dealer's insurance cost. Alternatively, because bond assume no losses, they can be priced accordingly. Pricing losses into dealer bonds would make them more expensive. You can read more about the differences between surety bonds and insurance here.

Auto Dealer Bond claims are rare, but they do happen. Claim handling depends on the State where the Auto Dealer is located. Some States have claimants file a complaint with the State first and then the State makes a claim against the surety bond. Other States allow the claimant to file a claim directly with the surety bond company.

In either case, the surety bond company must investigate the claim to make sure it is valid. If the claim is valid, the surety bond company will be required to make a payment. However, the surety bond company will then seek reimbursement from the Auto Dealer under the Indemnity Agreement.

Motor Vehicle Dealer Bond premium amounts vary by state. Some States may only require dealers to provide a $25,000 bond while others such as New York may require as much as $100,000.

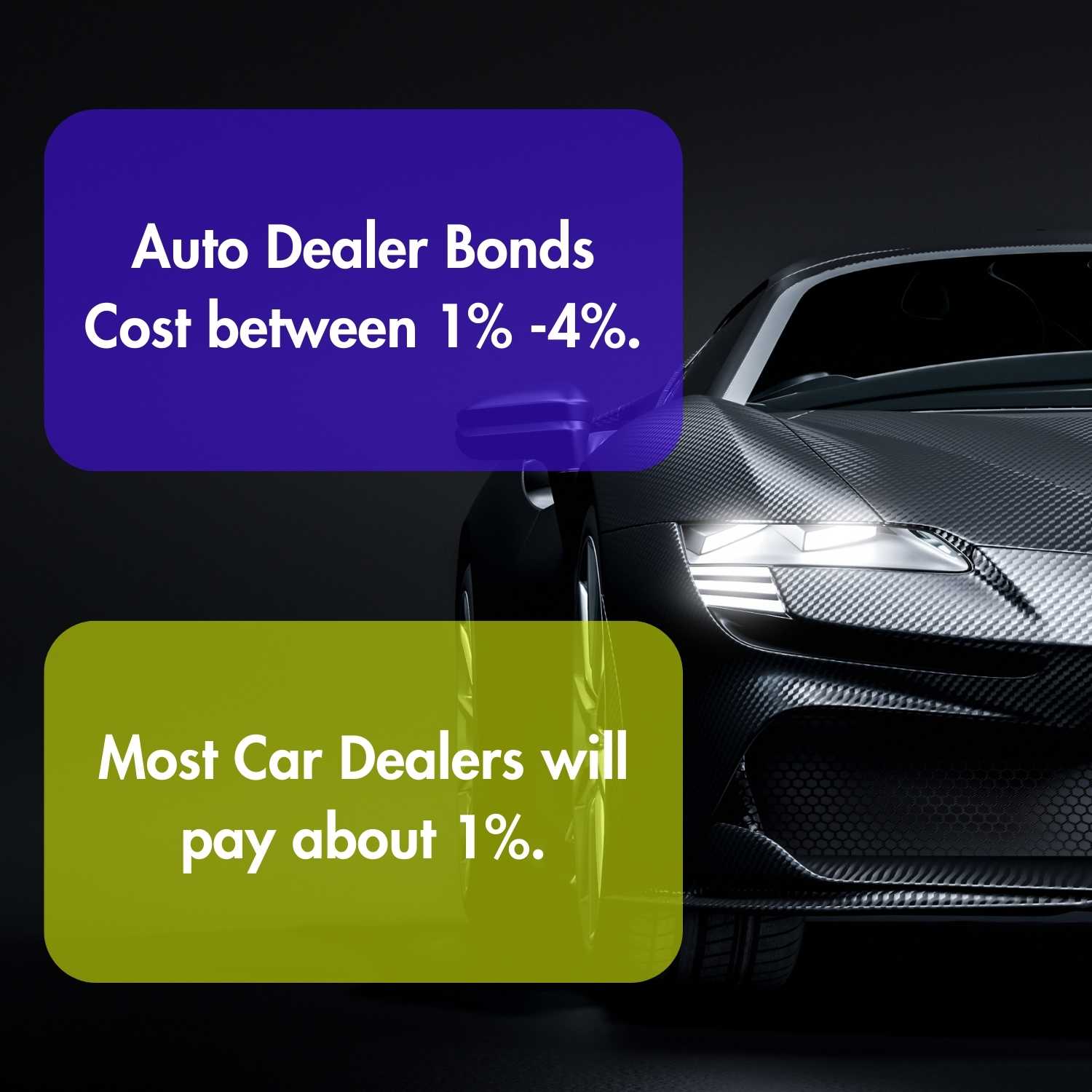

The cost of the bond depends on the credit, financial strength and history of the Auto Dealership. Dealerships with strong financial strength and a long history of compliance may pay less than 1% of the bond amount per year. However, a dealership with poor credit, financial strength or a history of claims and complaints could pay as much as 4% of the bond amount per year. Most dealerships will pay about 1% of the bond amount each year that the Auto Dealer Bond remains in place.

Most auto dealers can purchase bonds online instantly with just a credit check. Simply search for the bond by State here. However, the best terms and pricing usually require an Auto Dealer to submit company financial statements and an application for review. Most auto dealers have no trouble qualifying for these surety bonds.

Some States allow auto dealers to post cash, CDs or Irrevocable Letters of Credit (ILOCs) instead of a surety bond. The advantages to these alternative instruments may be cost. However, they all tie up assets that cannot be used in the auto dealer’s business. They also offer little to no protection if a claim is made. Learn more about surety bonds versus ILOCs and Cash by clicking on the images

Auto Dealer Bonds are easy to obtain and do not tie up a dealership’s financial resources like other alternatives. Most dealerships can purchase these bonds instantly and at low cost.

Click on the State Below to Learn More About Auto Dealer Bonds in that State:

Indiana

Iowa

Kansas

Kentucky

Louisiana

Maine

Maryland

Massachusetts

Michigan

Minnesota

Mississippi

Missouri

Montana

Nebraska

Nevada

New Hampshire

New Jersey

New Mexico

North Dakota

Ohio

Oklahoma

Oregon

Pennsylvania

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.