Performance Bonds can be challenging for contractors in certain situations. These can be related to the contractor, the project or even both. Learn what makes a Performance Bond challenging to get and options for obtaining them anyway.

Performance Bonds can be difficult to write when a contractor has had challenges. Some of these common challenges are below.

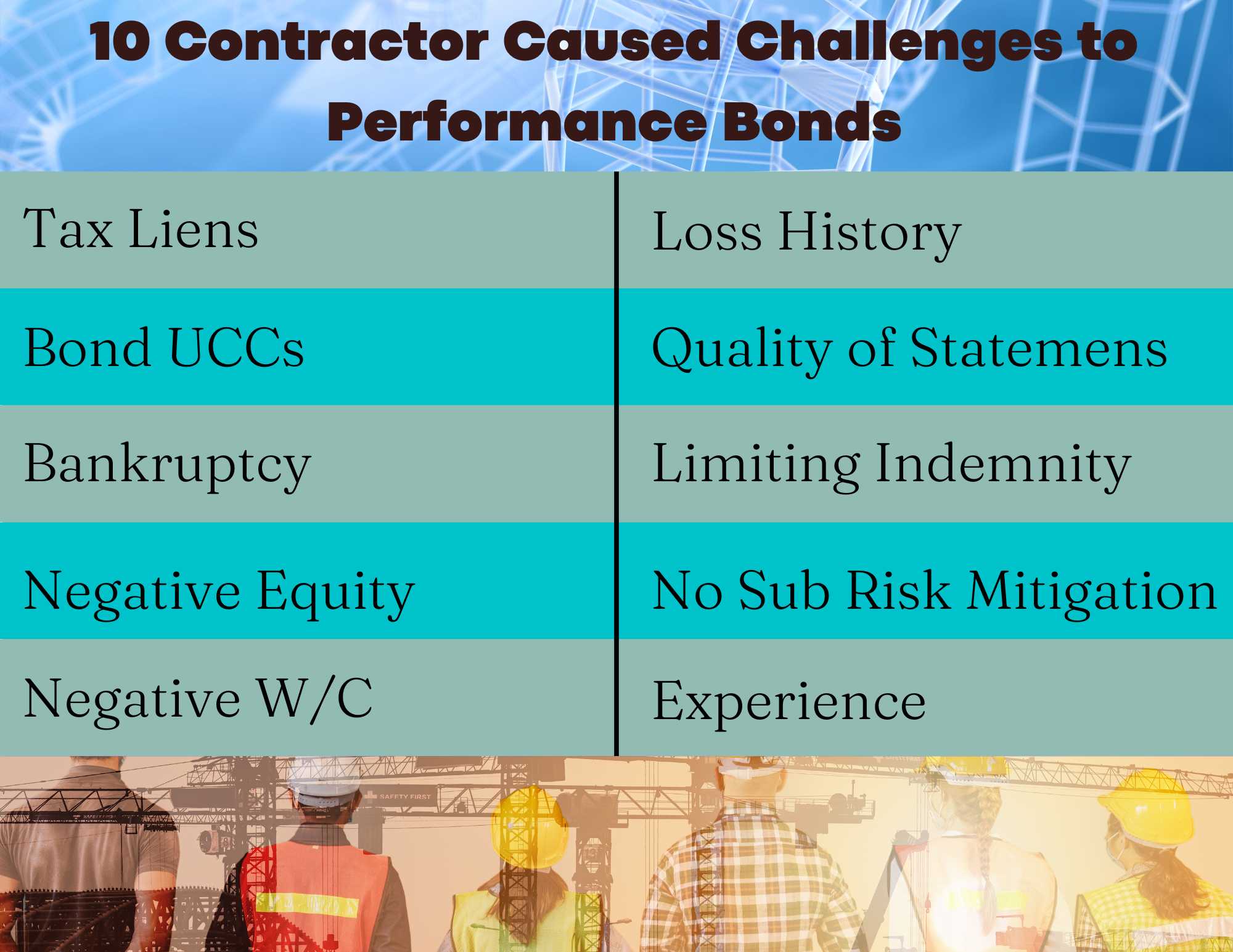

Contractors with tax liens provide one of the biggest challenges to getting performance bonds. Tax liens are caused by a failure to pay taxes owed to a government entity. Tax liens can be filed against a business, a person or both.

Tax liens create problems for surety bond companies and other creditors. When the government files a tax lien, they take a priority financial interest over other creditors. This means that a surety bond company will not have access to a Principal’s assets unless the lien is satisfied first. For this reason most surety bond companies will not provide Performance Bonds to Principal’s with tax liens.

Generally, in order to obtain any type of bonding, a payment plan must first be put in place with the IRS or government entity or the lien must be paid off. Should the lien be paid, most bond companies will consider writing bonds again.

If a payment plan is put in place, a contractor will likely still be required to use other tools to obtain a performance bond. Common tools include the SBA Surety Bond Guarantee Program, funds control, or collateral. The SBA Surety Bond program can be a great option. It allows the surety bond company to feel comfortable writing the performance bond and it is not visible to the Owner or Contractor (Obligee) requiring the bond.

In my experience, the second worst thing a contractor can have is a UCC Filing by a surety bond company. Contractors needing Performance Bonds should avoid this at all costs. A UCC Filing by a surety bond company generally means that the contractor owes the bond company money. This could be a claim in dispute, or it could be that the Surety Bond Company has paid a claim and is seeking reimbursement from the contractor.

Either situation is bad for the contractor needing a bond. I find that contractors are often surprised to learn that the surety bond company has made a filing that shows up on a credit report. Contractors need to understand that surety bonds are not insurance and claims will follow them.

A contractor with a UCC Filing by another surety bond company will find few options to obtain bonding. The reason is that the new bond company does not want to be in second position for a claim against the contractor’s assets. In other words, there may not be assets to satisfy both bond companies and the first surety bond company already has priority.

Generally, to obtain a performance bond, the contractor will need a very good explanation for why the filing has been in place. For example, a surety claim is in dispute. In this case, the contractor should be prepared to provide detail on the situation, the process and the expected outcome. Copies of legal filings will generally be required.

Even with a great explanation, the contractor should be prepared to provide collateral, and/or funds control to get a performance bond. There are not many other ways that the bond company can protect their interests.

Bankruptcies create challenges for surety bond companies and contractors needing Performance Bonds. Bankruptcies are legal proceedings for businesses and individuals who cannot pay their debts. These proceedings may allow them to discharge debts or create a structure more favorable to repaying them. Bankruptcies come in different forms. They can be Chapter 7 or 13 for individuals and Sole Proprietorships or they can be Chapter 7 or 11 for businesses.

A bankruptcy will show up on a credit report and background check for many years depending on the type of bankruptcy, even after it has been discharged. Contractors going through bankruptcy proceedings cannot get performance bonds without posting 100% collateral. However, once the bankruptcy has been closed (discharge) there are options. Contractors will still need to use tools such as the SBA Surety Bond Guarantee Program, funds control, or collateral for a period after the bankruptcy in most cases.

Once a bankruptcy has been removed from a contractor’s background and credit report, it will be easier to obtain bonding. However, most bond applications still require the contractor to disclose the bankruptcy. Although most will, some surety bond companies will not write performance bonds for contractors who have ever had a bankruptcy. They often cite statistics that say that bankruptcy filers are likely to declare bankruptcy again. However, current statistics show that only about 8% of bankruptcies filers declare a second time.

Equity is simply a company’s assets minus its liabilities. It is sometimes referred to as Book Value. Equity is an important calculation for creditors. A company with negative equity may have a difficult time paying their bills as they come due.

Performance Bond Companies take Equity a step further. They use Analyzed Equity instead. Analyzed Equity is the company’s equity once the bond underwriter has eliminated certain assets and liabilities. In their analysis, contract surety bond underwriters often remove items that are intangible such as Goodwill or Amortization. They also frequently remove items that may be difficult to collect such as Account Receivables over 90 days old and receivables from shareholders.

Negative Equity does not mean that a contractor is out of business or in liquidation. It just means that they may have little room for error. The company’s ability to continue will depend on future profits coming into the company. There are in fact very legitimate reasons for having negative equity. This is a common occurrence when a business sells or for ESOPs. Usually, the debt and Goodwill create negative analyzed equity.

The problem for surety bond companies is that this makes a business a difficult credit risk. Should a claim happen, there may not be enough tangible assets for the surety to get reimbursed for this reason, writing Performance Bonds for contractors with negative equity can be challenging.

The second reason surety bond companies struggle with negative equity is reinsurance. Reinsurance is insurance purchased by a surety bond company to mitigate their losses. Most reinsurance treaties specifically exclude contractors with negative analyzed equity. Therefore, if a bond company does write a performance bond for one of these contractors and suffers a loss, they will bear the entire loss.

Getting Performance with negative equity is challenging but not impossible. Depending on the situation, no additional terms may be required. For example, ESOPs and companies with solid histories of profitability may be able get performance bonds with no additional conditions. Still other companies may need to use tools such as SBA, Funds Control, or Collateral.

Working capital is a measure of a company’s ability to meet its short-term obligations. Working capital is current assets minus current liabilities. Working Capital is the primary consideration for most contract surety bond companies. Their belief is that contractors get in trouble when they run out of cash and liquidity. Therefore, a contractor with negative working capital will have a very difficult time obtaining performance bonds with these companies.

Contractors do have other options though. Some surety bond companies focus more on net worth and equity instead of working capital. These companies often write contractors with negative working capital if they have a strong equity position. This is especially useful for heavy equipment contractors. These contractors often use their working capital to purchase equipment so they can obtain and complete new work. Although these companies are often light on working capital, they may have significant equity in their equipment.

Other cases include contractors with significant paid off buildings and property. Although these assets may be depreciated, they often still contain significant value that an equity bond company can use to write performance bonds.

Every business needs to make money at some point on their operations. Surety Bond Companies carefully look at profitability trends for contractors. Contractors that lose money each year make it difficult to provide performance bonds. Bond companies are always concerned that these losses will continue.

Losses are not as much of a problem for contractors with very strong balance sheets compared to their bond needs. These contractors have a lot more flexibility when it comes to manufacturing losses. However, they are an issue for contractors that are stretching capacity. Contractors that are stretching capacity need to make money and keep money in the company. Surety Bond Companies frown on these contractors that manufacture losses to save on taxes. These contractors will find obtaining Performance Bonds difficult.

One of the most common reasons that surety bond companies will not write performance bonds is the contractor’s financial statement quality. Poor quality financial statements mean that a contractor does not have good systems in place. This means that they are more likely to not recognize issues until it is too late. Most contractors should be able to produce monthly or quarterly financial statements and schedules including a Work In Progress (WIP) report. These statements should include underbillings, overbillings and depreciation. Those numbers should also correctly tie to the WIP Report.

Having financial statements that do not correctly tie together will cause a surety bond company to lose confidence in the accuracy of the statements and the contractor. However, this is very common, even for large contractors. Contractors looking for performance bonds should invest in good financial reporting that they can produce on at least a quarterly basis. They will also likely need to invest in a CPA Reviewed Financial Statement for their year-end report.

Experience is important to contract surety bond companies. They want to know that the contractor has experience building projects of similar size and scope. Most surety bond companies will write Performance Bonds for contractors that are twice the size of their largest previously completed project. For example, if a contractor has completed a $2 million project, most bond companies will approve performance bonds for that contractor on a $4 million project. Some surety bond companies are comfortable writing performance bonds for projects as large as four times a contractor’s largest completed project.

Bigger projects require more cash management, more supervision, and more risk. The best way to qualify for a larger project is to mitigate this risk. This often means asking for subcontract bonds from subcontractors. It also means having a plan for supervision, material, labor, equipment and how to coordinate it. It also helps for a contractor to increase their cushion through a bigger bank line of credit to accommodate unforeseen issues.

Limiting Indemnity can make it difficult for a contractor to obtain Performance Bonds. Contractors understandably want to limit indemnity to as little as possible, while surety bond companies want as much as possible. When a contractor has a very strong balance sheet, it is common to remove them from personally indemnifying the bond company. However, a contractor with a smaller balance sheet may not be able to remove their personal indemnity and insisting on doing so can make getting performance bonds challenging.

Similar challenges occur when a contractor’s spouse refuses to indemnify. Other challenges occur when the contractor has ownership in different entities that will not indemnify. In both these situations, there will be concern from the bond company about shifting and sheltering assets. A better solution is to build the construction balance sheet to a point where the indemnity of shareholders or other entities is simply not needed.

Indemnity can also be an issue for contractors owned by Private Equity firms. Companies purchased by private equity often have negative equity. Additionally, the private equity firm and their owners usually will not indemnify. Usually collateral in an interest bearing or investment account is the way around this issue. More can be read about Private Equity Surety Bonds here.

For many General Contractors, subcontractors make up their biggest project risk. Therefore, contractors that do not protect themselves against subcontractor default can make it difficult to obtain Performance Bonds.

Consider a General Contractor performing a $10 million project. This project may very well have $9.5 millions of value subcontracted. A problem with any subcontractor could cause major delays, cost increases and delay damages. Issues could also cause a performance bond claim or even take the contractor out of business.

Surety Bond Companies want to see that contractors are protecting themselves from Subcontractor risk. There are several ways to do this including subcontractor bonds, Subcontractor Default Insurance, prequalification, joint checks, funds control, etc. The important thing is that a contractor has a process to reduce this risk. Without managing subcontractor risk, a contractor may find it difficult to obtain performance bonds.

Sometimes even the strongest contractors have challenges getting performance bonds when there are difficult project elements. Some of the most common project challenges are below.

Contractors are often surprised that surety bond companies are concerned with projects in different geographical locations. However, contractors often underestimate the risks associated with traveling. New geographies have different laws and customs. Contractors may not understand local labor and subcontractor operations. I have also seen contractors significantly misunderstand weather. In this scenario, the contractor underestimated how wet the ground remains and hit significant delays and damages.

Contractors going into a new geographic location should spend plenty of time researching the area before making the jump. Often, management from the area is a smart idea. They will know the local weather and labor situations. This will also make it easier to obtain performance bonds.

Like location, new scope of work can create challenges for obtaining performance bonds. For example, a General Contractor specializing in concrete building may want to get into wood frame to take advantage of industry trends. However, they often underestimate the challenges associated with doing so. Generally, different labor and different subcontractors specialize in each segment and there may not be much overlap. Scheduling is also dramatically different.

Contractors starting a new scope should go slowly and carefully. They should often hire or acquire someone with experience in that field. They should also meet with labor, material suppliers and competitors to learn the industry’s pitfalls. Finally, it would be wise to protect themselves against subcontractor issues until they get some experience with them.

New expertise can potentially be another challenge, even when it is in the contractor’s field of work. For example, a plumber who specializes in commercial buildings runs a big risk by bidding on a treatment plant project. Although both projects require expertise, one is certainly different from the other. Contractors will need to have a great explanation for the surety bond company in order to get performance bonds on these projects. Contractors should hire supervision, project management and labor with experience in this type of work. They should also start small to gain experience before bidding larger projects.

Performance Guarantees are a major red flag for surety bond companies. Performance guarantees promise a specific level of outlook, energy savings, etc. These guarantees can be common on solar and other energy projects. Performance Bonds are meant to guarantee a contractor’s work. They are not meant to guarantee product performance. These guarantees should be passed back to the manufacturer or covered by an insurance policy. Most surety bond companies will require the Performance Guarantee to be excluded from the contract in order to write Performance Bonds for that project.

Similar to Performance Guarantees, Surety Bond Companies do not want to be in the business of providing long term warranties. Everything breaks down over time and bond companies and their contractors do not want to be responsible for long term wear and tear. Most bond companies will require that warranties are two years or less in order to write performance bonds for the project. Anything longer should be pushed back to the product manufacturer or covered by an insurance policy.

There are notable exceptions. For example, the Department of Transportation in Iowa requires 4 years warranties on highway work. Surety Bond Companies operating in the state have become comfortable with these requirements and these performance bonds are written easily.

International Exposure makes it very difficult to write Performance Bonds. The risks associated with a contractor performing work in a different country are tremendous. Getting material and equipment to other countries is challenging and expensive. Many countries do not have a local lumber yard where additional supplies can be purchased.

Additionally, labor can be very challenging in many countries. I’ve seen contractors struggle with both expertise and getting labor to show up on a regular basis. Labor may also try to continue to negotiate for more money once the contractor arrives. Some countries even require the contractor to post advance payment bonds that commit the contractor to paying for labor before the work is done.

Political Risk is also significant for international performance bonds. In some countries, bribes are common or required. Contractors may be unable to work unless they understand the correct customs.

For these reasons and more, surety bond companies are very hesitant to write performance bonds with international exposure. Generally, these bonds are reserved for contractors who have net worth greater than $10 million and plenty of experience operating in these areas.

The exception of certain areas of North America and the Caribbean. U.S. Surety Bond Companies are generally comfortable providing bonds in Canada, Mexico and the Virgin Islands for contractors that qualify. You can learn more about International Surety Bonds here.

Long completion times increase the risk of all construction projects. Much can change over time. Prices generally escalate upwards for material and labor. People also change jobs. A contractor may run into issues obtaining other work which can impact the company’s overhead and support systems. For this reason, surety bond companies closely underwrite projects that require more than 12 months to complete.

Contractors wanting bonds for long term projects need to make sure they have a strong balance sheet to weather unforeseen circumstances. Additionally, labor agreements, or golden handcuffs may be needed to make sure key people remain in place.

Public Private Partnership or P3s combine public projects with private investment. P3s are viewed as risky by surety bond companies because often the contractor must perform work and incur costs while receiving revenue from the project’s performance. Generally, bond companies only want to write P3 performance bonds for the largest and most qualified contractors.

However, they also heavily scrutinize subcontractors on P3 projects. The reason is that the General Contractor may not be able to make payments if the project does not go as planned. For this reason, surety bond companies writing subcontractor bonds on P3 projects, generally want to verify that the General Contractor on the project has provided a payment bond. This payment bond helps ensure that the subcontractor will be paid regardless of how the P3 performs. You can read more about bonding P3 projects here.

Inadequate Financing is another red flag when trying to obtain a Performance Bond. Financing is usually not an issue on public projects. However, private projects are a different story. Contractors working on private projects should verify that the funding has been approved and set aside. Contractors have been burned and even put out of business by projects that had their financing pulled. Unfortunately, the contractors may not know until they have already performed work or purchased materials. Although Mechanic’s Liens can be filed, it may take years to collect payment.

Surety Bond Companies do not want contractors to take the financing risk on a project. Getting performance bonds on these projects often requires the contractor to verify that financing is in place and secure.

Bad contract terms make it difficult to provide performance bonds on projects. Contingent Payment Clauses, Flow Down Clauses, Damages, Indemnity Provision, Short Cure Periods and Termination Clauses can also shift undo risk back to contractors. Although some bad contract terms may be acceptable to obtain work, contractors and their surety bond companies may need to push back against some contract provisions. You can read more about Bad Contract Terms here.

Many factors can contribute to making obtaining performance bonds a challenge. These can be both contractor driven, and project driven. However, knowing what these issues are can make contractors better prepared to address the issues and obtain bonding. These issues also apply to other contract surety bonds such as bid bonds, payment bonds and maintenance bonds. Even in the worst scenarios, most contractors can obtain performance bonds with the right help and the right tools.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.