A Work in Progress Report or WIP for short is one of the most important tools a contractor and surety bond underwriter has. Learn more about how to calculate a good Work in Progress Report and what each item on the report means.

A Work in Progress report gives a snapshot of how a contractor’s uncompleted projects are performing based on estimates from the Contractor. A Work in Progress Reports is also referred to as a WIP, Work in Process, Status of Contracts, and Schedule of Contracts Reports. A WIP can be either short form or long form. You can view a WIP report here.

All contractors need a WIP report regardless of size. Contractors have varying scopes of financial statements but all types of construction financial statements should include a Work in Progress Report.

A Work in Progress Report should include all of the following:

With this information we can calculate the other items needed on the WIP Report.

Estimated Total Cost is calculated by adding Total Costs to Date and Estimated Cost to Complete. It is important for contractors to have real time project management and reporting from the field. Otherwise, the Estimated Cost to Complete and The Estimated Total Cost will be inaccurate and a contractor may not realize there is a problem on a project until it is too late.

Percent Complete is calculated by dividing Total Costs to Date by Estimated Total Cost. This calculation lets us know how much of a project is complete and remaining based on a Cost Method. The Cost Method is the most common used method to calculate Percent Complete and the one Surety Bond Underwriters prefer.

There are other methods that can be used to determine Percent Complete such as Billings and Unit depending on the contractor and type of work but these are less common.

Percent Complete under the Billings Method would be Total Billings to Date divided by Estimated Total Billings. This method is appropriate when cost may be difficult or impossible to accurately estimate.

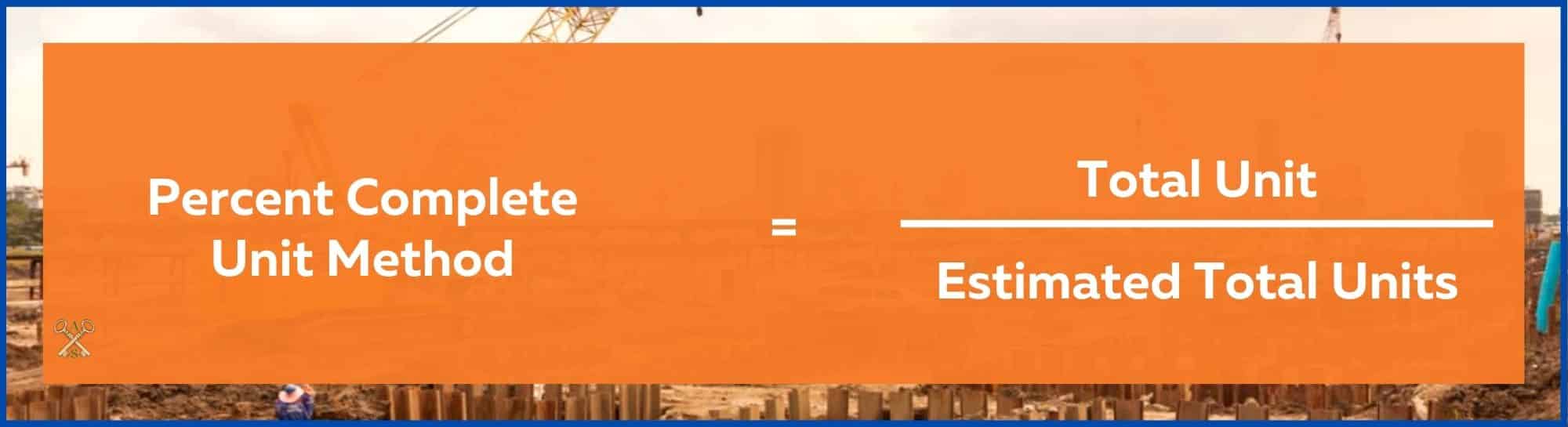

Percent Complete under the Unit Method could be a variety of things. Many times these are used on Time and Material projects such as may be used by an excavator. In this case, the Unit Method could be calculated by dividing Total Hours/Estimated Total Hours to come up with the Percent Complete.

Estimated Gross Profit is calculated by subtracting Estimated Total Cost from the Total Contract Price. Estimated Gross Profit is carefully watched by Surety Bond Underwriters of the course of a project.

If Estimated Gross Profit decreases over the course of the project, it is referred to as a profit fade. Profit fades are concerning to underwriters and questions are often asked about the problems on the project, how the contractor has fixed them and how sure the contractor is that further fades will not continue.

A contractor with multiple profit fades may have a problem with their estimating systems. This may also cause the surety bond underwriter to lose confidence in a contractor’s future estimates.

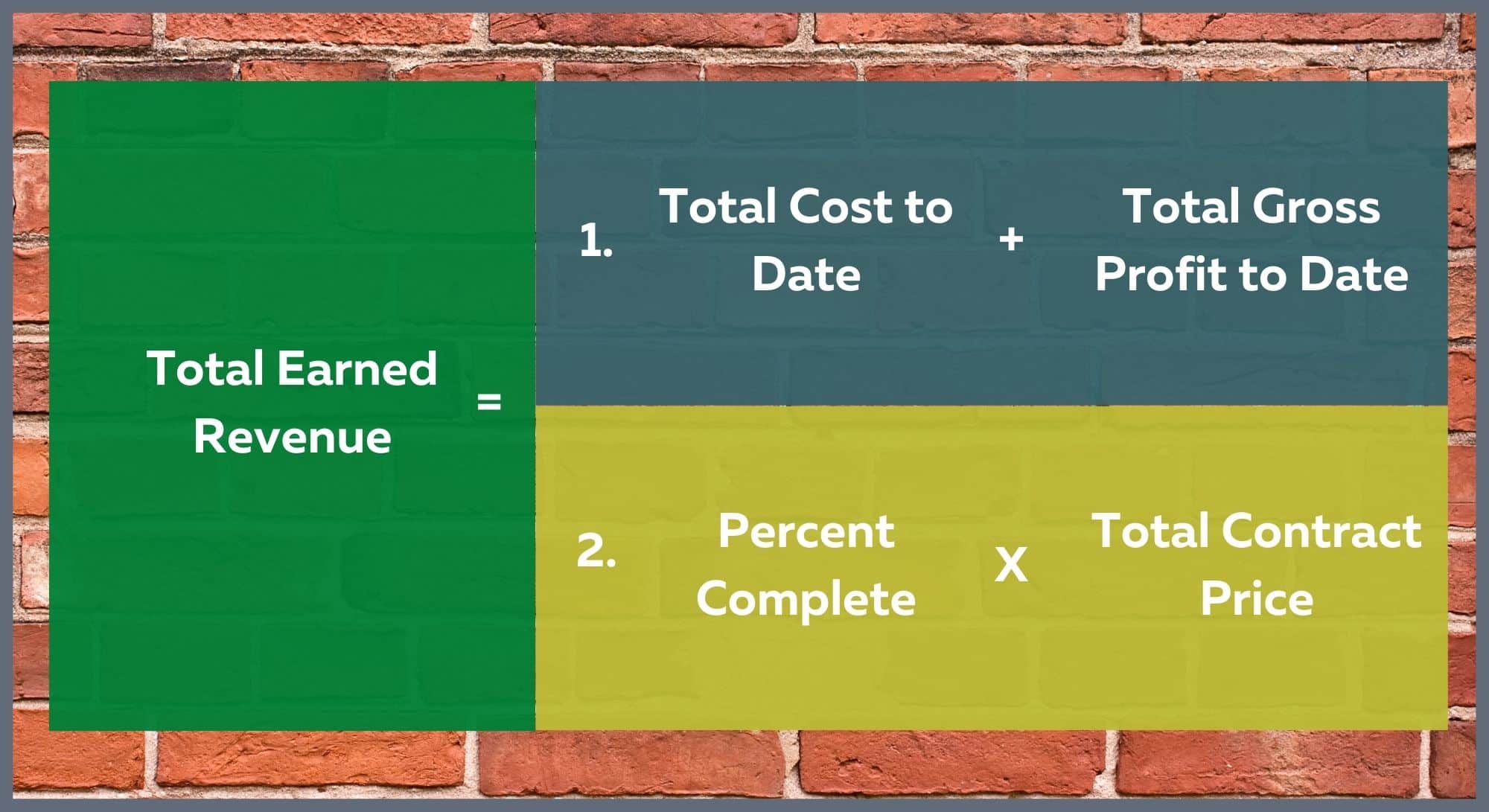

Gross Profit Earned to Date is calculated by taking Estimated Gross Profit and multiplying it times Percent Complete. Gross Profit to Date shows how much of the project’s gross profit the contractor has actually earned on the project regardless of the amount the contractor has actually billed.

Total Earned Revenue can be calculated in a couple of ways:

Total Earned Revenue gives the amount of revenue the contractor has earned on the project regardless of what the contractor has actually billed.

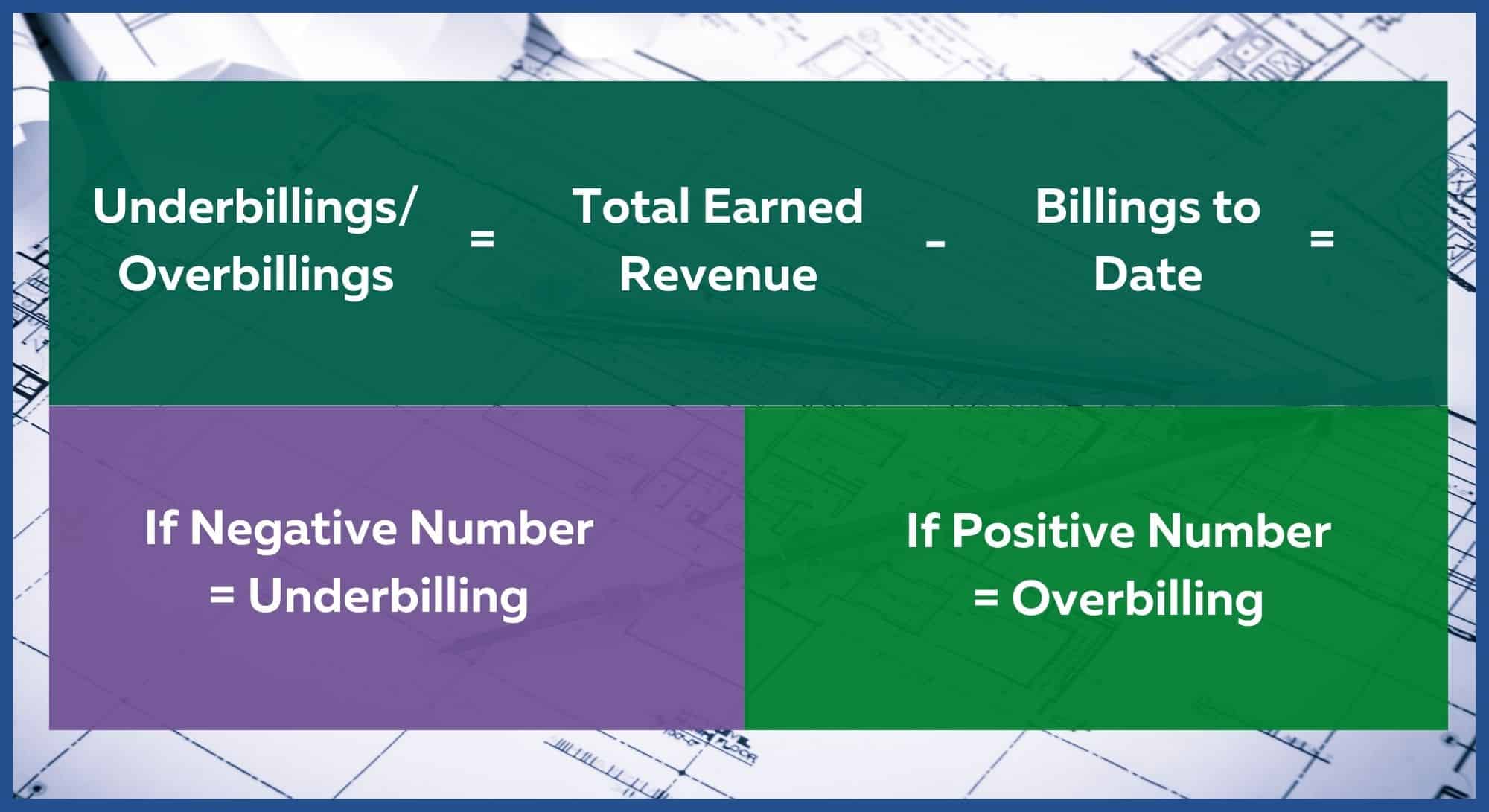

Costs and Estimated Earning in Excess of Billings on Uncompleted Projects (Underbillings) and Billings in Excess of Costs on Uncompleted Projects (Overbillings) is calculated by Taking Total Earned Revenue and subtracting Billings to Date. If Total Earned Revenue exceeds Billings to Date, the project is Underbilled. If Total Earned Revenue is greater than Billings to Date.

Underbillings and Overbillings are important. They are part of an accurate Percentage of Completion Method of Accounting.

Underbillings are very important to surety bond underwriters and should be important to contractors as well. Underbillings show up on a contractor’s balance sheet as a current asset. This is because a contractor has performed work and will collect money later.

In theory, that should help contractors as it improves working capital. However, Underbillings are often a sign of a potential loss on a project. If a contractor has earned revenue, they should bill for it timely. Underbillings often show up when there is an unapproved change order.

There are legitimate reasons for underbillings. However, a contractor who is constantly underbilled has a problem with their accounting and billings systems. They may also lose confidence of the surety bond underwriter. More can be read about underbillings here.

Overbillings are also important to surety bond underwriters. Being slightly overbilled on a project is a great practice. It allows a contractor to use the Owner’s money to their advantage. Overbillings show up on a contractor’s balance sheet as a current liability. This is because the contractor has billed for work they have not yet done. This will cost the contractor money to come back later and do the work. Surety bond underwriters look for contractor’s to have cash and accounts receivable balances that offset overbillings.

Too much Overbilling can also be a problem. When a contractor is overbilled by more than their Estimated Gross Profit on a project, it is called Pure Job Borrow. This practice is frowned upon and could signal cash flow issues. The contractor is essentially robbing one project to finance another. More can be read on Overbillings here.

Above we saw how a Work in Progress Schedule is put together. Now will look at how surety bond companies use a Work in Progress in their contract bond underwriting.

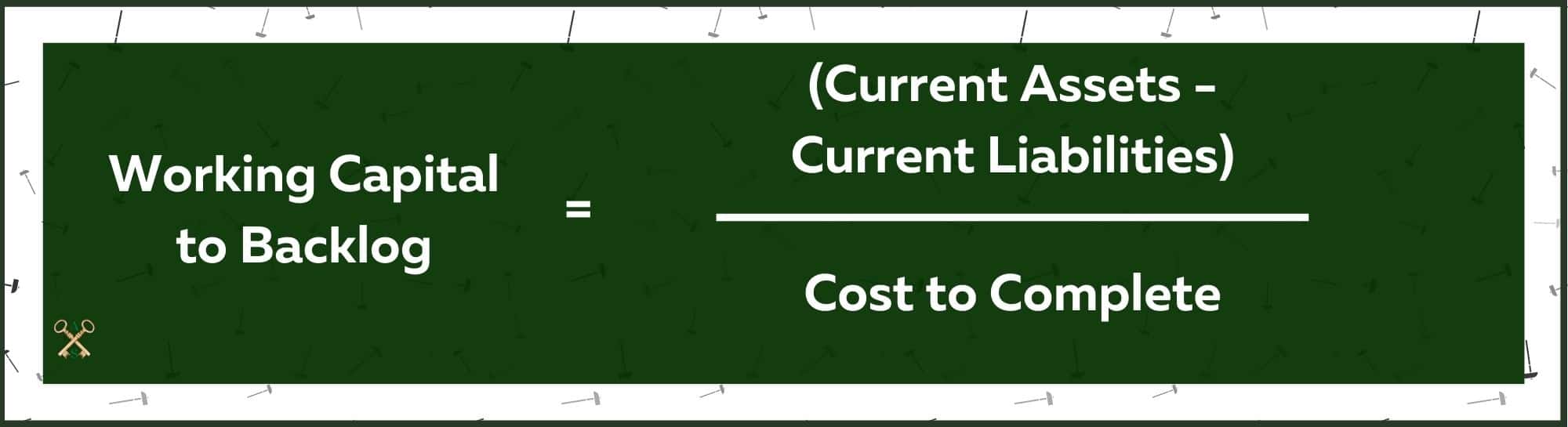

Backlog is the total amount of uncompleted work a contractor has under contract. There are a few different ways to look at backlog from a contract bond perspective. The most common is the cost method. Surety Bond Companies compute backlog by subtracting Cost to Date from Estimated Total Cost. You may notice that this is Cost to Complete. Some surety bond companies look at Remaining Billings as their measure of backlog.

Backlog can tell a surety bond company if the contractor needs more work to be profitable or if they are already stretching their capabilities. In fact, most surety bond programs are based on percentage of working capital and/or equity to backlog.

Working Capital to Backlog is calculated by taking Backlog (Cost to Complete) and dividing it by Analyzed Working Capital.

For example: A contractor with $1,000,000 in analyzed working capital and a Cost to Complete (backlog) of $20,000,000 is at a 20:1 ratio ($20,000,000/$1,000,000). Said another way, $1,000,000 is 5% of $20,000,000. In the industry this is referred to as a “5% case”. A 5% case is the normal amount of surety bond credit that many contract surety companies will give a general contractor. Therefore, if a General Contractor wants to increase their backlog by $10,000,000, they generally need to increase their working capital by $500,000 or 5%.

Equity to Backlog is calculated by taking Backlog (Cost to Complete) and dividing it by Analyzed Equity (or Net Worth). Often contract bond companies like Equity to Backlog to be 10:1 or better. Some Net Worth surety bond companies base a contractor’s surety bond capacity off of their net worth instead of working capital. These companies may want a “5% or 10% Equity Case”.

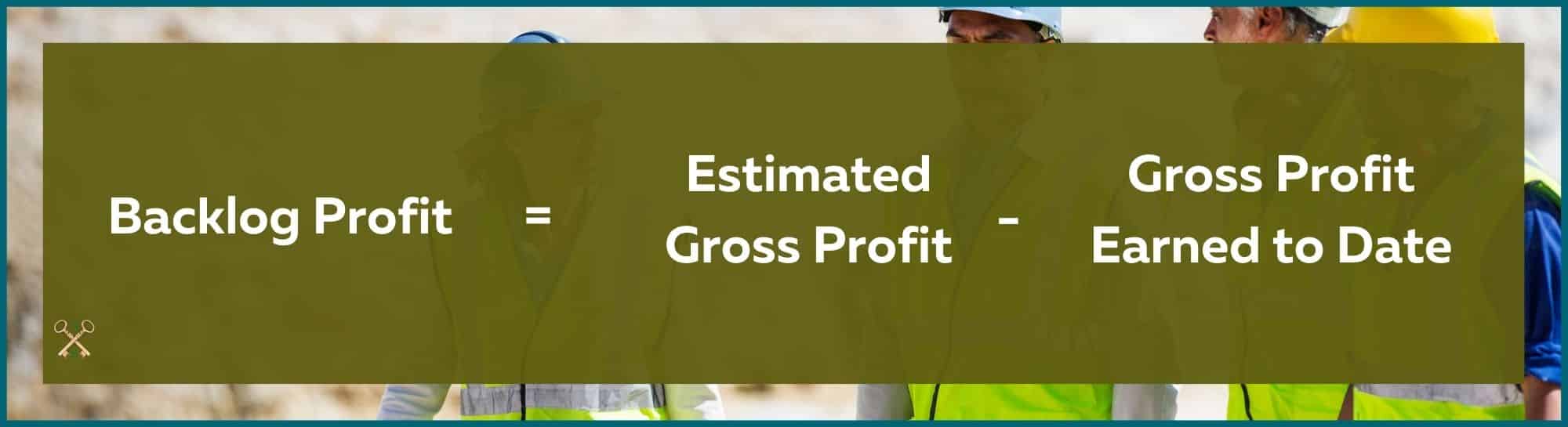

Backlog Profit is the amount of profit a contractor has remaining on their uncompleted work that is under contract. Backlog Profit is calculated by taking Estimated Gross Profit and subtracting Gross Profit to Date.

Backlog Profit is important to a surety bond underwriter because it tells them how much more work will be needed to make the contractor profitable for the year.

For example, if a contractor has $1,000,000 in overhead expenses and $500,000 in backlog profit, the surety bond underwriter knows the contractor will need more work and possibly more performance bonds to be profitable.

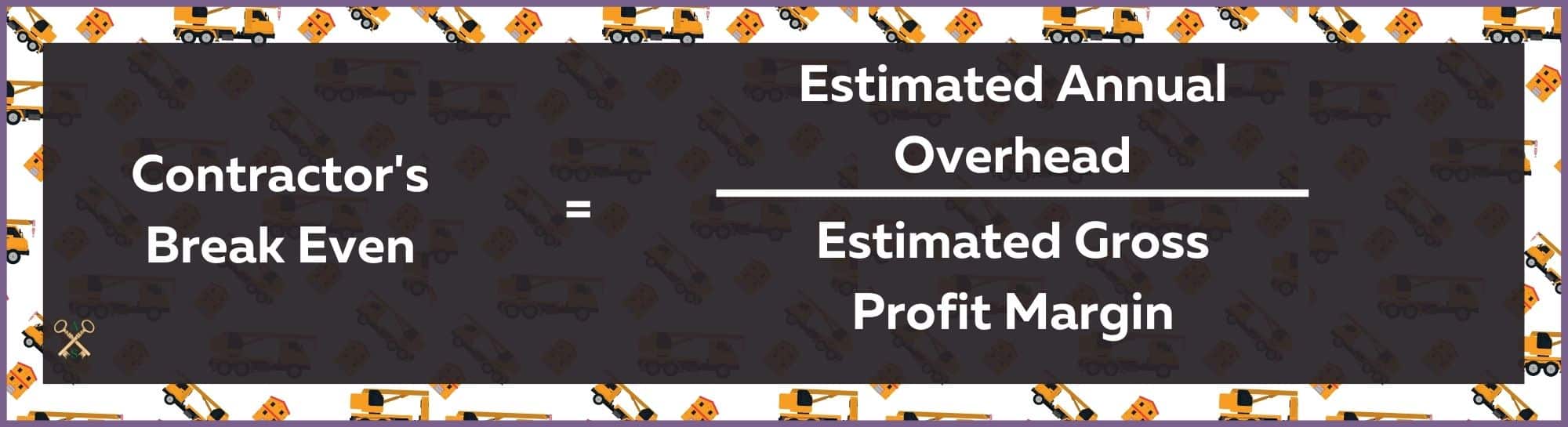

Break Even for a contractor is calculated by dividing Projected Overhead by Estimated Gross Profit Margins. Overhead and Profit Margins are unknown but there are few ways to get fairly accurate numbers. First a contractor may have good estimates that they can provide. Secondly, a surety bond company can look at the contractor’s historical profit margins and overhead to get a number.

Here is an example of how surety bond underwriters use Break Even analysis. Suppose a Contractor has an average Gross Profit Margin of 5% and the contractor’s overhead averages $1,000,000. The contractor’s break even point for the year is $20,000,000 in revenue ($1,000,000/5%). Based on the contractor’s historical performance and overhead, both the surety bond company and contractor know that the contractor needs to obtain more than $20,000,000 in work to be profitable.

Surety Bond Companies use a Contractor’s Work in Progress Report to assess trends from the contractor. Have project size and work loads increased or decreased? Are profits holding up or fading? Do certain types of projects make or lose money? All of these things factor into a surety bond company’s trust in a contractor and ability to support future work.

Although uncommon, some WIP Reports contain Estimated Project Start and End Dates. This is a requirement for the SBA Surety Bond Guarantee Program who has their own Work in Progress Form which can be found here.

Some WIP Reports specify which jobs are bonded and which jobs are unbonded. Again, this is not common but this could be important information to lenders and surety bond companies. For example, lenders typically will not lend against “bonded receivables” so they like to know which projects have performance bonds.

Secondly, some surety bond companies only look at bonded backlog. This means, the only backlog they count against a contractor’s surety bond capacity are those projects that are bonded. In these cases, it is important to know which projects are bonded so a contractor can calculate their remaining bond capacity.

A Completed Contract Schedule is normally included along with a Work in Progress Report. A Completed Contract Schedule provides information such as Total Contract Amount, Total Cost and Gross Profit on projects that a contractor has completed. This is also an important tool that surety bond underwriters use for trend analysis and to see how projects closed out. Surety bond companies may also bill final performance and payment bond premiums off the final project amounts on these schedules.

Understanding a Work in Progress Report is important for contractors to maximize their surety bond capacity, but it is also much more than that. Contractors should get in the habit of preparing and looking at these reports monthly to understand how their projects are performing and how that performance will affect their businesses.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.