ERISA Bonds are mandated to protect certain retirement and health plans. Learn more about what plans need these surety bonds, what amounts they need to be and how to obtain them.

The Employment Retirement Income Security Act of 1974 (ERISA) is a congressional law in the United States that protects individuals in most private retirement and health plans by setting minimum standards that must be followed. According to the Department of Labor (DOL), the Act:

“requires plans to provide participants with plan information including important information about plan features and funding; sets minimum standards for participation, vesting, benefit accrual and funding; provides fiduciary responsibilities for those who manage and control plan assets; requires plans to establish a grievance and appeals process for participants to get benefits from their plans; gives participants the right to sue for benefits and breaches of fiduciary duty; and, if a defined benefit plan is terminated, guarantees payment of certain benefits through a federally chartered corporation, known as the Pension Benefit Guaranty Corporation (PBGC).”

An ERISA Bond is an insurance policy that protects the plan assets against theft, fraud or dishonesty by Fiduciaries and other persons who handle plan funds or property. Acts covered by an ERISA Bond include but are not limited to embezzlement, larceny, theft, forgery, willful misapplication, willful conversion, willful abstraction and other acts of dishonesty. An ERISA Bond is considered a Fidelity Bond.

ERISA Bonds DO NOT cover Fiduciaries for acts that breach their fiduciary duties. It is NOT a Fiduciary Liability Insurance Policy. Although it is usually recommended for Fiduciaries to be covered by such a policy, it is not required under ERISA.

ERISA Bonds also do not cover investment losses caused by regular market conditions. An example would be an investment declining in market value.

Under ERISA, every Fiduciary on the plan and every person who handles funds or property must be covered by an ERISA Bond. Funds and Property include contributions from employees and employers, property, mortgages, investments, private company stock, along with cash, checks or investment used for making distributions. It is an unlawful act for anyone to receive, handle, disperse or exercise control over any covered ERISA plan assets without being covered by an ERISA Bond.

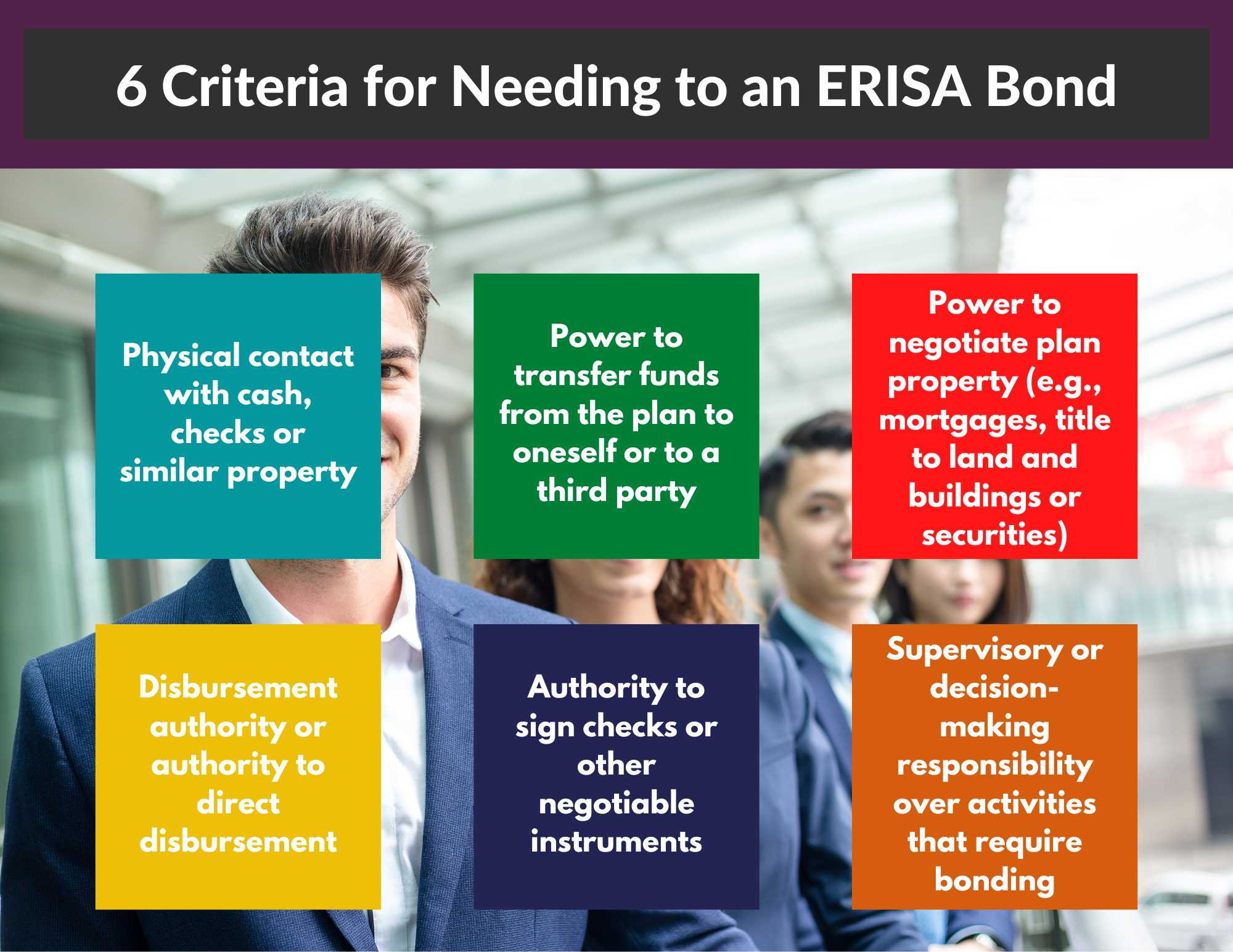

According to the Department of Labor, a person is deemed to be handling funds or property whenever their duties or activities could cause loss to the plan by fraud or dishonesty. This applies whether they are operating alone or in concert with others. The DOL further determines a general criteria for handling to include:

Anyone performing these roles must be covered by an ERISA Bond.

There is a strong industry trend to outsource many services covered by ERISA. Third Party Administrators, investment advisors and other parties must be covered by an ERISA Bond if they meet the criteria of handling funds and property for the covered plan.

Some parties are exempt from providing ERISA Bonds. These parties include:

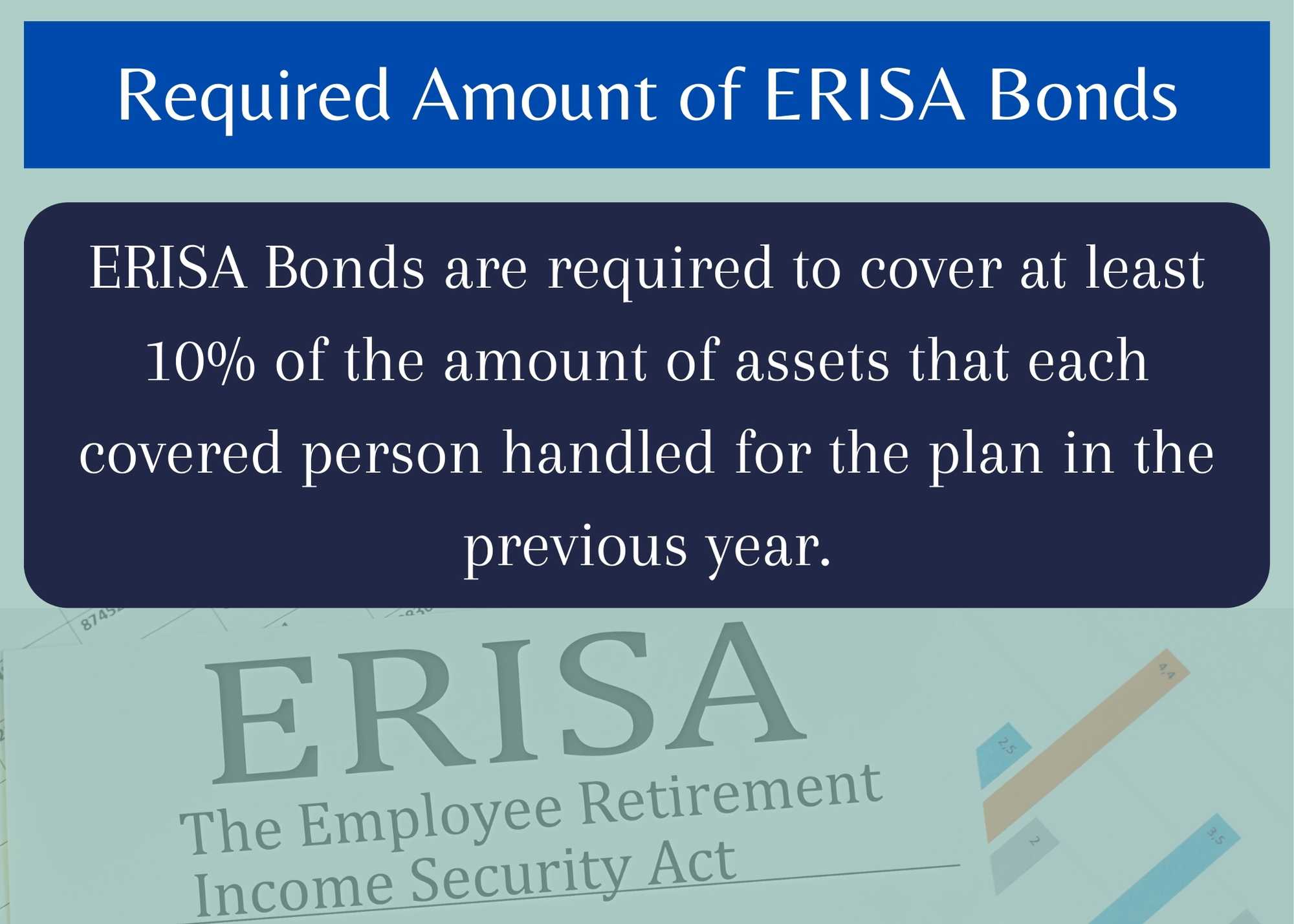

ERISA Bonds are required to cover at least 10% of the amount of assets that each covered person handled for the plan in the previous year. For example, a plan holds $1,000,000 assets in the company 401k. Trustees, administrators and other parties will need to have an ERISA Bond in the amount of at least $100,000. Generally these bonds are written to cover all the parties involved for at least 10% of the plan assets. If there is no previous plan year, the DOL allows the company to make estimates for the plan amount.

The law does set both a minimum and maximum amount required for each individual under an ERISA Bond. An ERISA Bond must be at least $1,000. However, the required amount does not have to exceed $500,000 for most plans. This maximum increases to $1,000,000 if the plan holds company securities in the plan.

An ERISA Bond may cover multiple plans. However, the $500,000 bond maximum does not apply when more than one plan is covered. The bond amount in such cases must still meet the 10% requirement for BOTH plans. For example, an employer is covering two plans with an ERISA Bond. One plan has $1,000,000 in assets while the other plan has $5,000,000 in assets. The minimum amount of the ERISA Bond must be $600,000. This is calculated by taking Plan 1’s minimum amount ($1,000,000 x 10% = $100,000) and adding it to Plan 2’s minimum amount ($5,000,000 x 10% = $500,000). A claim by one plan can not reduce the minimum amount available for the second plan.

Although the DOL sets a maximum required ERISA Bond amount, Employers should consider higher or full limits. A loss to employee retirement assets by dishonesty or fraud could destroy a company’s reputation, cause devastating litigation and potentially a loss of its workforce.

Failure to report the correct bond amount on the company’s 5500 could trigger an Audit of the plan. It can also lead to plan termination and penalties.

Some ERISA Bonds contain an “Inflation Clause”. These clauses generally raise the bond amount by a specified amount each year to accommodate an increase in assets. These clauses do provide great protection to covered parties. However, ERISA Bond limits should still be reviewed regularly. Increased contributions, market performance and other factors can often lead to bond limit increases that may exceed the inflation amount.

For larger plans, a “no dollar” ERISA Bond may be purchased. These bonds say that the ERISA Bond covers 10% of plan assets, at a minimum of $1,000 and a maximum of $500,000. These bonds are allowed by ERISA and protect the company from increases to the plan assets automatically.

An ERISA Bond cannot have a deductible or any mechanism to reduce the bond’s ability to pay first dollar of the minimum required amounts. However, an ERISA Bond may have a deductible above the minimum amount.

Although “Bond” is in the name, an ERISA Bond is an insurance party. It is a two party agreement. The Plan is the beneficiary of the bond. The surety or insurance carrier is the party writing the coverage. Unlike a surety bond, indemnity is not required for an ERISA Bond. Should a covered individual cause a loss, the plan can make a claim against the ERISA Bond. You can read about differences between surety bonds and insurance here.

ERISA Bonds are very easy to obtain. Many companies can simply add the coverage through their commercial insurance policy. Others can purchase ERISA Bonds online in just a few minutes by clicking the button below. ERISA Bonds are considered low risk and easy to obtain for almost any business.

Many ERISA Bonds do contain exclusions for any individuals known by the plan to have committed acts of dishonesty. These individuals will need to be prevented from handling plan funds and property or an ERISA Bond without this language will need to be secured.

ERISA Bonds Costs depend on the insurance carrier writing the bond. However, these bonds are very inexpensive. The cost of an ERISA Bond is usually about 0.1%. For example, a $500,000 ERISA Bond can be obtained for about $500.

Because it is a U.S. Government requirement, all ERISA Bonds must be written by a surety bond company or insurance company that is approved in the U.S. Treasury’s 570 Circular. Certain Lloyds of London Insurers are also allowed to write ERISA Bonds.

ERISA Bonds are an important instrument to protect employees from dishonesty and fraud. These bonds are required by law and should be in place for any company utilizing a covered plan. These bonds are very easy to obtain and inexpensive so all companies can easily meet the requirements.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.