Performance bonds and payment bonds vary in cost depending on the qualifications, financial strength of the principal and the contract being bonded. Unfortunately, very few resources are available to help contractors understand and improve their performance and payment bond costs. Most resources give a generic amount such as 0.5% – 3%. This article provides deep insight into these contract bond rates so that contractors can understand what they are paying for performance and payments bonds and work to improve those rates, if necessary.

Surety Bond companies that write contract surety bonds in the United States must file their rates in each state before they can issue bonds in that state. The Surety and Fidelity Association of America (SFAA) assists surety bond companies with this process. The SFAA collects data from its member surety bond companies and then develops loss costs. These loss costs assist the surety bond companies on what rates to file in each state. 98% of the surety premium is written by SFAA members so their information is vital to the industry’s rate making.

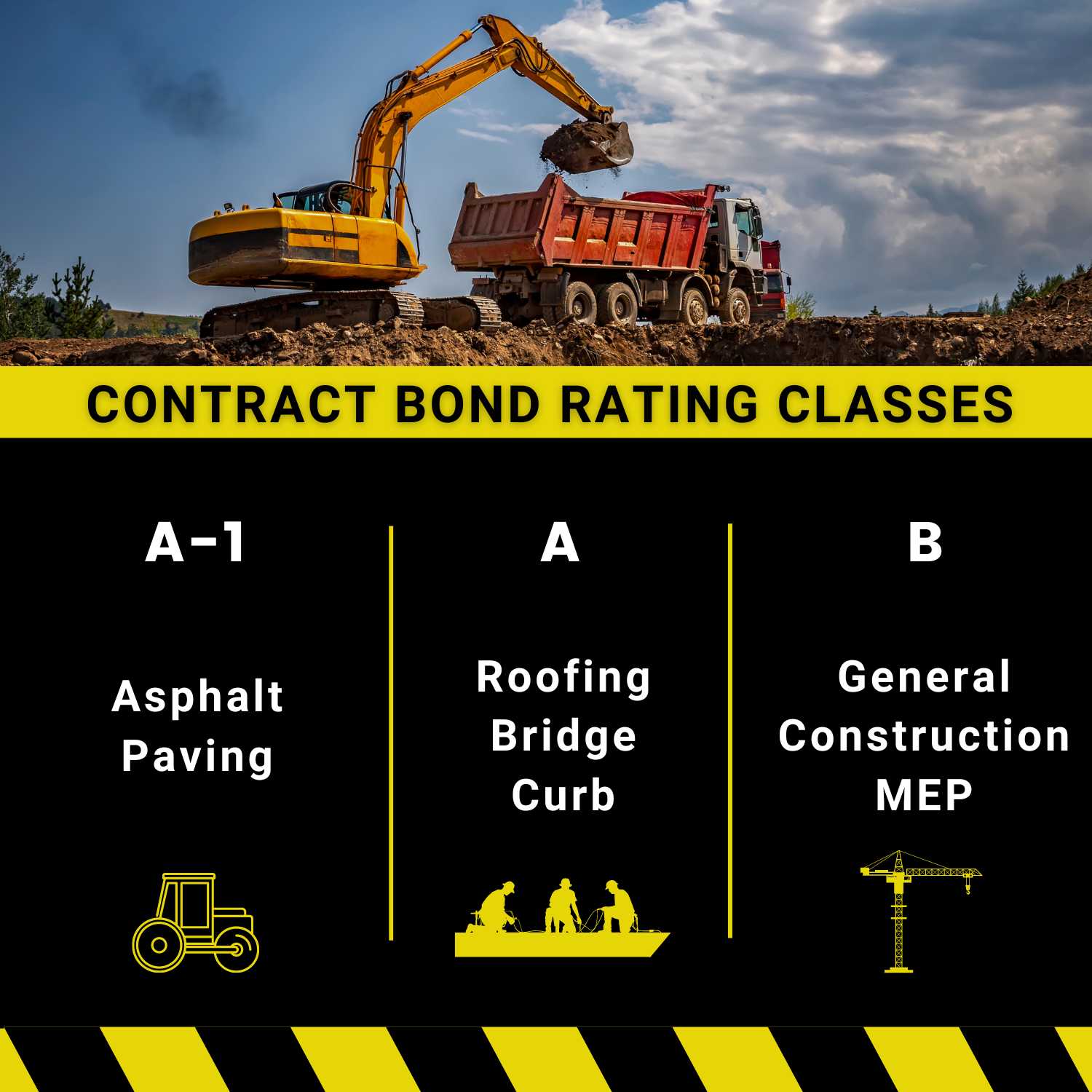

The first thing contractor need to understand about Performance Bond and Payment Bond costs is that they are rated by the class of the work being performed. Class B work includes things like General Construction of buildings, utility work, etc. Class A includes things like Roofing, Bridgework, Curb and Gutter, etc. There is also a Class A-1 which includes trades such as asphalt paving. Finally, many Contract Bond companies have a rate for Completion Bonds or Subdivision work. Each class includes tiers such as “Standard”, “Preferred” and “Merit” rates. Most Contract Bond companies have multiple filings for each class of business. Here is an example:

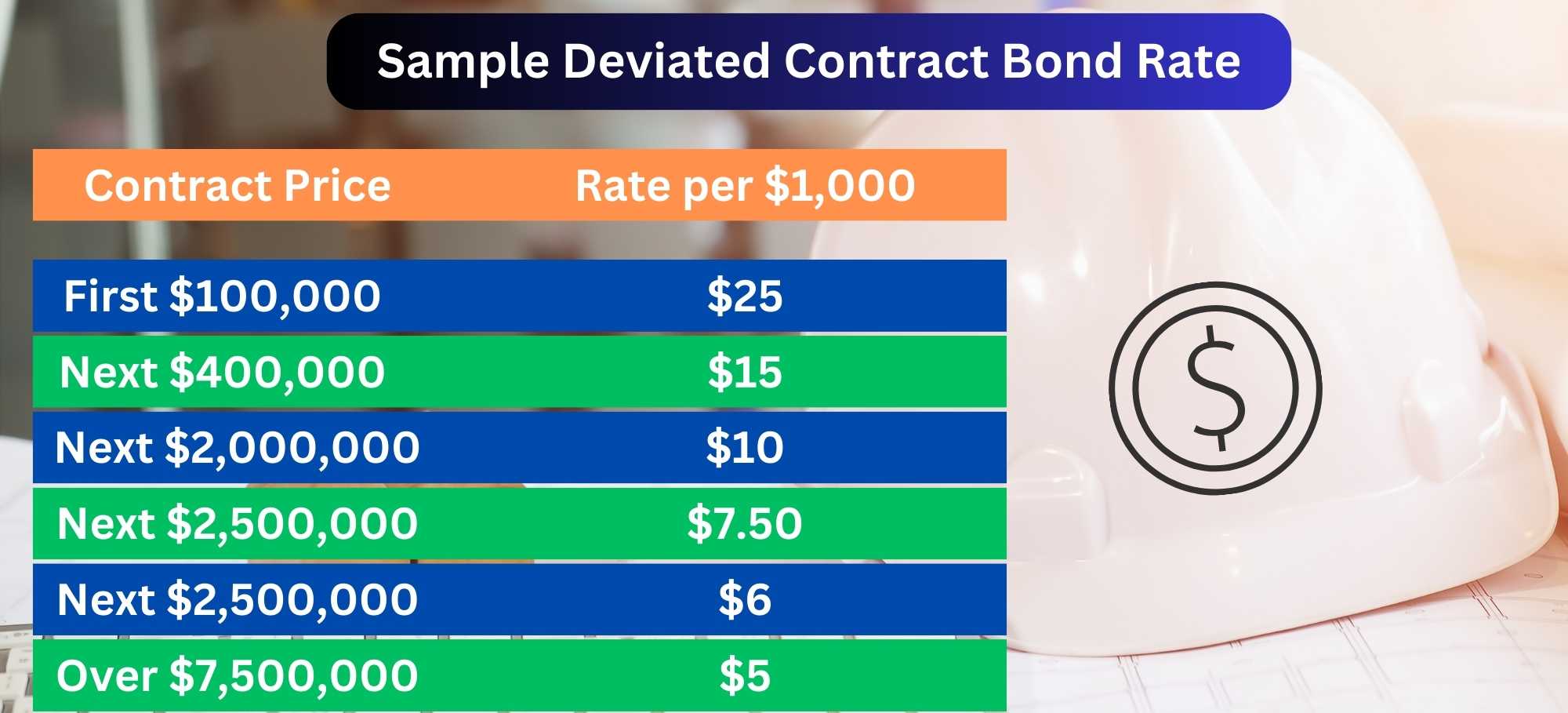

This is a standard Class B rate. Like most surety rates, the standard rate drops as the project gets larger. The contractor is charged $25 per $1,000 (2.5%) for the first $100,000 of contract price. To say it another way, if the contract is $100,000 or less, the rate would simply be 2.5%. What if the contract is $500,000? The calculation is as follows:

$100,000/$1,000 = 100 x $25 = $2,500

$400,000/$1,000 = 400 x $15 = $6,000

Our total premium on this project would be $8,500 ($2,500 + $6,000).

Most Contract Bond underwriters can also “debit” and “credit” rates by 20% – 30%. This gives the underwriter and Bond Broker some flexibility. Using the example above, if a 20% credit is applied to the Standard Rate, the breakdown would be as follows:

First $100,000 of Contract Price $20/$1,000

Next $400,000 of Contract Price $12/$1,000

Next $2,000,000 of Contract Price $8/$1,000

In this scenario, the cost for a $500,000 Performance Bond would be calculated as follows:

$100,000/$1,000 = 100 x $20 = $2,000

$400,000/$1,000 = 400 x $12 = $4,800

The total premium on this project would be $6,800 ($2,000 + $4,800).

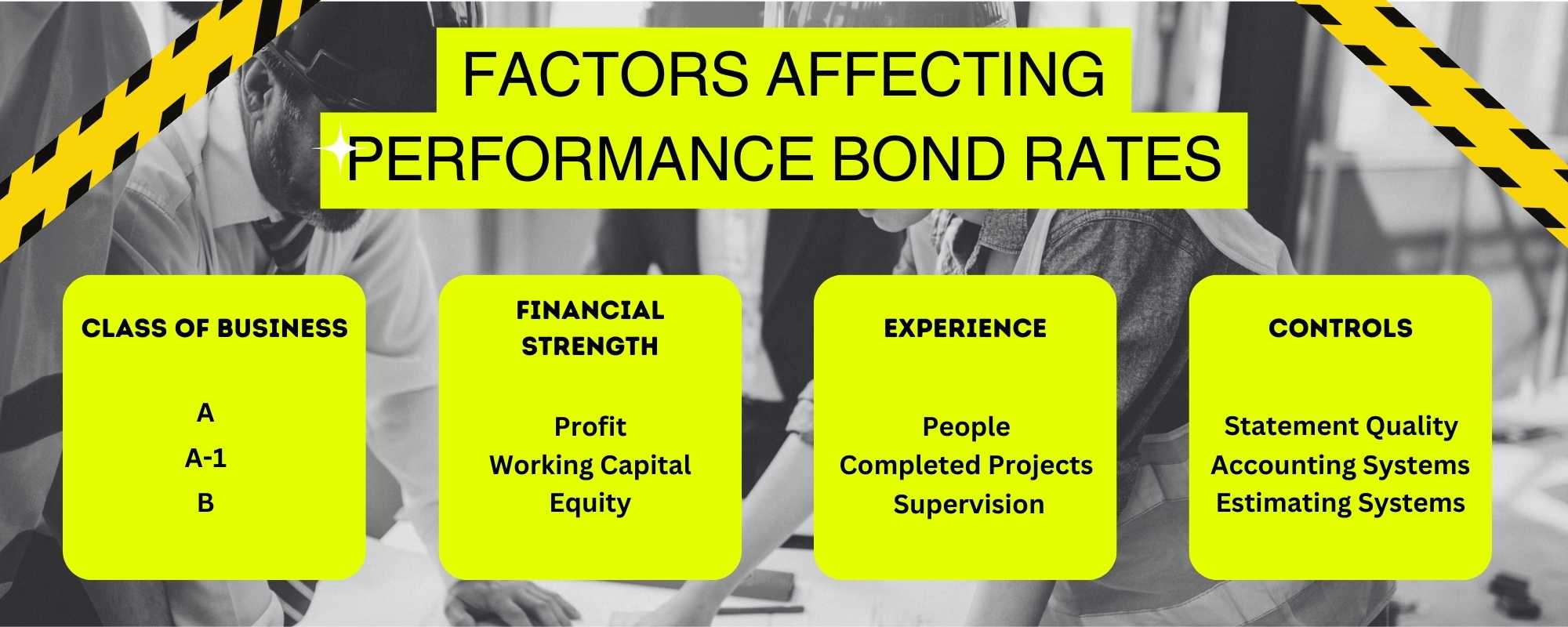

How do contract bond underwriters determine whether a contractor gets standard bond rates, preferred rates, merit rates or others? It is mostly determined by the financial strength and experience of the contractor. Contract Bonds are form of credit, similar in many ways to banking. Therefore, the strongest companies get the best performance and payment bond rates. Having more net worth, liquidity, experience and a track record of profitability will help contractors get better bond rates.

For many contract bond companies, financial presentation is also an important factor in determining performance and payment bonds costs. For example, having a strong CPA prepared Audit or Review will qualify a contractor for better bond rates than a contractor who is only getting a CPA Compilation or using internally prepared financial statements. A helpful breakdown on the different scopes of statements can be found here.

Not all performance and payment bond rates are on a sliding scale. New contractors, contractors with infrequent contract bond needs, contractors without CPA prepared financial statements or those contractors with financial challenges are often asked to pay higher contract bond rates in the form of a flat rate. Common examples include 1%, 1.5%, 2% and 3% flat rates.

Over the last 15 years, the use of personal credit-based underwriting for contract bonds has increased. These programs allow Performance Bonds and Payment Bonds to be issued for projects as large as $1,500,000 without providing any financial statements to the surety bond company. These programs are underwritten on the personal credit of company owners. If the owner(s) credit is acceptable, the bonds can be issued without other underwriting information.

The tradeoff for this ease in getting the contract bonds is that the costs are usually more expensive than obtaining performance and payment bonds through traditional means. Many contract bond companies charge a 3% or 2.5% flat rate for these bonds. However, the industry is getting more competitive, and some contract bond companies are starting to offer sliding rates for these credit-based programs.

Even with the higher cost of these credit-based performance and payment bonds, the ease of getting these bonds can easily offset the cost for many contractors. These bonds can usually be approved in a matter of minutes or hours for those with acceptable credit.

Design-Build contracts contain more risk than regular Design – Bid – Build Construction contracts. The principal contractor is responsible for all or part of the design risk, regardless of whether the design is subcontracted to a professional design firm. When contractors must provide Performance and Payment Bonds on these Design Build projects, they should expect to pay higher rates.

Most contract bond companies have a design build surcharge. That additional surcharge is usually 20% – 50% of the standard Performance Bond premium. Here is an example:

Assume the Design Build Surcharge is 20% and the class B Performance Bond premium is $8,500. Under a Design Build project, that same Performance Bond would now cost $10,200.

Expect Contract Bond companies to charge this surcharge even if the design work is subcontracted to a professional design firm. Contractors are often surprised by this. They often believe they have no design exposure or risk. Be aware that if your contract says, “Design Build”, your Contract Bond company will charge you the Design Build rate for your Performance and Payment Bonds.

You can read more about performance bonds on design build projects by clicking the image.

Another factor that can increase the cost of performance and payment bonds is the completion time of the project. The longer a construction project takes to complete, the more risk to the contract bond company and the contractor. Most contract bond companies give you up to 12 months to complete a project before a surcharge is added. Projects that exceed 12 months to complete are subject to additional bond costs. Often, this is 1% a month after the first 12 months.

Here is an example. Suppose there is a 1% surcharge after 12 months. The project is expected to take 18 months to complete, and the regular premium is $8,500 from the example above. The time surcharge premium would be:

18 months minus 12 months = 6 months.

6 months x 1% per month = 6%.

Therefore, we take our $8,500 premium and multiply it times 0.06 = $510.

The time completion surcharge is $510 in this scenario. That surcharge would be added to the regular premium for a total of $9,010 ($8,500 + $510).

Another factor contributing to performance and payment bond costs is maintenance. Many construction contracts contain a warranty or maintenance period. This can be anywhere from 12 months after project completion to a much longer period.

Each contract bond company has different rules for maintenance. Some include 12 months at no addition cost if it is issued with a performance bond. Others may include maintenance up to 24 months after project completion for no additional cost. Additional maintenance periods beyond the bond company’s limits will cause an additional maintenance charge, however. This additional premium will factor into your total performance and payment bond cost.

Maintenance costs are calculated in a similar manner to the regular performance and payment bond costs. Each contract bond company has their own maintenance rates, and they can be flat rates or on a sliding scale. Standard maintenance rates are on a sliding scale and may look something like this example:

First $100,000 of Contract Price $2.50/$1,000

Next $400,000 of Contract Price $2.00/$1,000

Next $2,000,000 of Contract Price $1.50/$1,000

Continuing on the previous examples and using a contract in the amount of $500,000, each additional year of maintenance can be calculated as follows:

First $100,0000/1,000 = 100 x $2.50 = $250

Next $400,000/1,000 = 400 $2.00 = $800

Total Premium for Each Additional Year of Maintenance = $1,050

Again, this is added to the regular bond cost. If the Performance Bond cost $8,500 with an extra year of maintenance, the total bond cost is now $9,550 ($8,500 = $1,050).

If there are two additional years of maintenance, the total bond cost is $10,600 ($8,500 + $1,050 + $1,050).

As we discussed, contract bond companies determine performance and payment bond costs on factors such as filed rates, class of business, experience, credit score, financial strength and quality of financial statements. However, another major factor in determining contract bond costs is the type of contract bond company you are working with.

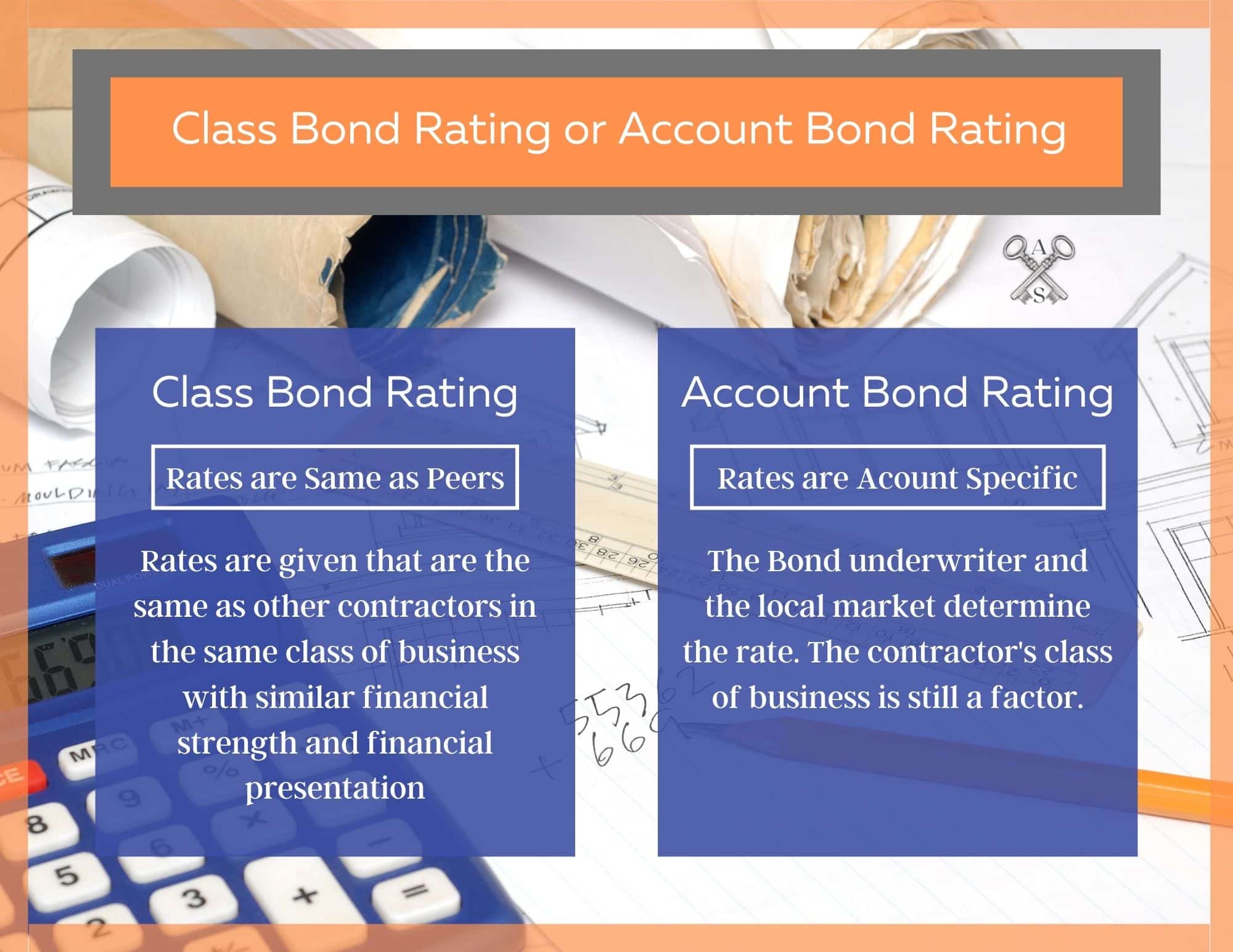

Some contract bond underwriters have a lot of flexibility in determining what performance and payment bond rates they give contractors. Other contract bond underwriters have very little control over their rates. This is because most surety bond companies fall into one of two categories. They either use account rating or class rating.

Contract bond companies that use account rating tend to have more flexibility when determining a contractor’s bond rate. They rely on their local underwriters to make decisions on the bond rates they give each account. Usually, these bond underwriters are given broad authority to assign rates based on the merits of the account and that underwriter’s experience with local market conditions. Regional and specialty contract bond companies are more likely to use account rating.

On the other hand, many larger contract bond companies use class rating. This means contractors are given their performance and payment bond rates depending on what categories they fall into. For example, all contractors performing Class A Road Work with a CPA Reviewed Statement and tangible net worth from $1,000,000 – $2,000,000 will receive the same rate.

The thought process is that all similar accounts are on a level playing field when it comes to their contract bond rates and costs. Under this scenario, a contractor would only be able to improve their performance and payment bond rates by making a fundamental change such as increasing their tangible net worth or upgrading their CPA statement. This could be accomplished by converting from a CPA Compiled Financial Statement to a CPA Review Financial Statement or it could be accomplished by converting from a Reviewed Financial Statement to a Audited Financial Statement.

It’s important for contractors to understand a contract bond company’s thought process so they can make appropriate business decisions. Here is an example for a small contractor:

In this example, a contractor needs performance and payment bonds on a project with a contract price of $1,500,000. The contractor is not a frequent user of contract bonds and has decided to have a CPA Compiled Financial Statement. The contractor qualifies for a better performance and payment bond rate from a financial standpoint, but because the scope of his financial statement is a CPA Compilation, the contract bond company’s best Class Rate is a 1.5% flat bond rate. The cost for the performance and payment bonds would be $30,000 in this example.

As an alternative, assume that the same contract bond company would give that contractor a Class B Standard $25 sliding rate if they upgraded to a CPA Reviewed financial statement. The performance bond cost on a $25 sliding rate would be $18,500. Assuming a quality CPA Review from a construction-oriented CPA cost the contractor $10,000, they would be slightly ahead under this scenario.

However, if that contractor needed another performance or payment bond during the same year of similar size, the savings by converting to a CPA Review would be significant. Contractors should consider these factors when making business decisions as they could have a large impact on their overall performance and payment bond costs for the company.

Performance Bonds are typically issued with Payment Bonds. If these two bonds are issued together, there is only one charge for both bonds. Under this common scenario, the obligee gets double the protection for one price. Both Performance Bonds and Payment Bonds can be issued by themselves, but the cost remains the same regardless of whether they are issued together or independently. Said another way, a performance bond by itself will cost the same as when it is issued in combination with a payment bond and vice versa.

The exception to this rule is a maintenance bond. There is typically no additional charge to issue a maintenance bond if it’s less than 12 months and issued with a performance. However, if a maintenance bond is issued by itself, the maintenance bond rates are normally higher and will cost more than if it is combined with a performance bond.

Contractors should also understand overruns and underruns when it comes to Performance and Payment Bond costs. Performance and payment bonds costs are based on the FINAL amount of the contract they are guaranteeing. Changes to the contract price throughout the project will also change the final performance and payment bond cost.

Change orders that increase the contract price create what is called an overrun. That means that more premium is owed to the contract bond company by the contractor. This happens because the final contract price has increased beyond what was initially bonded and the Contract Bond Company is owed for this increase in risk. As a counter to that, a decrease in contract price creates an underrun and the contract bond company owes the contractor money back because the final contract price has decrease from the initial bonded amount.

These changes to the bond cost are applied on the back end of the contract. That is important when you have a sliding rate because any overruns may be invoiced at a lower rate and underrun may be invoiced at a higher rate. Here is an example:

Here are the standard Class B rates used in the previous examples:

First $100,000 of Contract Price $25/$1,000

Next $400,000 of Contract Price $15/$1,000

Next $2,000,000 of Contract Price $10/$1,000

Recall that on a $500,000 contract, these rates gave a performance and payment bond cost of $8,500 calculated as follows:

$100,000/$1,000 = 100 x $25 = $2,500

$400,000/$1,000 = 400 x $15 = $6,000

Now assume that a change order created a final contract price of $600,000. This would create an overrun of $100,000. The overrun would be calculated as follows:

$100,000/$1,000 = 100 x $25 = $2,500

$400,000/$1,000 = 400 x $15 = $6,000

$100,000/$1,000 = 100 x $10 = $1,000

The total performance and payment bond cost for the project would be $9,500. However, the contract bond company already invoiced $8,500 so the overrun would cost an additional $1,000 in bond premium.

If instead of increasing the contract price, there was a change order that lowered the final contract price to $400,000, there would have an underrun. The underrun would be calculated as follows:

$100,000/$1,000 = 100 x $25 = $2,500

$300,000/$1,000 = 300 x $15 = $4,500

The total performance and payment bond cost for the project would be $7,000. However, the contract bond company already invoiced $8,500. The underrun means they would return $1,500 to the contractor.

The reader will notice that in both examples, the final contract price changed by $100,000 but the bond premium changed by different amounts. This is the result of a sliding bond rate. The overrun pushed a portion of the contract into the $10 or 1% rating scale. The underrun, however, was all invoiced at the $15 or 1.5% rate.

Bond companies routinely send out contract status reports to the obligees on Performance and Payment Bonds throughout project to see how the projects are progressing. Some contract bond companies assess contract prices based on these status reports and will invoice overruns and underruns throughout the project. Other contract bond companies send a status at the end of a project and invoice any changes then. Contract bond underwriters may also use a contractor’s Completed Contract report to get these final contract amounts.

Although not a direct Performance and Payment Bond Cost, additional tools used to by surety bond underwriters to support these bonds can add to the overall cost of the bonds. Contract Bonds are a type of credit product and contractors that have financial challenges may be required to use different tools to support Performance and Payment Bonds. Some of the more common tools include The SBA Surety Bond Guarantee Program, Funds Control and Collateral. More detail on these products can be found elsewhere but when these tools are required, they do increase the costs of performance and payment bonds.

Currently the fee for this program is 0.6% of the bonded contract amount. Contractors using this program will have to pay the fee directly to the SBA before receiving their Performance Bond or Payment Bond.

Going back to the example of a $500,000 contract at a standard Class B Rate, the bond premium was $8,500. However, a contractor using the SBA’s Surety Bond Guarantee Program would have to add an addition $3,000 ($500,000 x .6%) to their performance or payment bond cost. This would make their total performance bond cost $11,500 ($8,500 + $3,000).

You can read all about the SBA Surety Bond Guarantee Program.

Funds Control acts as an escrow account for contract proceeds and payments. Contract Bond underwriters use it to ensure that the revenue from the project they are bonding is used to pay the subcontractors and suppliers on that project first. This funds control service has a cost. Most funds control companies charge 0.75% – 1.00% of the contract price for this service. Again, assuming a $500,000 contract, the funds control services would add $5,000 to the Performance and Payment Bond Cost. Read more about funds control.

Collateral for Performance Bonds can take many forms such as an Irrevocable Letter of Credit, Real Estate and Investment Accounts. However, the most common collateral used by bond companies is an Irrevocable Letter of Credit in favor of the bond company. The ILOC amount required can be a percentage of the bond amount or an underwriter may require it to be for the entire contract amount.

The cost for an ILOC is determined by the contractor’s lender, but generally run between 0.5% – 2% of the required amount annually. It is also important to know that most contract bond companies will require this ILOC to be in place for six months after the completion of the bonded project and the contractor must keep paying interest until that time has passed. Read more about Surety Bond collateral.

These surety bond tools can be valuable for contractors that have had financial challenges or issues obtaining bonding. They do increase the costs of Performance and Payment Bonds, but they also give contractors the ability to obtain a bond when they may not be able to otherwise.

Keep in mind that there is nothing preventing a surety bond underwriting from requiring more than one of these tools. Doing so could increase the cost of bonding significantly. Using the examples above, a $500,000 contract that requires both SBA support and Funds Control to get approval, could cost the contractor $16,500 ($8,500 standard premium + $3,000 SBA Fee + $5,000 Funds Control). Additionally, if a contractor is in position where multiple tools are needed, a contract bond company will likely be charging them a higher underlying rate such as a 2% or 3% flat rate. This makes a performance or payment bond relatively expensive, but the contractor may have to pay it to get the contract.

Performance and Payment Bond Costs are based on the final price of each contract. Usually these are a one-time cost for each project such as in a construction contract. However, there are exceptions. Service Contracts often require performance bonds and payment bonds as well. Examples of service contracts include things like mowing services, security services, and cleaning contracts.

These contracts are often long term in nature and open ended on the contract price. Therefore, pricing for these performance and payment bonds are usually done on an annual basis. An example would be a three-year contract for security services at an annual contract value of $500,000. A contract bond company would usually issue a $500,000 performance and payment bond once for the underlying contract, but the premium would be due each year for the three-year duration. This makes bond costs for service contracts slightly different than most performance and payment bonds. Read more about bonds on service contracts.

Bond Cost Calculators make determining costs on Performance Bonds and Payment Bond easy. Simply enter the contract amount and the rates and the calculator will determine the bond premium. The downside to the calculator is that it does not calculate design build surcharges, or time completion surcharges. You can find a Bond Cost Calculator by clicking on the image.

Performance Bonds and Payment Bonds are considered a job cost. The principal contractor on the bond is ultimately responsible for making payment to the surety company and any failure to do so will come back on them. However, as with most job costs, the party requesting the bond ultimately absorbs the cost because a contractor will add it into their bid or estimate.

For example, if a public school includes a requirement for performance and payment bonds in their specifications, they also include the cost in their estimate. This is because they know all good contractors will include the price of the bonds in their bid.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.