Subcontractor Default Insurance and Performance Bonds both protect against subontractor Default on a project. Learn more about the differences between these two tools and which is right for your project.

As the name suggests, Subcontractor Default Insurance or SDI is an insurance policy that protects the policyholder against an economic loss caused by the default of one of its covered subcontractors. Some contractors still refer to SDI as “SubGuard”, which was the original program developed by Zurich.

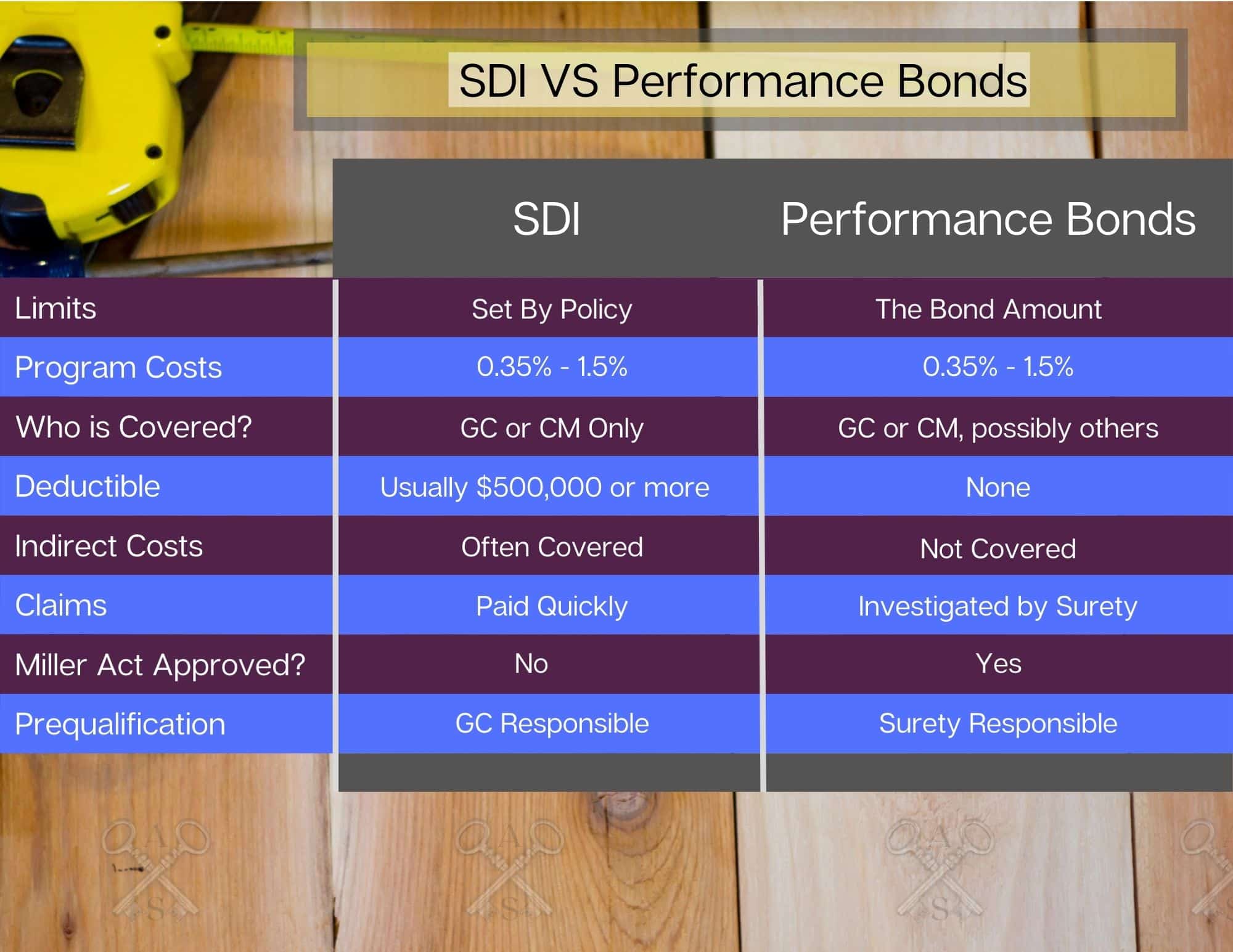

Like most Insurance policies, SDI is a two-party agreement between the insurance carrier and the policyholder (General Contractor or Construction Manager).

The increase in SDI usage has caused additional Insurance companies to enter the market and offer the product. Each company has unique underwriting guidelines, limits and deductibles.

A performance bond is a credit product that guarantees that the principal (contractor) on the bond will complete the bonded contract according to the terms and conditions.

Performance Bonds are three party agreement between an obligee (General Contractor or Owner), Principal (Subcontractor), and a Surety (Bond company).

Claims against an SDI policy is a major advantage. Once a Default occurs, a claim can be submitted and paid quickly to keep a project moving along. This is often referenced as a reason contractors choose SDI instead of performance bonds.

Another major benefit to SDI is that these policies can be crafted to cover additional costs such as indirect cost when a claim is made. No such benefit exists under performance bonds.

Because SDI is an insurance policy, there are deductibles that must be paid by the General Contractor.

Each policy is different but it is common to have a deductible of $500,000 or more. This means that the General Contractor must have a loss that exceeds this amount before getting any benefit.

Most of these policies also have Coinsurance provisions that can affect the reimbursement amount.

These can be significant detractors from SDI as many contractors cannot afford to absorb one or more losses of this size.

When a contractor on a performance bond has been declared to be in Default and a claim is made against the performance bond, the bond company must investigate the claim to make sure it is valid.

Investigating a Default is time consuming and may hold up a project. This is one of the biggest disadvantages of a performance bond when compared to Subcontractor Default Insurance.

However, making sure the claim is valid is an important aspect of a performance bond as the principal must reimburse the bond company for any paid loss under the indemnity agreement.

Some surety bond companies are now providing bond forms that make some cash available so that a project can continue while a claim is being investigated.

Performance Bonds are also limited to completing the contract. Indirect costs are not covered, and the bond amount is the most a surety is required to pay to remedy the situation.

Performance Bond claims also carry another large downside from the perspective of the obligee. The Surety on the bond gets to decide how to cure the default.

This can include financing the existing Subcontractor, finding a replacement, taking over the project or just paying the obligee. This lack of flexibility is a big disadvantage compared to SDI.

You can read all about Performance Bond Claims.

Performance Bonds are not Insurance and are not subject to deductibles or coinsurance. Surety covers first dollar losses meaning the General Contractor or Construction Manager is reimbursed for the full loss subject to the bond limit.

This is vital for contractors who cannot afford to absorb large SDI deductibles.

SDI generally costs between 0.35 – 1.35% of the project amount. Sometimes carriers may provide an opportunity to return premium for good performances in these programs. However, SDI has other indirect costs such as pre-qualification expenses.

Performance Bond Cost is based on a Contractor’s financial strength, the type of work being performed, and a bond company’s rate filings. Generally, a performance bond will cost between 0.5% – 3% of the contract amount. You can read more details about Performance Bond Costs.

Contractors purchasing SDI must go through underwriting with the SDI carrier. This typically involves providing Audited Financial statements, loss history, Subcontractor data, risk management plans and an application.

A second part of underwriting is the Subcontractor pre-qualification that must take place in order to use SDI with most Insurance companies. The General Contractor purchasing the SDI policy must either have an internal team prequalifying contractors in the program or use a third-party vendor.

This additional cost and time are usually significant and should be carefully examined for any contractor considering the use of SDI.

In order to obtain a performance bond, a contractor must be pre-qualified by a third-party surety bond underwriter. Performance Bond underwriting is based on a Contractor’s financial ability to complete the work, their capacity to complete the work and the underwriter’s analysis of the Contractor’s overall character. These together are referred to as the 3Cs.

Unlike insurance performance bonds are written under the assumption of no losses. Therefore, a Surety bond underwriter would not provide a performance bond to a contractor unless they believed the contractor was qualified and capable of completing the contract.

SDI is a product to protect General Contractors or Construction Managers. The policy does not typically protect other parties such as the project owner, Subcontractors, or material suppliers.

It’s important for project owners to understand that if the general contractor has issues on the project, there is no protection in SDI to ensure completion. There is also no protection ensuring that the GC or CM will pay their bills and that the project will be free of mechanic’s liens.

Likewise, Subcontractors and materials suppliers have no guarantee of getting paid by the general contractor having an SDI policy in place.

This is a product disadvantage when compared to performance bonds.

A performance bond protects the obligee on the bond. That could be the project owner or it could be the General Contractor if a Subcontractor is the Principal on the bond.

However, at no additional cost, a performance bond can be combined with a Payment Bond. The payment bond ensures that subcontractors and material suppliers are paid on the project, giving them valuable protection. This also protects the project owner by ensuring the project will be free of mechanic’s liens.

A Dual Obligee Rider may also be added to a performance bond. This rider extends the bond’s benefits to another party such as a lender.

SDI is meant to be purchased by large General contractors and construction managers. Usually, a contractor needs to have $50 million or more in revenue to qualify. However, that is still on the small side with most SDI carriers, and some require $150 million or more in subcontractor expenses to qualify.

Additionally, the contractor needs to have a very strong balance sheet to be able to pay the SDI premiums and absorb the large deductibles.

Any contractor that can qualify can purchase a performance bond. Most contractors can qualify for a $1 million performance bond by just having good credit. Other programs such as the SBA Bond Guarantee Program, funds control and collateral help make almost any contractor be able to qualify.

SDI is a relatively new product over the last twenty years. This can be a benefit as more Insurance companies develop product offerings. A listing of some companies currently offering SDI is below:

It can also be negative in that case law for SDI is still relatively new.

Performance Bonds have been around for a very long time. Case law is well established on both a federal and state level.

Unfortunately, surety has also become somewhat of a stale industry. Innovation and new products are lacking.

Both Subcontractor Default Insurance and Performance Bonds have advantages and disadvantages. Many of the biggest and best contractors utilize both products. All parties should understand the use of the product before signing a construction contract that involves either one.

Axcess Surety is a leading expert in performance bonds and construction. Contact us anytime for additional information.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.