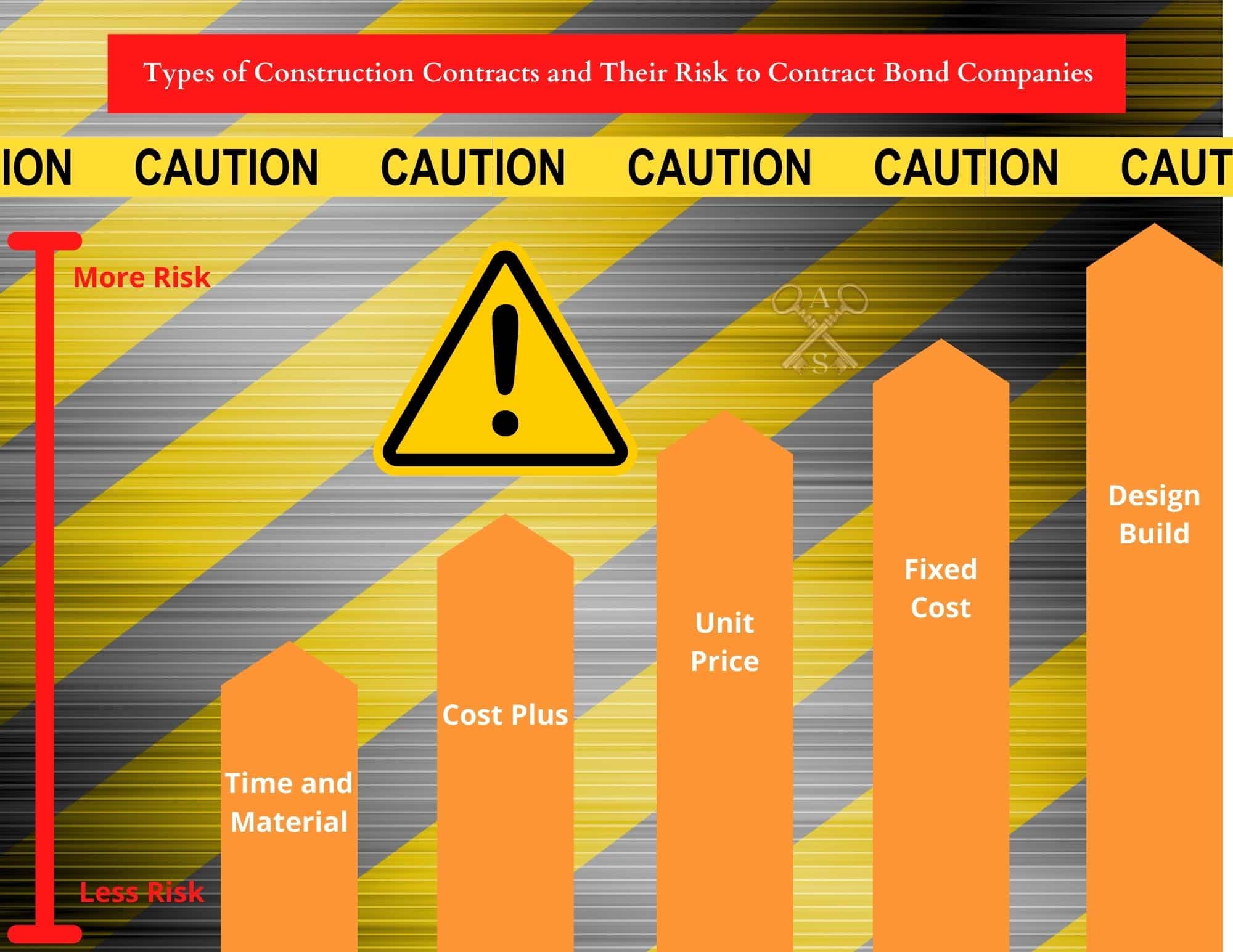

Understanding the types of Construction Contracts are important to contract bond underwriters and should be understood by contractors as well. Each carries a different level of risk. Read more about the type of construction contract below and how contract bond underwriters view them.

A Fixed Price Contract or Lump Sum Contract is the most common type of construction contract. In a Fixed Price Contract, a contractor estimates the costs to complete the project and then adds markup for the contractor’s overhead and profit. The contractor then submits the bid to the owner directly or through a bid letting. The Owner expects to pay the fixed amount to complete the project and no more.

The contractor under a fixed price contract takes on the financial risk and reward of the project. If the costs are more than the estimates, the contractor will make less profit than anticipated or even lose money. If the costs are less, the contractor could recognize additional profits. Estimating construction projects is difficult. Contractors must often predict the future of weather, labor markets and material prices. This is especially challenging in the current environment. This can lead to significant risk and losses that cannot be passed back to the Owner under a Lump Sum Contract.

Fixed Price Contracts are also the most disputed type of construction contract as the expectations of Owners and Contractors are often very different. Poor designs, vague specifications and contracts can all lead to disagreements. Additionally, under a Fixed Price Contract, any changes to the contract are expected to be addressed through proper change orders which are agreed to and signed by both parties. However, this is frequently a cause of disputes and even contractor failure. Contractors who are often excited for additional profit, perform the work and incur the cost before the change orders are signed. Unapproved change orders often lead to losses for the contractor. These often show up as Underbillings on a contractor’s balance sheet. Contract Bond underwriters heavily scrutinize underbillings, and for good reason. Read more about underbillings here.

To ensure a contractor completes the project for a specified price, Owners often require performance bonds and payment bonds from the contractor on fixed price contracts. The performance and payment bonds provide a third-party guarantee to ensure that the project will be completed according to the contract and agreed upon price and that subcontractors and material suppliers will be paid. Even though they present more risk, Surety Bond Companies like Fixed Price Contracts. They can accurately estimate their maximum risk on each project and provide surety credit accordingly. Just as important, surety bond companies have many years of experience handling fixed price contracts and case laws are very established for these contracts. Other lenders often like fixed price contracts as well. It can make getting project financing easier. Owners often like lump sum contracts as they know their maximum cost upfront. However, fixed price contracts can be very risky to contractors. In fact, many large contractors have gotten out of the fixed price contract market after large losses. Lump sum contracts are most appropriate for projects that are well defined.

Unit Price Contracts are priced by a quantity of work performed during a project instead of a fixed amount. A contractor provides the Owner a price for specific quantities of work. Examples include pricing utility lines by the linear foot or excavating soil and rock by the cubic yard. The final contract price is determined by the amount of work performed. Unit price contracts are appropriate when the quantity of work is hard to estimate up front. On the other hand, unit price contracts are rarely used for buildings and structures. Unit Price Contracts make it easy for Owners and Contractors to start projects with routine tasks.

Surety bond underwriters look favorably at unit priced contracts. If the contractor’s estimates are good, they can significantly reduce the default risk for the contractor and the contract bond company. They also allow both Owners and surety bond underwriters to benchmark the Contractors bid price with industry standards. These standards are published yearly by many reputable companies. Some contractors incorrectly assume that there is no risk to Unit Price Contracts. Fuel, labor, material, and weather are still unpredictable. Additionally, Owner abuse could be a problem in Unit Priced Contracts if the quantity of work significantly exceeds the expected scope. Many contracts limit the quantities to a percentage above the estimate such as twenty percent. A bad unit price can add up to losses for a contractor and their surety bond company as quickly as a fixed price contract. For example, an excavator who poorly estimates his cost per linear foot may end up with a larger loss than they would have on a fixed price contract.

Costs Plus Contracts are an agreement where the Owner agrees to reimburse the Contractor for agreed upon project costs PLUS a fee for the contractor’s overhead and profit. The fee can be a percentage of the contract or a fixed fee, which is more common. Usually the Contractor still gives the Owner an estimate of the project up front. Then as work is performed, the Contractor submits approved costs for reimbursement by the Owner.

It is very important in Cost Plus Contracts to define what is reimbursable by the Owner. Common items are Performance and Payment Bonds, job materials, subcontract costs, building permits, equipment, etc. However, it is important to negotiate the Contractor’s costs as this can be a point of contention. Examples include the Contractor’s supervision, use of Contractor’s owned equipment, vehicles, insurance, etc. Are these project costs or part of the Contractor’s overhead? These things should be negotiated up front to avoid disputes.

One of the biggest risks to Owners in a Cost-Plus Contractor is that there is very little incentive to keep the costs down. By reimbursing costs and giving the Contractor a set fee, the Owner takes risk of potentially significant cost overruns on the project. As a way to protect themselves from the risk, many Cost-Plus Contracts include a Guaranteed Maximum Price (GMP). The Guarantee Maximum Price is the maximum the Owner will have to pay under the contract which shifts project risk back to the Contractor. Usually when there is a Guaranteed Maximum Price, there is also an incentive for the Contractor. For example, an Owner may share the savings when a project is completed below the GMP. Another alternative is for the Owner to give the Contractor an incentive bonus for completing the project on time and within budget.

Cost Plus Contracts are ideal for Contractors and their contract bond companies because they significantly reduce the risk of default or payment issues on a project. In fact, if a contract is Cost Plus without a Gross Maximum Price, most surety bond companies do not even count the project against a Contractor’s backlog for surety bond capacity. These types of projects rarely require Performance Bonds or Payment Bonds.

Conversely, if the project has a Gross Maximum Price, the surety bond company must count it toward a Contractor’s program. These projects do carry risk of default by the Contractor and the Owner often does require Performance Bonds and Payment Bonds on these types of projects to guarantee that the Contractor will not exceed the maximum price.

It is important to note that Owners and General Contractors often require performance and payment bonds from subcontractors on Cost Plus Contracts even when there are no Contract Bonds between the Owner and General Contractor. Because the Owner is absorbing the cost of subcontractors, they want to make sure the subcontractor performs according to their contract. This is a way for Owners to reduce their risk of cost overruns on a Cost-Plus Contract.

Time and Material Contracts (T&M) are an agreement between a Contractor and Owner where the Owner agrees to pay the Contractor a set price for time spent on the project plus any materials the Contractor uses. Usually the Contractor gives the Owner a set price whether by the hour, day, etc. that incorporates the Contractor’s costs and profits. Time and Material Contracts are appropriate when bidding and pricing each project would not be cost effective. Often these contracts involve maintenance. An example may be an Asphalt Contractor filling potholes and repairing asphalt. Each individual repair may be insignificant so the Contractor charges Time and Material.

Time and Material Contracts almost never require performance or payment bonds. These contracts present the least amount of risk to a Contractor and the most amount of risk to the Owner. As such, these contracts are welcomed by surety bond underwriters. Time and Material Contracts are also not counted against a contractor’s backlog and surety bond capacity.

Design Build Contracts are usually a single contract where the contractor acts as both the contractor and design professional. Design Build contracts are said to reduce time and costs, while improving communication. You can read more about Design Build Contract and Contract Surety Bonds by visiting this page.

Design Build Contracts are considered to have more risk by contract bond underwriters. That is because the contractor carries the design risk as well. A contractor could build everything correctly and pay all their bills on the project but still be involved in a performance bond claim due to fault design work.

Any of the construction contracts listed above can be either “Hard Bid” or “Negotiated” with the exception of Cost Plus Contracts. Cost Plus Contracts are almost always a Negotiated Contract.

Hard Bid Contracts occur when a contract is won by bidding against other contractors for a project specification and having the lowest price. Hard bid contracts are common and often required in public work. Because of The Federal Miller Act and Little Miller Acts, these projects usually require a contractor to provide Performance Bonds and Payment Bonds when they are awarded the contract.

Hard Bid Contracts carry more risk for a contractor and their contract bond company. Because of the competitive nature of the bidding process, the contractor often can not put too much cushion in their bid to cover mistakes and delays. The owner normally dictates the terms of these contracts and the contractor must usually accept those contract terms. This can lead to disputes and possibly litigation. Also, contractors under a hard bid usually have very little ability to go back to the Owner and get compensated for any cost overruns or delays.

Although most public work is hard bid, some new specifications are adding language to allow some flexibility in contractor selection. Common languange may say that “the project will be awarded to the lowest responsible bidder.”

As their name implies, negotiated contracts are when a contractor works directly with the Owner or Owner’s Representative to come to an agreement on contract price. The contract also gets the opportunity to negotiate with the owner on contract terms which can make these contracts less risky for both the contractor and their contract bond company.

Understanding Construction contracts is an important part of reducing a contractor’s risk and getting construction bonds. Contractors and their contract bond companies should understand the potential risks of each contract before signing it. The wrong contract could result in a bond claim or even put a contractor out of business. When in doubt, an attorney versed in construction may save the contractor time and money later.

Axcess Surety Bonds has a team of construction experts. Contact us anytime for advice on construction contracts and how to get contract bonds for each.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.