Underbillings and Overbillings are important to all contractors and contract Surety Bond underwriters. Learn more about what they are and what underwriters look for in determining a contractor’s bond capacity.

Most contractors should be using the Percentage of Completion (POC) method of accounting. This is the most accurate method of construction accounting and creates both Underbillings and Overbillings. You can read more about the Different types of financial statements here.

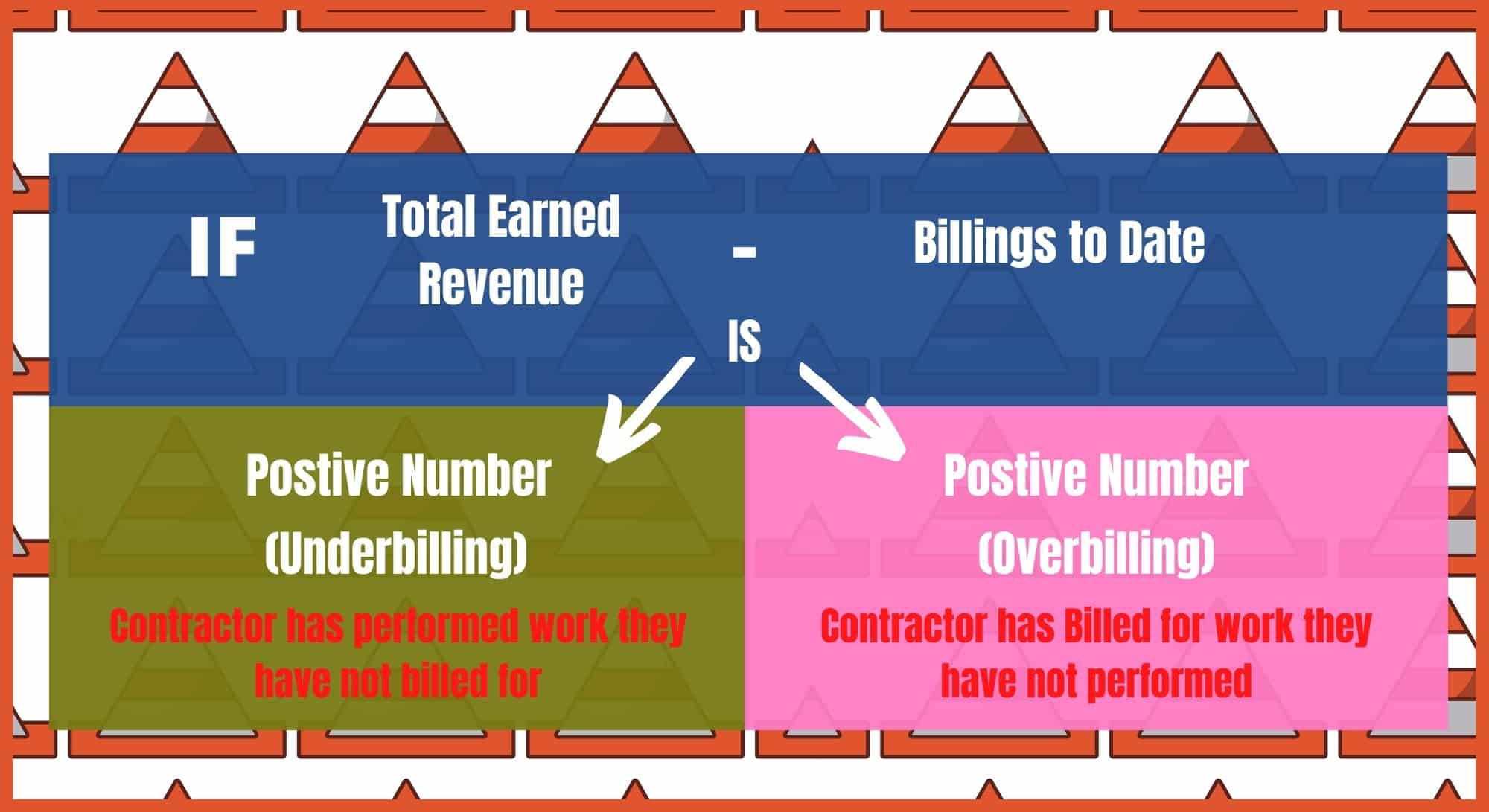

Underbillings are an industry name for Costs in Excess of Billings on Uncompleted Contracts. Simply put, they are revenue that a contractor has theoretically earned but not yet billed. For example, if a project is 50% complete but a contractor has only billed for 40%, the project is 10% underbilled.

The formula for calculating underbillings is:

[Total Cost Incurred to Date + Gross Profit Recognized to Date] – Total Amount Billed to Date.

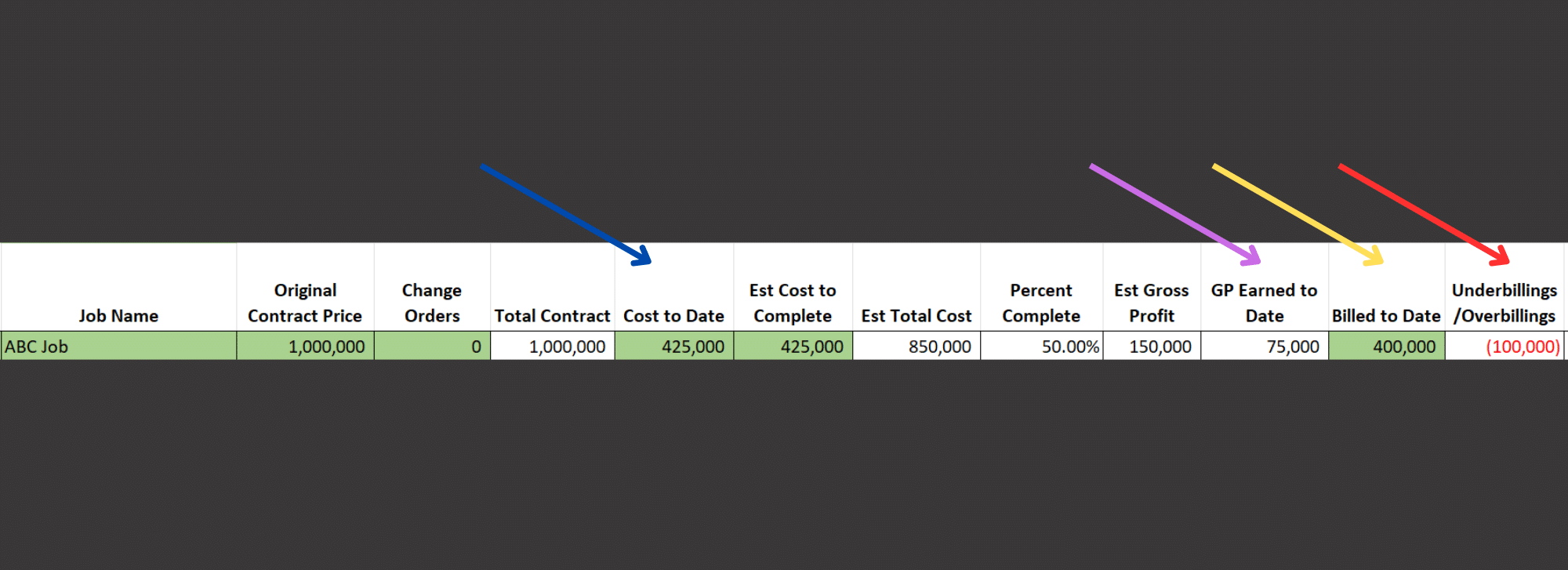

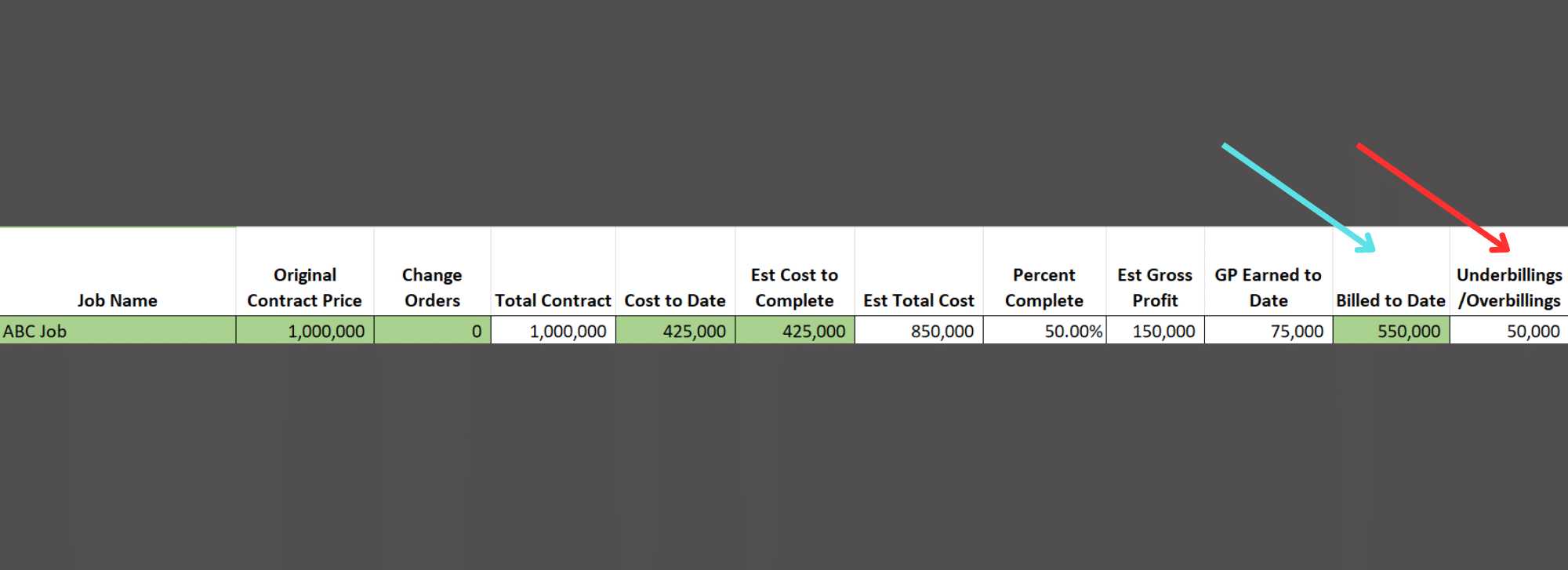

Here is an example. Suppose a contractor has a project valued at $1,000,000 with an Estimated Total Cost of $850,000 and Estimated Gross Profit of $150,000. The project has incurred Costs to Date of $425,000. Using the Cost-to-Cost Method (Estimated Total Cost / Cost to Date), this project is 50% complete, meaning that we have also earned 50% of the profit. Therefore, the Gross Profit Earned to Date is $75,000. In this scenario, we have billed $400,000 on the project to date. Using our underbilling formula we add the Costs to Date of $425,000 with the Gross Profit Earned to Date of $75,000. This equals $500,000 which is the Total Earned Revenue on this project. We then subtract the Billings to Date of $400,000 from the $500,000 and we get $100,000. We have a $100,000 underbilling.

If you consider the example above, the project is underbilled by $100,000 because we have earned $500,000 of revenue on this project but we have only billed for $400,000.

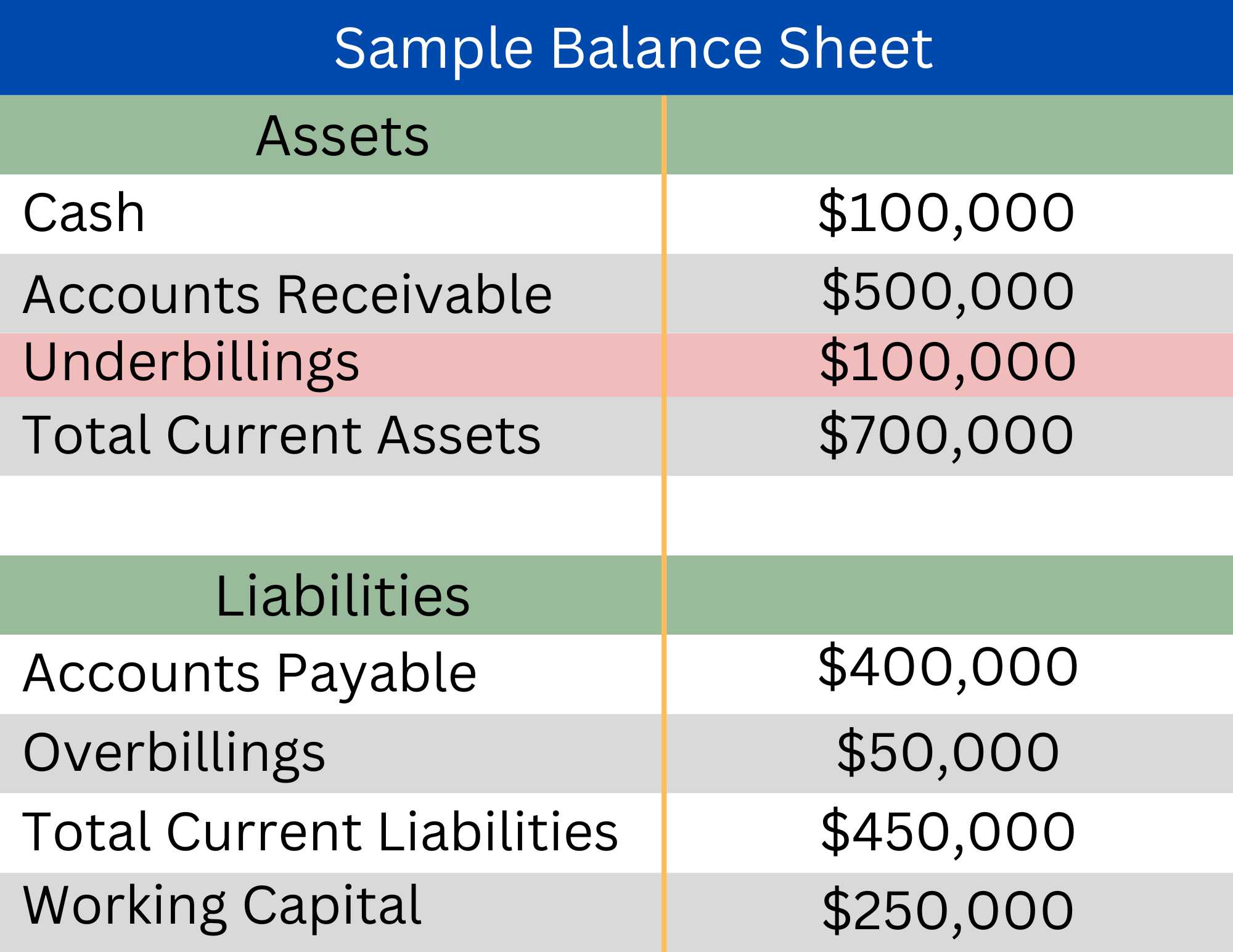

Underbillings show up on a contractor’s Work in Progress Report. This report should tie back to a contractor’s balance sheet where Underbillings appear as a current asset. Underbillings are a Current Asset because in theory, they should be revenue that the contractor can bill for and collect in the future.

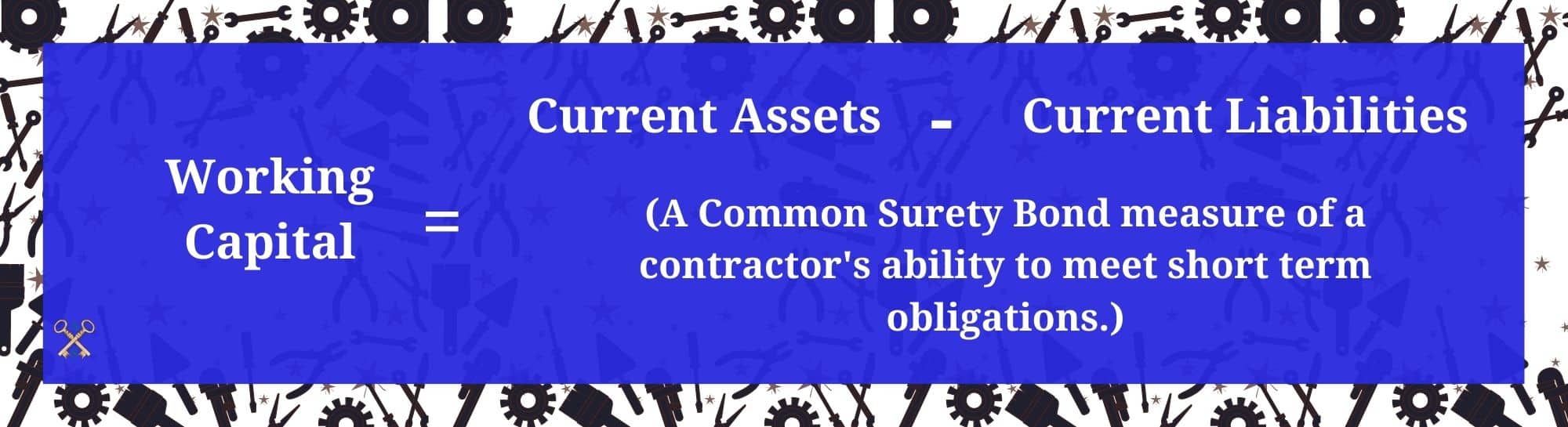

Many contract surety bond companies base a contractor’s bond capacity as a multiple of working capital. Working Capital is calculated by taking Current Assets and subtracting Current Liabilities.

In theory, because it’s a Current Asset, more underbillings should increase working capital and therefore surety bond capacity. However, this is almost never the case. You can see how Underbillings show up on a balance sheet and their relation to working capital in the sample balance sheet below.

Because we only have one project, our underbillings on the balance sheet only show the $100,000. In reality, the amount showing up on the balance sheet would be to total underbillings for all contracts in progress.

Contract Surety Bond companies are skeptical of underbillings because they often turn into losses. From a practical standpoint, underbillings often appear when there is a project dispute, a poor estimate, or bad billing practices.

Underbillings often happen when there is a dispute. The contractor submits a change order for work that has been done but cannot bill for it. This creates an underbilling. Contractors should ALWAYS have a signed change order in hand before doing work outside the contract.

For this reason, contract bond underwriters will closely monitor underbillings on a particular project. If the Underbilling remains for more than a billing cycle or two, most surety bond underwriters will assume it’s a loss, and remove it from their analysis.

Underbillings can also occur when a project was estimated improperly. For example, a contractor may realize they have significantly more cost than originally estimated, but the contractor may be unable to bill for those costs under the contract.

Underbillings also show up when a contractor has bad billing practices. If a contractor has earned revenue that is not in dispute, the contractor should be billing for it.

Constant underbillings are a sign that a contractor has poor accounting systems in place, and this is a major red flag to surety bond underwriters. Contractors often have bonds claims and go bankrupt when they have bad systems in place.

There are situations when Underbillings are justified. One example is when a contractor is not allowed to bill for material or equipment until it is installed.

Certain trades also tend to have more underbillings. However, these underbillings should generally be small and billed quickly.

Overbillings are an industry term for Billings in Excess of Costs on Uncompleted Contracts. Simply put, these are revenues that a contractor has billed for, but that they have not yet earned. For example, if a contract is 50% complete and the contractor has billed for 60%, the project is 10% overbilled.

The formula for Overbillings is: Total Billings to Date – [Cost to Date + Gross Profit Earned to Date].

Using our example from earlier, let’s assume that instead of the $400,000 Billings to Date, we had actually billed $550,000 instead. Everything else stayed the same. Our Work in Progress Report would look like this:

Our project is now overbilled by $50,000. Using our formula for overbillings, we see that $550,000 has been Billed to Date. We still have Costs to Date of $425,000 and Gross Profit Earned to Date of $75,000 and we add those two together to get $500,000. We subtract this number from our $550,000 Billed to Date number and we get an overbilling of $50,000. This amount is an overbilling because we have billed more at this point in time than we have earned from our costs and profits.

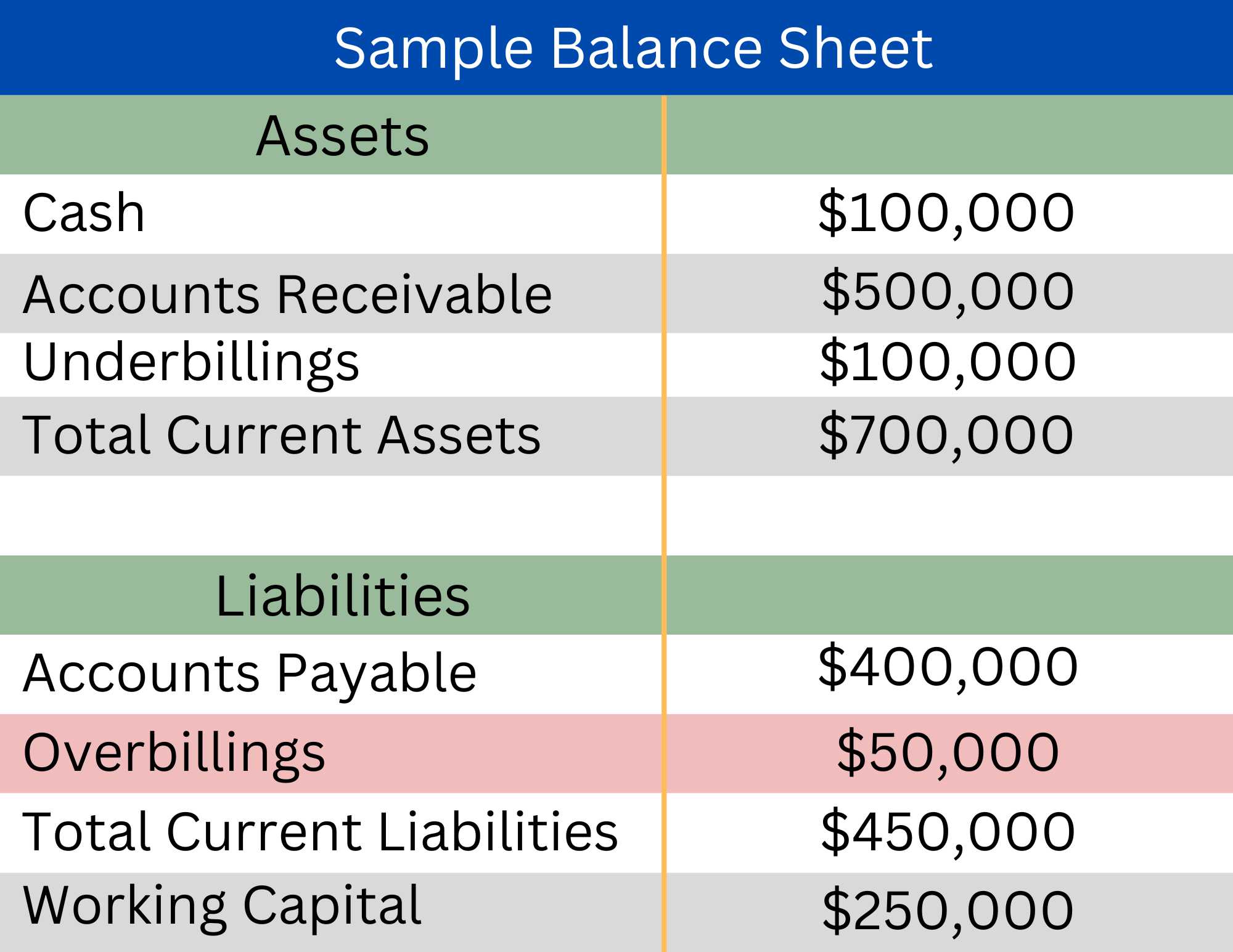

Overbillings also show up on a contractor’s Work In Progress Report and should tie back to the Contractor’s balance sheet as a Current Liability. Overbillings are a Current Liability because the contractor has billed for costs and earnings on work they have not completed yet. This work will need to be completed in the future and the contractor will not be able to bill for the costs at that time.

Below shows how overbillings appear on a contractor’s balance sheet and their relationship to working capital. In this example, we only have one project. In reality, the amount showing up on a balance sheet would the total overbillings for all projects under construction.

Most contract surety bond companies view some Overbilling as a positive. It is a best practice to stay slightly ahead of Billings on a project. In fact, an accepted industry practice is to “front load” a contract to cover mobilization, insurance and performance bond costs, etc. Front loading is the process where contractors shift their schedule of values to be higher in the early stages of a project to cover upfront expenses and improve cash flow through the early parts of the project. Front loading is generally an accepted practice IF the larger early billings are reasonable. Front loading will create an overbilling.

Overbillings can be a problem for contractors though. Bond underwriters will want to make sure that a contractor has enough cash and account receivables to offset Overbillings. This is because the contractor will have a cash outflow later in the project. Not having enough cash and receivables to offset Overbillings is a sign of cash flow troubles to come.

While being slightly overbilled on a project is acceptable, job borrow is not. Job Borrow occurs when a contractor uses revenue from one project to cash flow another project.

Pure Job Borrow occurs when a project is overbilled by more than the project’s remaining Gross profit. Job Borrow is often a sign of cash flow issues to contract bond underwriters and other lenders.

Learn more about underbillings, overbillings and how surety bond companies look at a Contractor’s Work in Progress Report here.

Every contractor should understand Underbillings and Overbillings. Accurate accounting and timely billing practices are vital to the success of any construction company. These practices are also essential to contractors needing contract bonds such as bid bonds, performance bonds and payment bonds. Contractors may use our free WIP Report here to help them track projects and billings.

Contact Axcess Surety anytime for best practices and help with all bond needs.

Other Frequently Asked Questions

An underbilling in Percentage of Completion Accounting occurs when a contractor has billed less on a project in a period than they have earned. For example, a contractor has earned 50% of the project revenue but only billed for 40%. The project would be 10% underbilled.

An overbilling in Percentage of Completion Accounting occurs when a contractor has billed for more than they have earned on a project for a given period. For example, a contractor has earned 50% of the project revenue but has billed for 60%. The project would be 10% overbilled.

The contractor has billed for work that has not been completed and will have costs when they do complete the work that they will not be able to bill for again. Therefore, an overbilling shows up as a Current Liability on a balance sheet.

The contractor has performed work that has not been billed and should be able to bill and collect that revenue later. Therefore, an underbilling shows up as a Current Asset on a balance sheet.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.