Financial Statements are essential for contractors who want to obtain contract surety bonds such as bid bonds, performance bonds, and payment bonds. They are also important for contractors to understand their business and project cash needs. Below are some common types of financial statement accounting methods along with how contract surety bond companies view each.

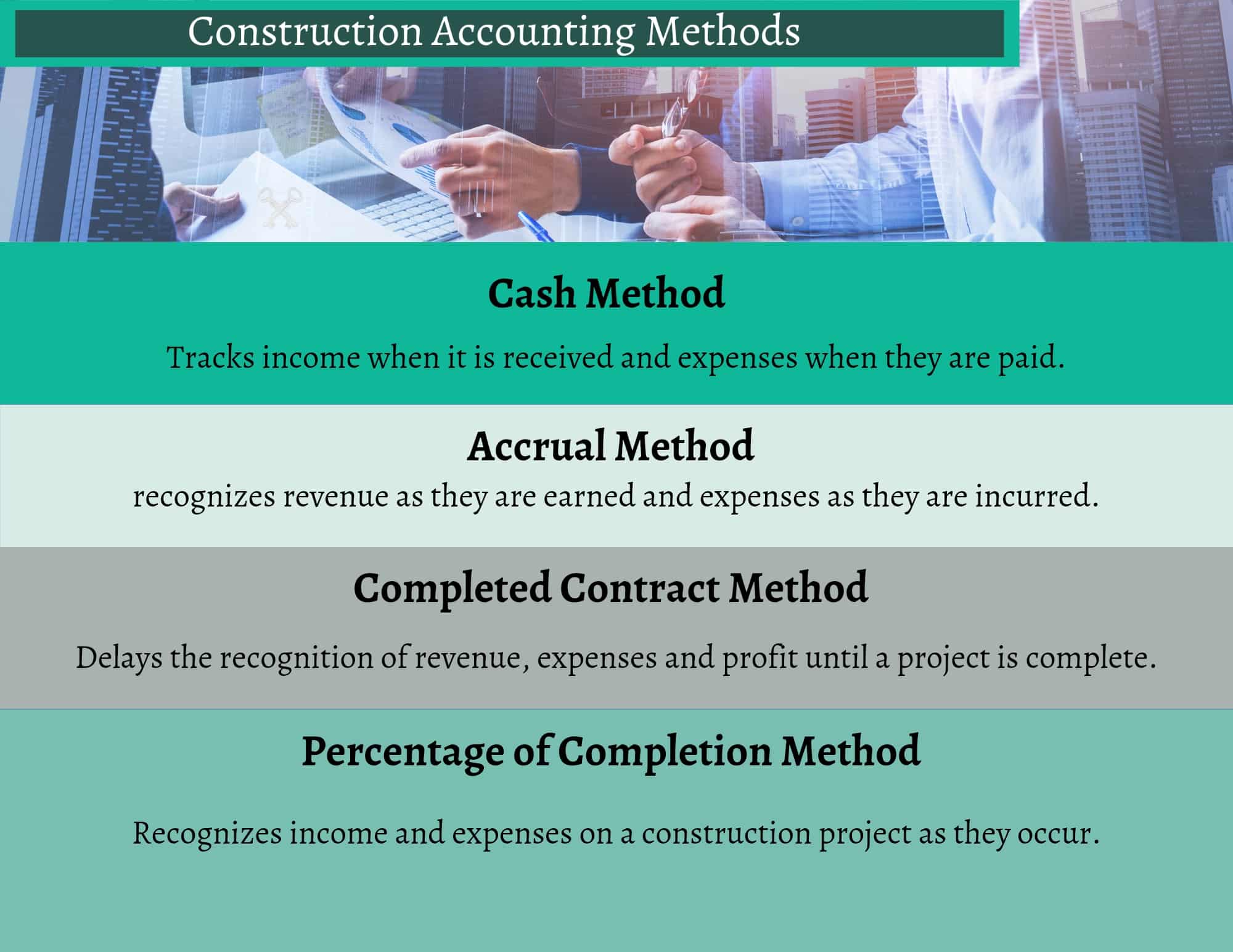

The cash method of accounting is the most basic type of accounting. The cash method tracks income when it is received and expenses when they are paid. This method of accounting is very similar to somebody balancing a checkbook. Cash is recorded as it comes in and as it is paid out. It does not account for accounts receivable or accounts payable. Because of its simplicity, many new and small contractors like to use this method. It can also be tracked very easily without expensive or sophisticated software systems.

Another advantage of the cash method for contractors is that it can have some tax advantages because it allows the contractor to delay the recognition of some income. The cash method also helps a contractor see how much actual cash it actually has since it should match their bank account.

Unfortunately for contractors, the Cash Method is the least preferred method for Contract Surety Bond underwriters and most other creditors. It is the least reliable method to represent the contractor’s actual financial position in most cases. This is because commercial construction projects typically span multiple periods of time and income and expenses are generated before they are collected. Contractors using the Cash Method of Accounting can expect very little surety bond capacity in most cases.

The Accrual Method of Accounting recognizes revenue as they are earned and expenses as they are incurred. With the Accrual Method, it does not matter when the actual cash is received or when the expense was actually paid.

The Accrual Method uses Accounts Receivable and Accounts Payable on the company’s balance sheet to offset the timing. Because income and expenses are tracked as they are earned, the accrual method gives a much more accurate snapshot of the contractor’s operations. The Accrual Method can also be easily tracked by most basic accounting software systems.

A disadvantage of the Accrual Method for contractors is that by itself, it does not give a contractor an accurate position of their actual cash. A company can be very profitable while having no actual cash in their bank to pay their bills. Cash monitoring is vital to all contractors, and running out of cash is one of the biggest reasons for contractor failure and performance bond claims.

The Accrual Method of Accounting is preferred over the Cash Method by construction bond underwriters and other creditors. It is generally viewed as the minimum standard for a contractor to obtain surety bond credit. However, it has limitations from both a surety and contractor standpoint. In its basic form, the accrual method does not track job performance through a Work-In-Progress Report, including overbillings and underbillings. These are vital for contractors and their bond companies.

The Completed Contract Method of construction accounting delays the recognition of revenue, expenses and profit until a project is complete.This method may benefit a contractor by delaying taxes to a later period. However, this method would be a detriment to a contractor if taxes are expected to rise in the future.

The Completed Contract method is most appropriate for small projects with short completion times. It could also be appropriate when estimates are hard to establish.

Contractors needing contract surety bonds should not be using the Completed Contract Method. Even if it is beneficial from a standpoint, it does not give the most accurate portrayal of a contractor’s current financial picture. Construction contracts regularly span more than one reporting period and contract Bond underwriters and other lenders expect more accurate information.

The Percentage of Completion Method (POC) recognizes income and expenses on a construction project as they occur. The POC method requires that a contractor make reliable estimates of a project’s total costs as well as ongoing costs.

Using the POC method, a contractor tracks their open projects through a Work-In-Progress Report. That report shows each project’s billings, costs and expected profit or loss as the project progresses. The report also shows a contractor’s earned income compared to their billings. Differences are shown as underbillings and overbillings on the company’s balance sheet. These are vital for understanding a contractor’s true financial position and getting contract surety bonds.

The percentage of completion method is the most accurate way to account for construction projects. As such, it is also the method preferred by most contract surety bond companies. For contractors wanting the most Surety Bond capacity, it is the only acceptable method for financial reporting.

In addition to the method of accounting, it is important to understand the scope of financial statements and how contract Bond companies view each.

Every contractor needs to be able to generate internal financial statements. Ideally these should be prepared on a monthly basis using the Percentage of Completion Method. These statements should still include a Work-In-Progress report and include under and over billings, along with depreciation.

Many contractors make the mistake of purchasing a cheap accounting software system for their internal reporting. These systems are insufficient for contractors. Not only can they lead to Contractor losses, they typically make it more difficult and costly for a CPA that does the year end statements. Contractors should invest in a good internal accounting system regardless of whether or not they need contract bonds.

Almost all companies are required to file Federal income taxes. Some contract Surety bond companies will use these tax returns in lieu of financial statements. There are some drawbacks though. Typically bond companies that accept tax returns require them to be on an accrual basis. This is a problem for many small contractors who have their returns file on a cash basis.

Secondly, these programs are limited in size. Most contract Bond companies can only write bonds up to $1.5 million based solely on tax returns.

The increase in credit based contract Bond programs has significantly changed financial reporting requirements for small contractors. Contractors needing small bonds used to need at least internal financial statements or tax returns. Now they may be better off using a credit based program. Many credit Based programs offer contract bonds up to $1,000,000 or 2,000,000 and the limits on these programs seems to be constantly increasing.

Compiled financial statements are also referred to as “compilations”. These statements are prepared by an outside accountant. For a compilation, the accountant does not review or audit the information. A Compilation statement also gives no assurances.

Compilation statements range widely in quality depending on the CPA. These statements can be very good quality and include WIP reports, completed contract reports, ageings and other schedules. They can also be a contractor’s internal statements with a CPA letter on top.

The quality of Compilation statements determines the amount of contract Bond capacity a contractor can qualify for. A quality compilation can get bonds upwards of $3 million – $5 million. However, a low quality compilation is often a waste of money and will get a contractor no more bond capacity than an internal statement.

Even a quality Compilation will not be enough for contractors needing regular bonding. They can be a good in between steps as a contractor grows. The risk a contractor faces when getting a Compilation is that their Surety needs grow past the compilation and they may be stuck paying for two statements.

A Review is conducted by a Certified Professional Accountant. During a Review, the CPA uses procedures to investigate a contractor’s financial condition and provide limited assurances to their accuracy and that they are presented according to Generally Accepted Accounting Principles.

A Reviewed Statement should be performed by an experienced construction oriented CPA. A quality Review should include all job schedules, a statement of cash flows, and notes to the financial statement.

A Review only needs to be performed once a year at the contractor’s year end. Internal interim statements are sufficient between the Reviews.

For contract bond purposes, a Reviewed statement is sufficient for most contractors. A contractor can expect to receive up to $50 million in surety bond credit with a Reviewed Financial Statement. Of course a contractor still needs to quantify financially.

An Audited Financial Statement is the best statement a contractor can obtain. During an audit, an auditor analyzes a contractor’s financial statements, and internal controls. An auditor attests to the accuracy of the financial statements and gives assurances that they comply with GAAP.

From a contract Bond standpoint, Audits provide the most contractors with the most bond capacity. Audits also provide a great tool for contractors to understand their companies and manage their risk. Even contractors that do not need an Audit from a surety perspective, often get one as a useful tool for their company. Publicly traded companies are required to have Audits.

Not all CPAs are created equal. Construction accounting is challenging and not many CPAs are good at it. A poor quality statement is often a waste of a contractor’s money. Contract Bond underwriters know what to look for in a quality statement. Poor quality statements hurt a contractor and their bond capacity.

Construction CPAs also understand what contract Bond companies, banks and other lenders are looking for in a financial statement. They can give contractors advice with these stakeholders in mind. Non construction CPAs often try to justify their expense by doing things that may hurt bonding.

Contractors would be wise to select a construction CPA. Friends, relatives or neighbors are usually a poor choice. Good CPAs can be found in construction trade associations and by referral.

Contract Bond companies expect the year end financial statement to be completed within 120 days of the contractor’s fiscal year end. Anything later could hurt a contractor’s ability to get bonds.

As said above, good construction CPAs understand this. They prioritize getting a contractor’s year end statement done. They do not wait for tax filings. This is usually a sign that contractors need to find a new CPA.

Unfortunately, contractors often view financial statements as a hassle that they have to do for bond companies and lenders. Although they are necessary for those parties, quality financial statements should be viewed as a vital tool for the contractor as well.

Contractors often go into Bond claim and out of business because they lose track of projects, profits fade or they fail to project cash flow needs. Having reliable internal controls and financial statements helps identify these problems before it’s too late.

Investing and using good accounting software and internal controls can be time consuming and expensive. Contractors should consider Outsourcing this until they grow to a size that they can hire their own full time people and invest in quality systems. Outsourced CFO services are very reasonably priced and can give contractors financial reporting capabilities that they may not be able to afford to do themselves.

Understanding Financial Statements will help a contractor get contract bonds and improve operations. Axcess Surety can make recommendations and referrals based on a contractor’s unique needs. Contact us anytime.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.