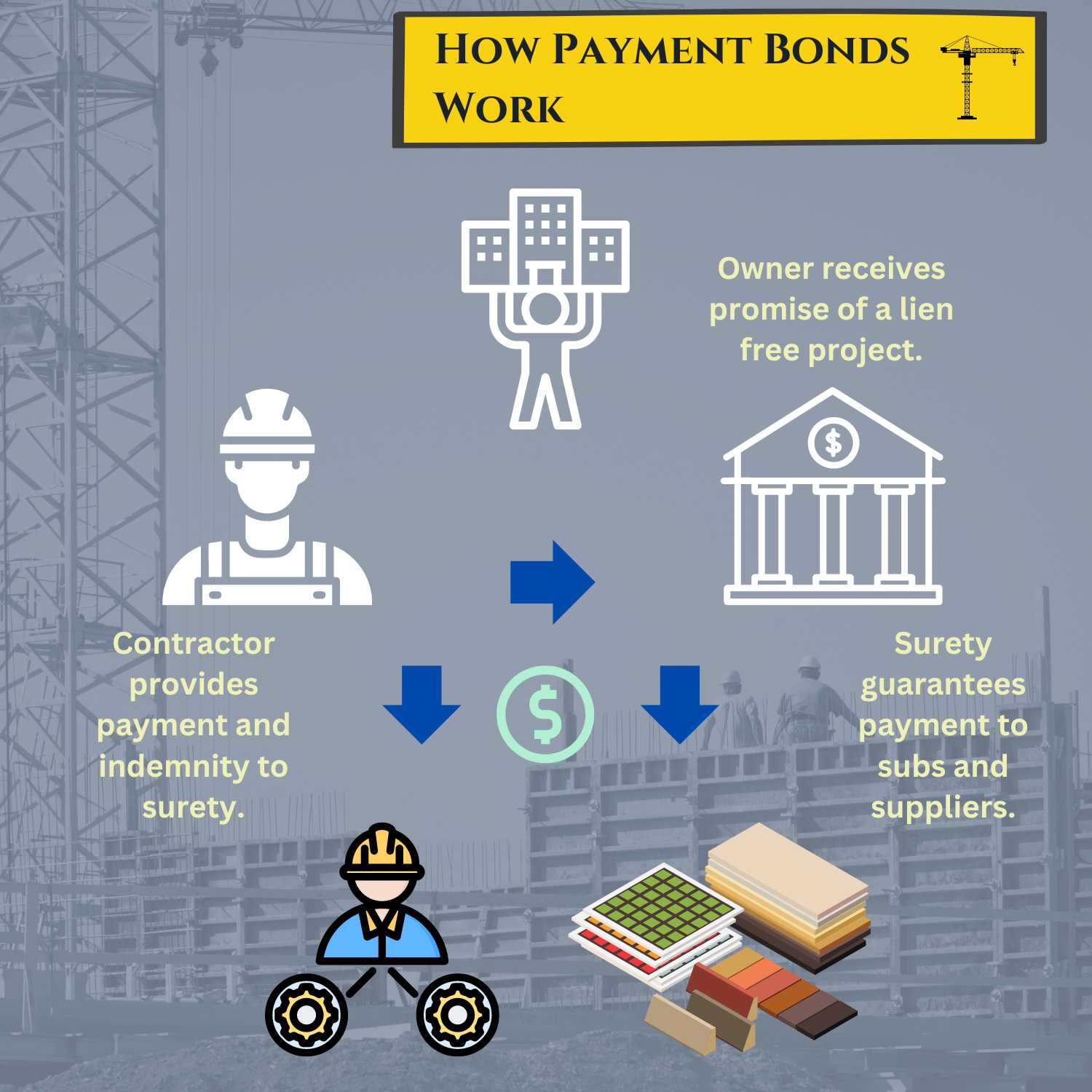

The contractor needing the bond is the principal. The principal pays a third-party surety bond company for a financial guarantee. In exchange for payment and the agreement to indemnify the surety bond company, the surety provides a payment bond to a project owner, or upstream contractor known as the obligee. The payment bond guarantees that the principal contractor will pay certain subcontractors and material suppliers under the contract. This benefits the obligee by keeping the project free of mechanic's liens.

Should the contractor not pay a subcontractor or supplier, they can file a claim against the payment bond. The surety will investigate the claim and pay the claim if necessary. The surety can then go back and seek reimbursement from the principal under the indemnity agreement.

The payment bond provides valuable protection to the owner, suppliers and subcontractors because collecting from a surety bond company may be faster and easier than trying to collect from the principal contractor. This is especially true if the principal is having financial trouble and may be unable to pay their bills.

Payment Bonds are often written together with other Contract Surety Bonds such as Performance Bonds, Bid Bonds, and Maintenance Bonds. Although a Payment Bond can be required by itself, most surety bond companies do not charge a separate premium to write it together with a matching Performance Bond. Therefore, there is no reason for an obligee to not require both on a given project.

Payment Bonds are easily obtainable for most contractors. For simple projects of $500,000 or less in value, a simple credit check is all that is needed. Click here or the button and purchase a payment bond in minutes.

For larger projects, more information may be required such as business and personal financial statements. A surety bond company will also likely run a credit report on the business. Since a Payment Bond guarantees that a principal will pay their bills, it’s important to have a solid track record of doing so in the past. Payment Bonds are a type of Contract Surety Bond. These bonds are underwritten using the 3Cs. These stand for Character, Capacity and Credit.

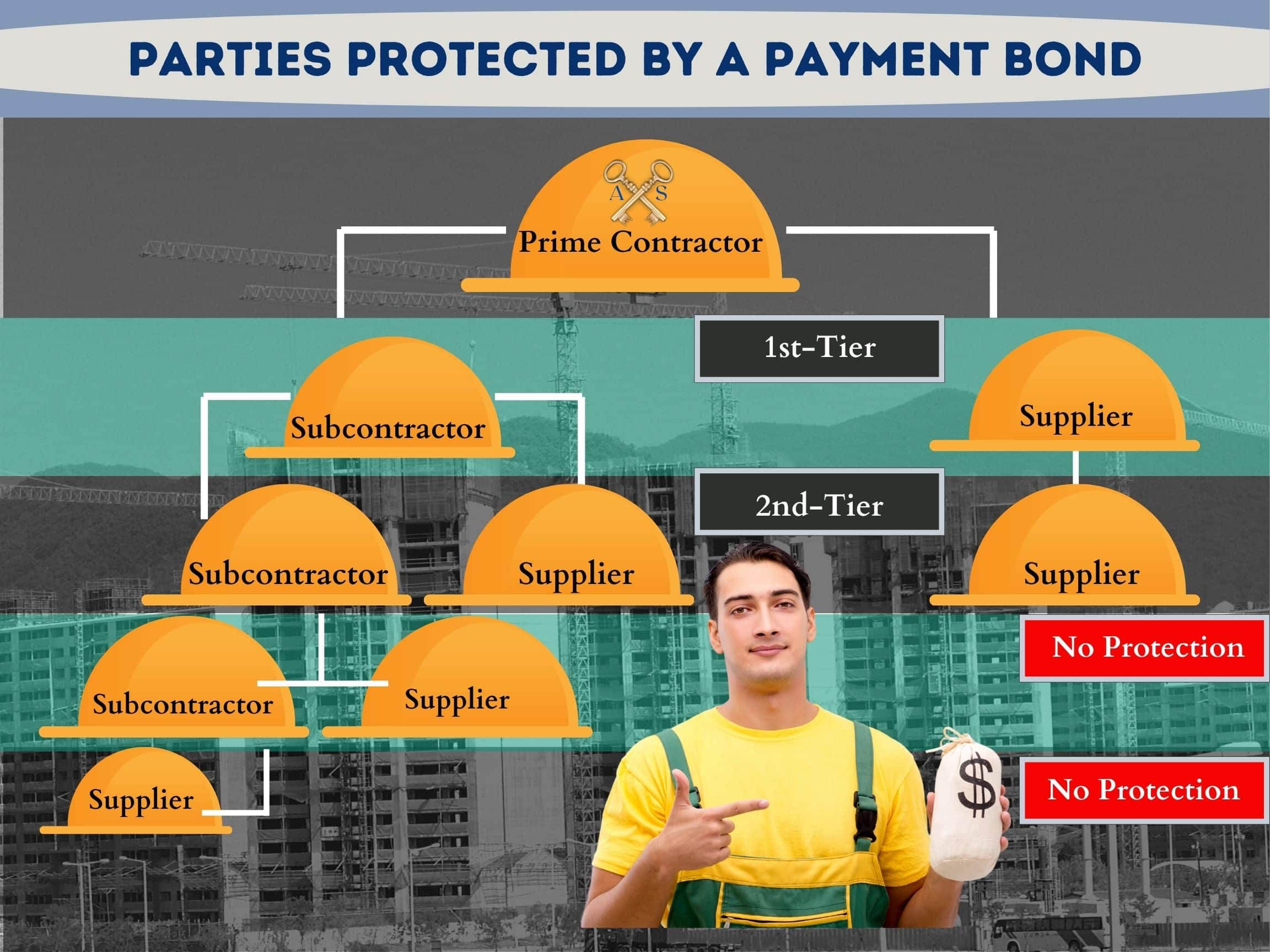

Other potential claimants under a payment bond include those providing professional services to the project including Engineers, Architects and Surveyors.

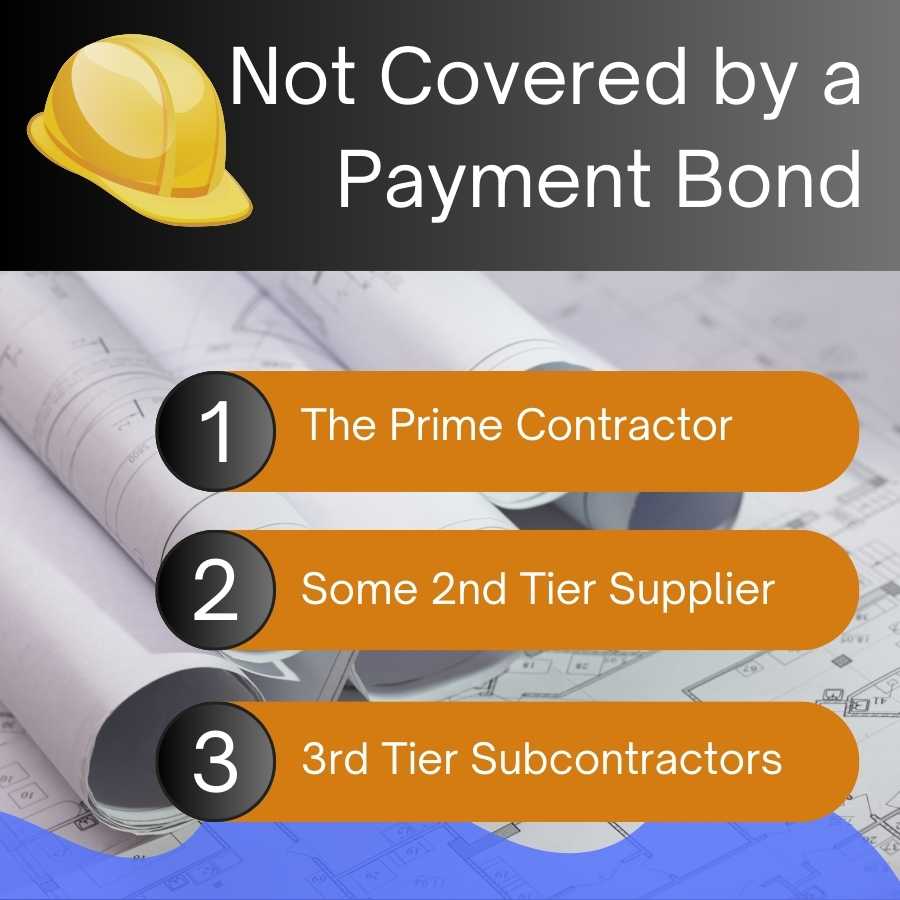

Although payment bonds are great tool for protecting subcontractors and material suppliers, they do have some limitations. Generally, a claimant under a payment bond must meet certain time, and contract requirements.

While Payment Bonds and Performance Bonds are usually written together, they guarantee two very different things. Payment bonds only guarantee that certain subcontractors and suppliers will be paid on a project. On the other hand, Performance Bonds guarantee that a project will be completed according to the contract and at the contract price.

Both payment bonds and performance bonds are normally written for 100% of the contract amount. Because there is only one charge when both bonds are written together, an obligee actually get 200% of the contract amount in protection.

For example, if an obligee requires a 100% performance bond and 100% payment bond on a $1,000,000 project, the principal is only charged once. However, the obligee gets $1,000,000 of protection against claims for non-payment and another $1,000,000 of protection for claims against cost overruns and performance issues.

There are many payment bond forms that can be used. Many states have their own statutory form as well as the Federal Government. There are also many standard forms such as AIA, Consensus Docs, EJCDC. Surety bond companies often have their own proprietary payment bond forms and some contractors do as well. It is important to read the requirements of each payment bond form, especially on private contracts.

Payment Bonds are a valuable tool for protecting contractor and supplier payment rights. Non-payment is a major risk and can cause major turmoil or even business failure. Contact Axcess Surety today to secure a payment bond or for any other surety bond needs.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.