Fidelity Bonds are an important tool to protect businesses and their customers against acts of theft and dishonesty. Learn more about these important bonds, including what they are, and how to obtain them.

A Fidelity Bond provides coverage that protects an organization from theft, and dishonest acts of employees, members, or volunteers. These Fidelity Bonds are often referred to as employee dishonesty bonds or employee dishonesty insurance. Fidelity Bonds were originally three-party agreements, like most surety bonds. However, over the years, they have transformed into two party insurance coverage.

According to FinancesOnline, 49% of businesses suffer from employee theft. A typical employee theft lasts 14 months before it is detected. While larger businesses may be able to absorb the financial impact, small businesses often cannot. I have personally seen the devastation that an employee theft can cause. I had a small contractor have millions embezzled by a trusted employee. The employee was so close to ownership that she even watched their children.

Employee theft can be devastating to a company financially, morally, and can have even broader reputational consequences if the theft is from a customer of the business.

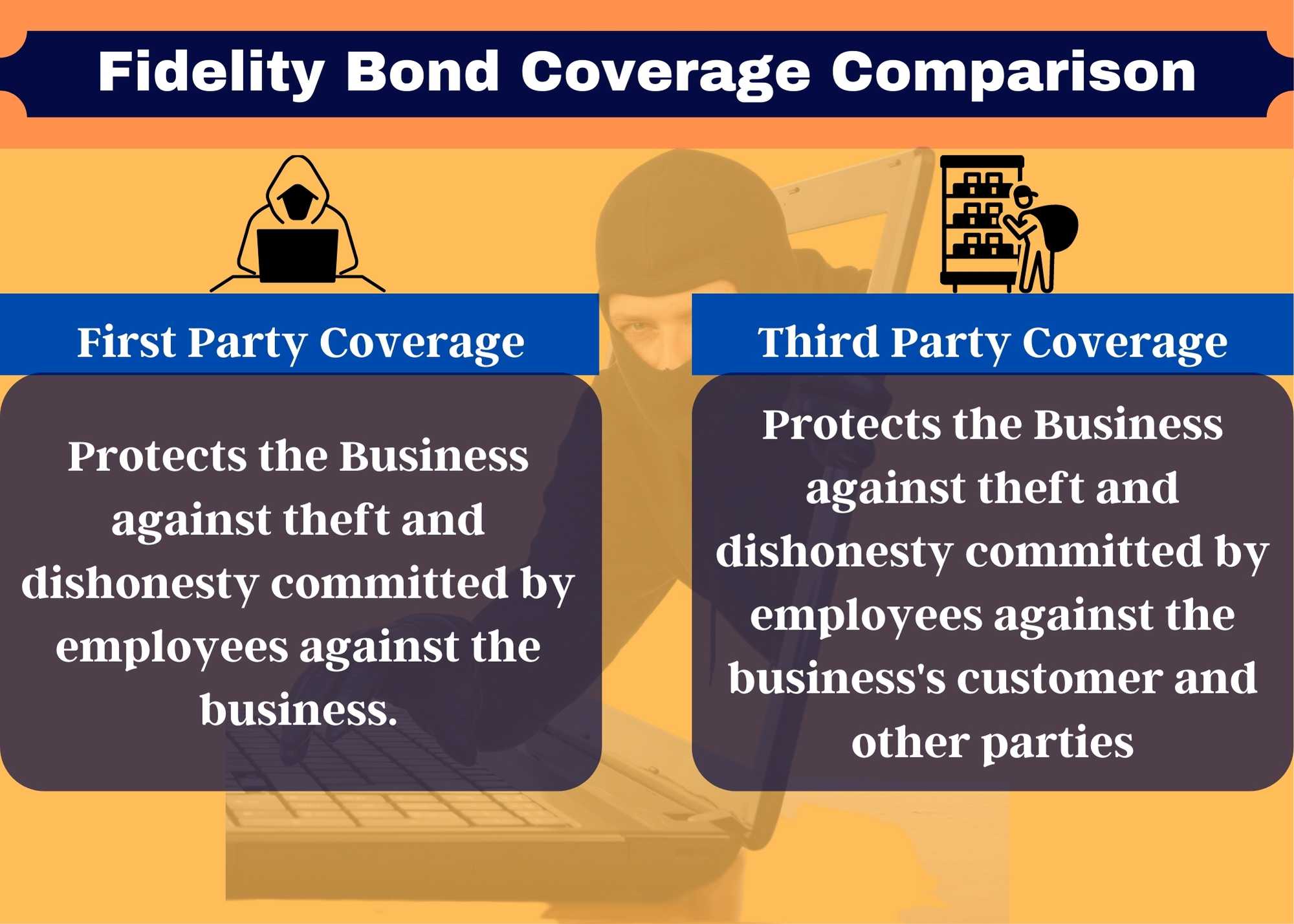

Standard Fidelity Bonds provide first-party coverage. That means the bond protects the Principal on the bond against theft or dishonest acts committed by the Principal’s employees. An example of a First Party claim against a Fidelity Bond would be a CFO that embezzles money from the company he or she is working at. If discovered, the company could make a fidelity bond claim against the bond.

Another popular use of Fidelity Bonds is to protect the customers of the business. This is referred to as Third-Party Fidelity Coverage. An example of Third-Party Fidelity Coverage may apply to a Janitorial Company. These companies frequently have employees in the businesses or homes of their customers. Should an employee of the Janitorial Company steal from the customer, a claim could be made against the Third-Party coverage of the Fidelity Bond.

Most businesses need some type of Fidelity Bond. In fact, the U.S. Department of Commerce attributes a staggering 30% of all business failures to dishonest acts of employees. Theft and dishonest acts can be devasting to a business, its customers and its employees. As mentioned above, businesses that are around customer assets are particularly at risk and certainly need coverage. These third-party Fidelity Bonds are often referred to as Business Service Bonds. Other common Fidelity Bonds include ERISA Bonds and Financial Institution Bonds.

The Employment Retirment Income Security Act (ERISA) is legislation that protects individuals in certain private retirement and health care accounts by requiring minimum protects for these accounts. One of the ways ERISA protects savers in these accounts is by requiring the employer to post an ERISA Bond or coverage in the amount of 10% of the plan’s assets for every person who handles funds or property for the plan. The minimum amount of the ERISA Bond must be $1,000. However, each person’s bond amount does not have to exceed $500,000 for most businesses or $1,000,000 if the plan holds stock of the company in the plan.

For example, a company’s 401k plan holds $5 million in assets and has 3 individuals who handle plan assets. Each individual would need to be covered by the maximum $500,000 in ERISA Coverage.

Businesses should also consider that 10% is the minimum coverage and more should often be purchased. Losses of employee retirements assets would tarnish the company’s reputation and likely put them out of business.

These ERISA Bonds protect savers in the event that someone from the company steals from the plan or acts dishonestly. ERISA Bonds DO NOT protect against financial losses from investment performance.

Because they apply to a government obligation, ERISA Bonds are required to be written by a surety bond company on the U.S. Treasury 570 Circular. However, some Fidelity Bonds issued by Lloyds of London may be accepted.

Another common Fidelity Bond is a Financial Institution Bond. Financial Institution Bonds are required by many companies that handle customer money and investments such as banks, credit unions, broker dealers, private equity, trust funds, and insurance companies.

Financial Institution Bonds can be broad and written to protect a wide range of theft and dishonesty. Common coverage also includes things such as computer fraud, wire fraud and impersonation fraud.

Fidelity Bonds can either be very easy or complicated to obtain depending on the type and size. Many standard commercial insurance policies contain some crime coverage and may even cover some ERISA liability. Many businesses may need or choose to purchase additional amounts.

First-Party Coverage Fidelity Bonds up to $100,000 can be purchased online instantly with little information. Simply click on the Fidelity coverage amount needed on the table below.

| Bond Amount | Instant Purchase |

|---|---|

| $1,000 Fidelity Bond | Purchase Now |

| $2,500 Fidelity Bond | Purchase Now |

| $5,000 Fidelity Bond | Purchase Now |

| $7,500 Fidelity Bond | Purchase Now |

| $10,000 Fidelity Bond | Purchase Now |

| $12,500 Fidelity Bond | Purchase Now |

| $15,000 Fidelity Bond | Purchase Now |

| $20,000 Fidelity Bond | Purchase Now |

| $25,000 Fidelity Bond | Purchase Now |

| $30,000 Fidelity Bond | Purchase Now |

| $40,000 Fidelity Bond | Purchase Now |

| $50,000 Fidelity Bond | Purchase Now |

| $75,000 Fidelity Bond | Purchase Now |

| $100,000 Fidelity Bond | Purchase Now |

Many Business Service Bonds and ERISA Bonds up to $500,000 can be purchased with just a simple application.

More complicated and larger Fidelity Bonds generally require a review of the company’s financial statements. They may also require detailed information on the company’s procedures to prevent theft and dishonesty. Some Best Practices that Fidelity Bond companies look for include:

There are many other practices, but Fidelity Bond companies will want to make sure companies have standards and practices in place to limit losses.

When underwriting Fidelity Bonds, a surety bond underwriter will often want to know the number of employees a company has. More employees increase the risk and cost of the Fidelity Bond as it presents more opportunity for theft and dishonesty.

It is a standard practice that Fidelity Bonds contain a “Prosecution Clause” or “Conviction Clause”.

A Prosecution Clause is a contract provision that requires the Principle to prosecute the person or persons accused of committing theft or dishonesty before the Fidelity Bond will pay a claim.

A Conviction Clause is a contract provision that requires the conviction of the person or persons accused of committing theft or dishonesty before a Fidelity Bond will pay a claim.

Conviction Clauses should generally be avoided. A business has relatively little control over whether conviction will occur. These clauses have been regularly replaced by Prosecution Clauses. Prosecution Clauses can be difficult for a company. In many small businesses, the people that steal are often long-term employees, that are close to management. Even when these individuals steal or commit dishonest acts, it can be difficult to pursue legal prosecution against them.

Fidelity Bond companies view Prosecution Clauses as vital risk management, however, First, key people know that they will indeed face legal consequences if they steal or commit dishonest acts. Secondly, it prevents collusion and fraud between and company and its key employees. For example, without a prosecution clause, two executives could conspire to steal from the company by making an agreement that one will not seek prosecution against the other if one is caught.

The cost of a Fidelity Bond depends on the amount of the bond, the purpose of the bond, and how many employees it will cover. For example, a three-year ERISA Bond cost about 0.25% of the bond amount. Therefore, coverage for $100,000 ERISA Bond would cost about $250 for three years.

Coverage for other Fidelity Bonds can vary. Business Services Bonds generally cost between 0.5% – 2%. Financial Institution Bond cost vary widely depending on the size, financial strength and risk management practices of the company.

Almost all businesses should have some Crime Coverage or Fidelity Bonds in place. Common businesses needing these bonds include Janitorial Services, Non-profit organizations, retail, restaurants, accountants, attorneys, money transmitters, gas stations, home care and residential contractors. However, many other businesses should consider this coverage as well. Anyone with access to cash, payments or record keeping is particularly high risk for an employee dishonesty claim.

As employee theft and dishonesty losses continue to increase, Fidelity Bonds are becoming more necessary for all businesses. Fidelity Bonds are not surety bonds, but they are valuable insurance coverage that should be a part of every company’s risk management.

Fidelity Bonds are actually a type of surety bond. Surety Bonds include three broad categories including Fidelity Bonds, Contract Bonds and Commercial Bonds. Fidelity Bonds protect businesses and individuals from acts of theft and dishonesty.

No Fidelity Bonds are not insurance. They are a type of surety bond. However, many insurance companies can provide similar theft and dishonesty coverage under an insurance policy.

State of California:

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.