Probate Bonds are surety bonds required by a court to ensure that estate of a deceased person is handled properly. There are several different types of probate bonds, and each provides a different type of guarantee, but all ensure that an appointed Fiduciary handles the estate fairly. These probate bonds include:

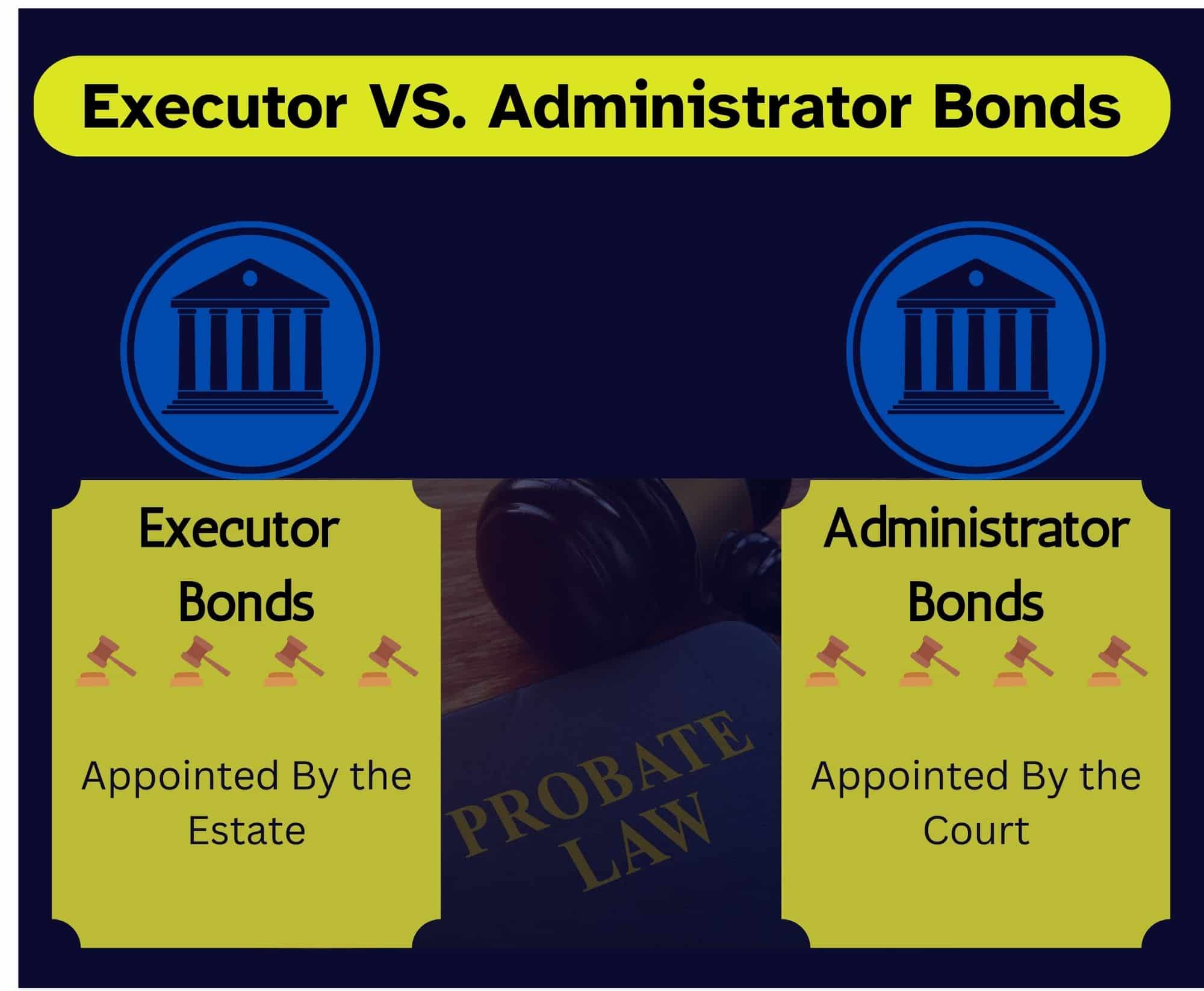

Executor Bonds and Administrator Bonds are very similar. The difference is that Executors are appointed by the Estate. These are referred to as Personal Representatives in some courts. Administrators are appointed by the Court. The duties of both Fiduciaries are similar. They are to collect the assets of the Estate, pay the Estate’s creditors and distribute any remaining assets to the Heirs of the Estate. A key difference is that the Executor is tasked with distributing any remaining assets according to the wishes of the Deceased. An Administrator is tasked with distributing any remaining assets according to local probate laws.

Many Probate Bond Brokers do not realize there is a difference between Executor Bonds and Administrator Bonds. Make sure you are getting the correct bond that is required by the court.

Guardianship or Conservator Bonds are required by the court when the assets of the estate are held for the benefit of a minor or person who may be incapacitated. This person is often called a Ward. The Guardian, or Conservator, depending on the court, is charged with handling the estate’s assets until the person reaches a status to be discharged. For a minor, this could be adulthood. For an incapacitated person, this could be a very long time. The Guardian must be careful to handle the Estate’s assets in a way that is in the best interests of the Ward.

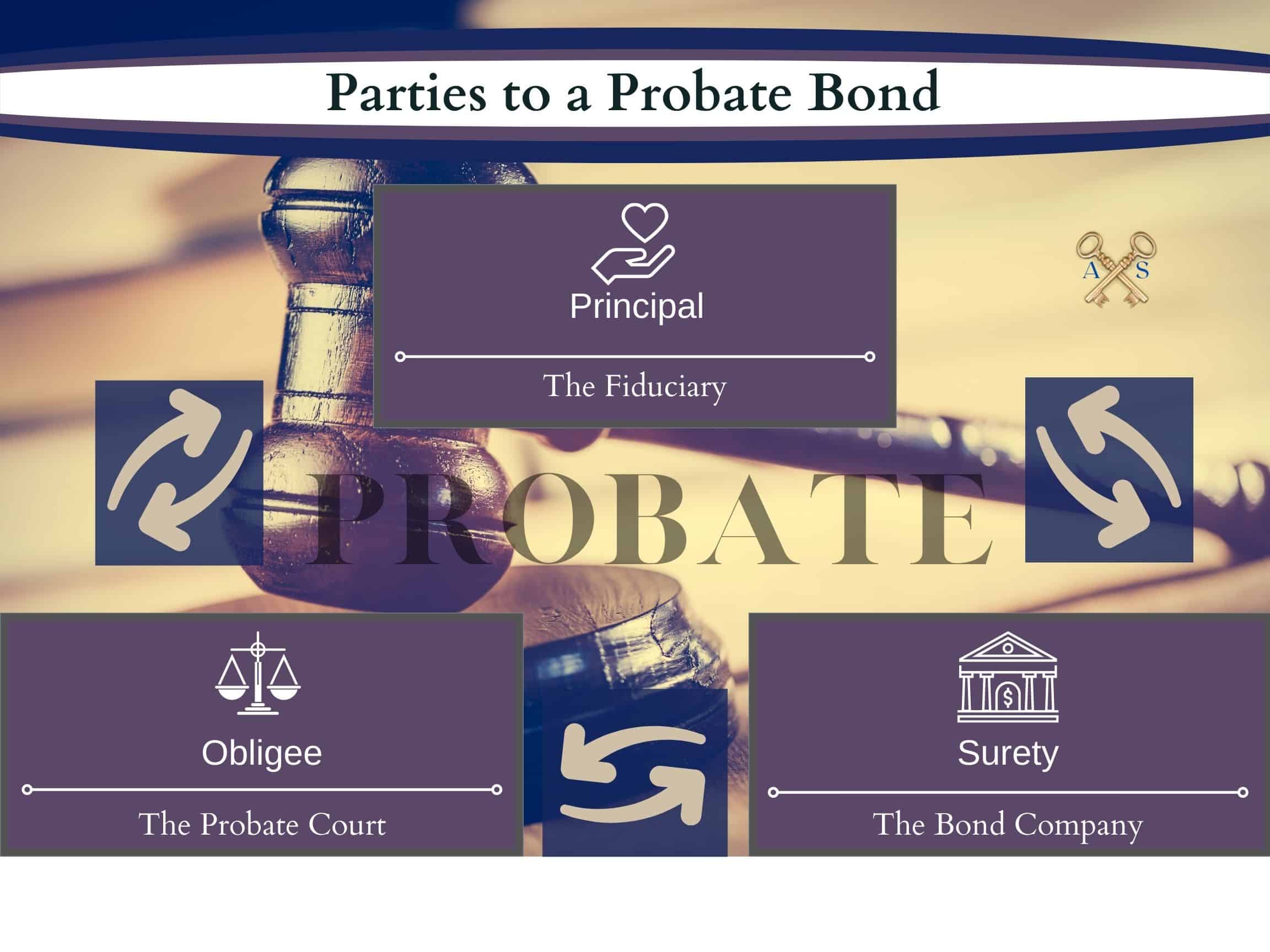

The Principal on Probate Bonds is the Fiduciary of the Estate. The obligee on these bonds is the Probate Court requiring the Bond. The Surety is the Probate Bond Company that is guaranteeing that the Fiduciary will perform in an honest manner that is in the best interest of the Estate.

Probate Bonds are considered risky by surety bond underwriters. Key underwriting considerations are the anticipated length that the Probate Bond and Estate will be open, are any of the assets being disputed, is there an attorney involved, experience of the Fiduciary, controls of the Fiduciary, if there is a business involved and size of the estate.

Larger Estates present more opportunity for error. They also have the possibility to have more disputes and larger opportunities for fraud.

Underwriters look at the controls the principal has in place. For example, is the principal experienced in keeping records? Will they use all checks instead of handling cash? On larger estates, the surety bond company may require controls such as a joint check arrangement.

Probate cases involving businesses are very risky. Unless the Fiduciary has worked in the business, he or she often lacks the skills needed to properly unwind the business and the chance of a dispute increases.

The duration of responsibility is a key consideration in Probate Bonds. An Estate that will be settled quickly is much less risky than a Conservator Bond that may be open for the next 10 years.

Disputes are a major red flag to surety bond underwriters looking at Probate Bonds. Heirs may not be pleased with how an Estate’s assets are being handled. Assets in litigation will require many bond companies to pass or require that the principal post collateral.

Experienced Probate Attorneys that stay involved until the Estate is closed, will make obtaining Probate Bonds much easier. On the other hand, attorneys that are simply performing a transaction create risk for the estate and the surety bond company.

Getting a Probate Bond depends on the size of the estate. Many probate bonds where the estate is $500,000 or less can be obtained with just a credit check of the principal and a review of the court documents. They can often be purchased in minutes by clicking here or on the button below:

Larger Probate Bond cases or those that are more complicated, require the principal to submit a completed application, court documents and in some cases, an Accounting and Inventory of the estate.

Probate Bonds cost between 1% – 2% of the bond penalty per year for every year that the Probate Bond is in place. This is important to understand as the Probate Bond will not be cancelled until the principal provides evidence from the court that the Estate is closed, and the principal has been discharged of their duties. The bond premium will be due each year until the paperwork is received.

The exception to this is if a different Fiduciary is appointed and a replacement bond is accepted by the court. However, the Probate Bond company will require a copy of this replacement before closing the initial probate bond.

Unfortunately, claims are not uncommon on Probate Bonds. Claims can occur in a number of Scenarios.

Although many things can trigger one of the parties above to file a Probate Bond Claim against a Principal, some of the more common causes include:

As you can see, there are many things that could lead to a Probate Bond Claim. Principals on a Probate Bond should make sure they are doing everything in the best interest of the Estate and keep great records to avoid Probate Bond Claims.

Like all surety bonds, Probate Bonds require indemnity. That means that if a claim occurs, the Probate Bond company will investigate the claim. If the claim is found to be valid and the Bond Company makes payment, they will seek reimbursement from the principal. You can read more about indemnity and surety bonds here.

Probate Bonds are common and most of them are very easy to obtain. Click here to easily obtain Probate Bonds for smaller estates. Axcess Surety employs Probate Bonds Experts. Contact us anytime to have your questions answered and to easily and quickly get your Probate Bonds issued.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.