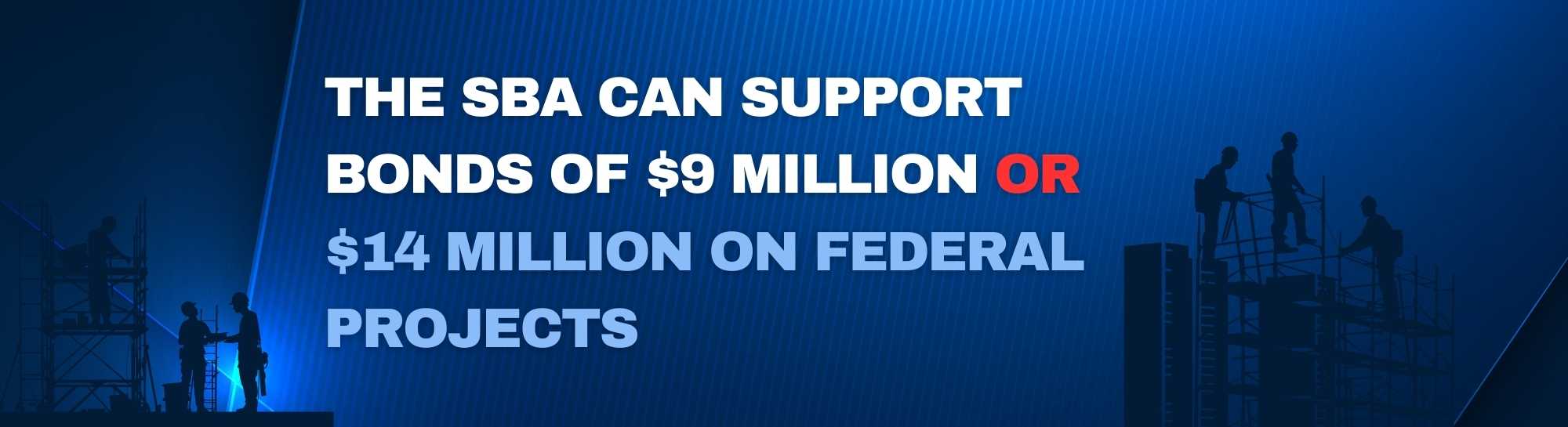

** UPDATE** The SBA Surety Bond Guarantee Program has increased its single bond limits to $9 million and $14 million on Federal Projects effective 2024.

The program was created as a way to help small businesses obtain more work by encouraging Surety Bond companies to write contract bonds for contractors who cannot obtain surety bonds in the standard Surety market.

The SBA acts as a reinsurer for the Surety Bond company writing the bonds. In other words, the SBA reimburses the Surety between 80% – 90% of the loss if an approved contractor goes into Bond claim. This gives the Surety a big incentive to write contract bonds for contractors they would not write otherwise.

The SBA, however, does not write surety bonds directly. It still needs a Surety Bond company to approve the bonds in addition to getting SBA approval.

Performance Bonds, Payment Bonds, Bid Bonds and some Timber Bonds are eligible. Maintenance Bonds are also allowed if they are written with another allowed surety bond.

Not all contract bonds are eligible for the SBA program. The following are not eligible for the program:

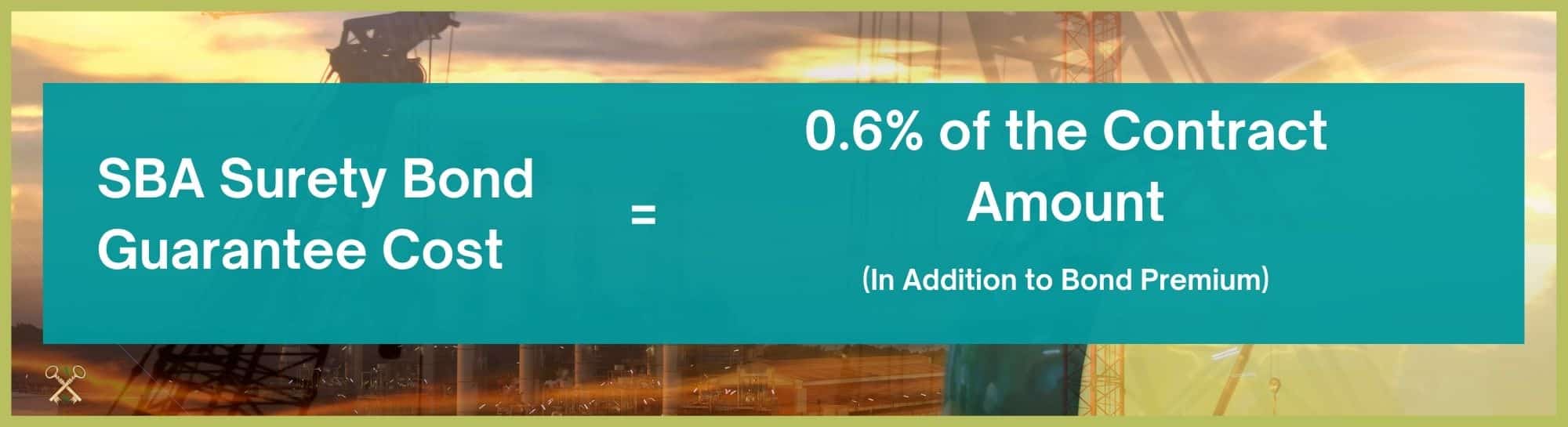

As discussed above, the SBA does not directly write these contract bonds. The contractor utilizing the program must pay both the Surety and the SBA. The SBA fee is currently 0.6% of the Bond Guarantee.

For example, for a $1 million performance Bond written with SBA support, the SBA would collect a $6,000 fee from the contractor. This fee must be paid upfront BEFORE the Bond is issued. Once this fee is paid, the broker will upload a copy of the receipt and wait for final approval to release the Bond(s).

It is also important for contractors to understand that the fee paid to the SBA is in addition to the Bond premium owed to the Surety Bond Company.

For example, if a Surety Bond company charges the contractor a 3% rate, the total cost would be 3.6% if they require SBA support. A $1 million contract would then have a total cost of $36,000.

In 2024, the SBA updated it bond program to be able to support single projects of $9 million, or single projects of $14 on some Federal Projects, if it certified by the Federal contracting officer. To qualify for this exception, the contractor must also be the Prime Contractor on the project.

Working Capital is a company’s current assets minus its current liabilities. Working Capital is a measure of a company’s ability to meet its short-term obligations. Because construction is such a cash intensive business, Working Capital is one of the most important underwriting considerations for most surety bond companies.

Unfortunately, small businesses may not always have enough Working Capital in the company to qualify for contract bonds. This is where the SBA Surety Bond Guarantee Program can really be helpful.

Unlike standard surety bond programs, the SBA views a company’s unused portion of their bank line of credit as if it were cash sitting in the company’s bank account. The SBA will even allow a contractor to set up a project specific line of credit to support a bond. This can be a big help when a contractor does not have enough working capital to qualify for a contract Bond in the standard market.

Typically, the SBA will support bond programs up to twenty times working capital. This may be more generous than many Surety Bond companies would write without SBA support.

The SBA Bond Guarantee allows surety bond companies to write contract bonds for contractors with negative Net Worth. A company’s net worth is simply its Total Assets minus its Total Liabilities. However, that is not the whole story for Contact Surety Bonds. Contract Bond underwriters use Analyzed Net Worth.

Analyzed Net Worth is the net worth of a company after an underwriter subtracts assets that are unlikely to be converted to cash. These are typically intangible assets, assets from related parties or assets that are unlikely to be collected.

Most Contract Bond companies will not write bonds for Contractors with negative Analyzed Net Worth, even if the contractor is profitable. There are two primary reasons for this.

First, contract Surety bonds are written with the assumption of no losses and indemnity. A contractor is expected to not cause a loss to a Surety, but if a loss happens, a contractor is expected to reimburse the Surety. A contractor with negative net worth will probably not have the financial means to reimburse the Surety.

The second reason is that contract Surety Bond companies often cannot get reinsurance when they write contractors with negative Analyzed Net worth. Reinsurance is important to surety bond companies. They purchase it so that they get protection from losses. If they cannot get reinsurance, many bond companies will simply not write Surety bonds.

Ownership transfers can be a challenge when it comes to obtaining Surety bonds. If bank debt is used by the new owner(s), it often creates Goodwill on the company’s balance sheet.

Contract Surety Bond companies do not count goodwill in their analysis because it is an intangible asset. This means that it cannot be easily converted to cash or used to complete a project.

By removing goodwill from their analysis but counting the debt, the new company often has negative Analyzed Net worth. As discussed above, this can be a problem for getting construction bonds in the standard market. However, the SBA Surety Bond Guarantee Program was created to help businesses in these scenarios.

The SBA will consider contractors who have had previous bankruptcies so long as those bankruptcies have been discharged. This can be a big advantage as most surety bond companies will not write contract bonds for contractors with recent bankruptcies. The contractor will need to show proof of discharge and this document will need to be uploaded in the SBA system.

Contractors will notice that the SBA requires more paperwork and forms than standard Surety Bond companies. This can be frustrating for contractors who are not used to the extra steps.

Surety bonds written with SBA support must be approved by both a Surety Bond underwriter and an SBA underwriter. The extra steps also take extra time. Contractors should be prepared for this extra time.

The SBA is meant for small businesses. The SBA determines if a business is small by their average annual receipts and NAIC class. They publish these standards on an annual basis. If a contractor is too big for the program, they simply cannot qualify for a SBA guarantee.

General contractors who subcontract most of their work may not be a fit for the SBA Surety Bond Guarantee Program. The SBA requires contractors to self-perform at least 15% of a contract to qualify. Generally, this does not include profit.

The SBA requirements are set. The SBA underwriters often do not have much flexibility. This streamlines the program, but contractors often want to negotiate terms when negotiations are not allowed with the SBA.

The SBA requires many items that a standard Surety Bond company would require to write contract bonds plus additional items.

The financial statements required depends on the size of the project being bonded.

The SBA will grant a one-time exception on the scope of financial statements which is beneficial for infrequent users. Those that need surety bonds often will need to get the appropriate scope of financial statements.

The principle will also need to provide internally prepared financial statements to the SBA every six months.

The SBA requires that contractors prepare and submit Work in Progress Reports (WIP) every 90 days. Although many contractors already prepare their own WIP reports, the SBA requires their own form to be completed. This Form 994F can be found here.

SBA Form 994 is the application for SBA assistance on a Surety Bond. This Form contains information on the principal’s business and background. It must be completed by the principal and submitted to the Bond broker before an SBA application can be started. Form 994 can be found here.

SBA Form 990 is required for each bond request. This Form has project specific information. It must be submitted to the Surety broker. SBA Form 990 can be found here.

SBA Form 912 provides information about the individual owners applying for a SBA guarantee. It is referred to as the statement of personal history. Form 912 is required from all individuals with 20% or more ownership in the company applying for the guarantee. You can find Form 912 here.

SBA Form 413 is a personal financial statement. It is required by anyone who is required to sign Form 912 and any others who may be personally indemnifying for the Bond.

The SBA will accept personal financial statements on other forms, however. Usually, owners have to prepare these for Surety Bond companies and lenders so they can use one they have already prepared. SBA Form 413 can be found here.

SBA Form 991 is only needed if a project has already started before when the Surety Bond is requested. The form requires the principal and obligee to sign the form saying there are no issues on the project to “the best of their knowledge.” Form 991 can be found here.

The SBA has a streamlined process for bonds $400,000 and less. This Quick Bond Program requires less time and paperwork than larger bonds. Another key component of the Quick Bond program is that there is no minimum credit score. This can be a great way for contractors who have had credit challenges to quickly obtain approval.

Not all businesses can qualify for SBA support based on their size. For most contractors, the size requirements are based on the average of the last three years of revenue. In general, most contractors who average less than $39,500,000 will qualify. Most subcontractor trades with less than $16,500,000 will also qualify. Businesses can check their eligibility here.

In some cases, Surety Bond underwriters may still ask for additional Surety tools to write bonds for a contractor. These tools could be in addition to SBA support. Surety Tools could include things such as funds control or collateral. Contractors need to carefully evaluate the pros and cons of these tools.

Like all contract surety bonds, the SBA Bond Guarantee Program requires indemnity. Both the company and the individual owners must indemnify to qualify for the program. Contractors can read more about indemnity here.

The SBA Surety Bond Guarantee Program is an excellent tool to help contractors obtain bonds that they would not otherwise qualify for. Contractors should work with a broker who is familiar with the program. Axcess Surety can help determine if the SBA Bond program is right for you. We will also evaluate alternatives. Contact us anytime. We are preferred SBA Surety Bond Guarantee Program Agent through our sister company.

A bid bond, performance bond or payment bond written by a surety bond company with the financial backing of the Small Business Administration.

$14 million on a Federal Prime contract if a federal contracting officer certifies SBA support is necessary. Otherwise, $9 million on other projects.

No. At this time the SBA will not support commercial surety bonds.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.