It can be difficult to distinguish the difference between bonds and insurance in construction. This is often because the same companies and brokers sell both products. However, these are very different products and contractors should understand the difference between the two. Learn more.

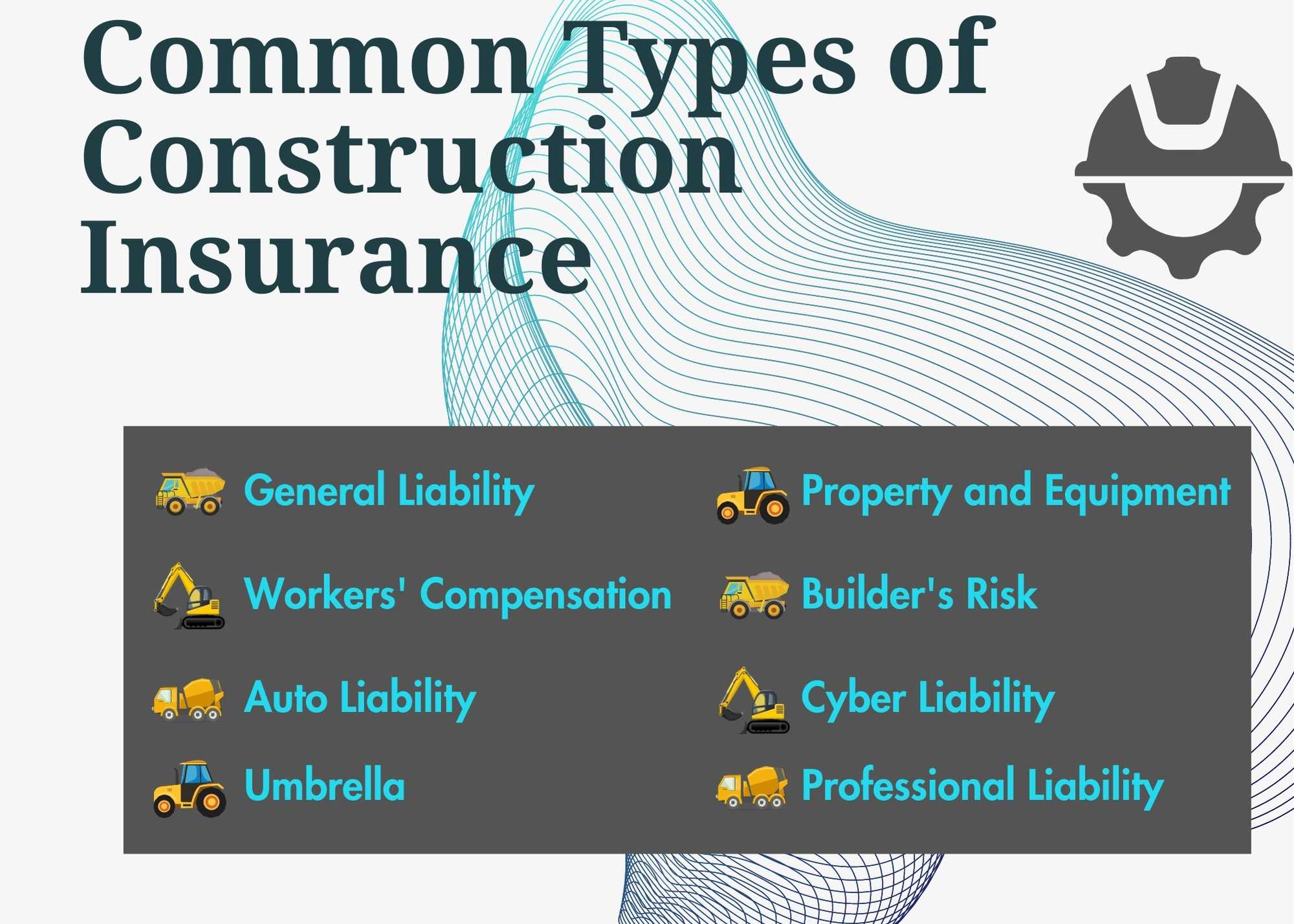

Most businesses need insurance. This is especially true in construction where injuries, and disputes are common. Contractors need several kinds of property and casualty insurance coverages including general liability insurance, workers compensation insurance, builder’s risk insurance, auto insurance, property insurance, umbrella insurance and possibly professional liability and cyber liability insurance. A more detailed explanation of these insurance coverages and what they do can be found below.

General Liability Insurance protects contractors from bodily injury and property damage caused by their operations. Supposed a contractor hits a utility line while digging, or a contractor’s scaffolding falls and injures a pedestrian. Each of these could be covered by the contractor’s general liability policy. Additionally, contractor’s need general liability in the event that their subcontractors do not carry adequate insurance.

Workers’ Compensation Insurance or “Work Comp” protects employees of the company from injuries or death sustained because of their employment duties. Work Comp insurance is mandated in most states if a contractor has employees. Work comp generally has two parts. The first part covers the employees’ injuries, and the second part compensates spouses and children for the employee’s loss of abilities.

Builder’s Risk Insurance protects a project while it is under construction. For example, a building may suffer a fire while it is being built. Because the project was under construction, it would generally not be covered by a standard property insurance coverage yet and the builder may be liable. This would potentially be covered by a Builder’s Risk policy.

Some contractors may need property Insurance to cover buildings that they own. A more common need for contractors is equipment coverage which is part of property insurance. Equipment Coverage is insurance that can cover both scheduled and unscheduled equipment.

Scheduled Equipment is equipment that is specifically valued and added to the schedule. Heavy machinery and equipment with large value should generally be scheduled.

Unscheduled Equipment is generally small tools and shop tools. Instead of providing a value for each piece of unscheduled equipment, contractors typically purchase an amount of insurance that covers all of it. An example may be $5,000 of unscheduled equipment with a maximum value of $500 for any one item. Any items that are more valuable should then be added to the equipment schedule.

Most Equipment Insurance policies also have coverage for rented equipment and equipment that may be borrowed from others. Contractors should always check to make sure they have enough limits when renting equipment though. It may be necessary to increase this coverage if a large piece of equipment is rented.

Most construction companies need commercial auto insurance coverage. This coverage protects the company’s vehicles, trucks, and sometimes mobile equipment from accidents that occur while driving.

Design is becoming more common in construction. Even if a contractor is not performing design-build work, they may be contributing to the design, making recommendations or providing advice that could open them up to liability. These types of lawsuits are generally excluded from the general liability insurance and need to be covered by a professional liability policy.

Cyber Liability Insurance protects contractors from electronic crimes. These could include hacking the contractor’s website and holding sensitive information for ransom. There was a time when contractors did not need to worry about cyber liability. However, construction is increasingly using more technology and sensitive information is increasingly shared via various construction software. More contractors are now realizing a need for cyber liability insurance.

An Umbrella Insurance Policy adds increased limits to the other policies. Generally, the umbrella insurance policy will add increased limits to the general liability, auto insurance and work comp policies. Contractors increasingly need larger limits to satisfy the contractual obligations that many owners and general contractors have. Therefore, many contractors are now required to purchase higher insurance limits through an umbrella insurance policy.

Now that we have covered what insurance contractors normally need, let’s look at what types of bonds contractors normally need. Construction Bonds generally refers to Bid Bonds, Performance Bonds and Payments Bonds that contractors need to bid on and guarantee work. Contracts often need license bonds as well, but these are not considered “Construction Bonds”.

Unlike construction insurance, construction bonds may not be required to operate the business. However, they are commonly required to obtain certain contracts. For example, all Federal Construction projects over $150,000 in value must be bonded under The Miller Act. Most other construction contracts involving public money have similar requirements. Additionally, many private construction contracts have similar requirements.

Bid Bonds guarantee that the bidding contractor will enter into a contract for their bid price if they are the winning bidder. Bid Bonds can also be a way to prequalify contractors. More can be read about bid bonds here.

Performance Bonds guarantee that a contractor will fulfill the contract according to the terms and contract price. Performance Bonds make sure a construction project gets completed and does not go over budget. The contractor bears the risk of cost overruns. More can be read about Performance Bonds here.

Payment Bonds guarantee that certain subcontractors and suppliers will be paid on the project. They help to keep the project free from Mechanic’s Liens. More can be read about Payment Bonds here.

As said above, these two products can be confusing but contractors may need both of them to obtain work. Below are other ways to better understand Bonds and Insurance in Construction.

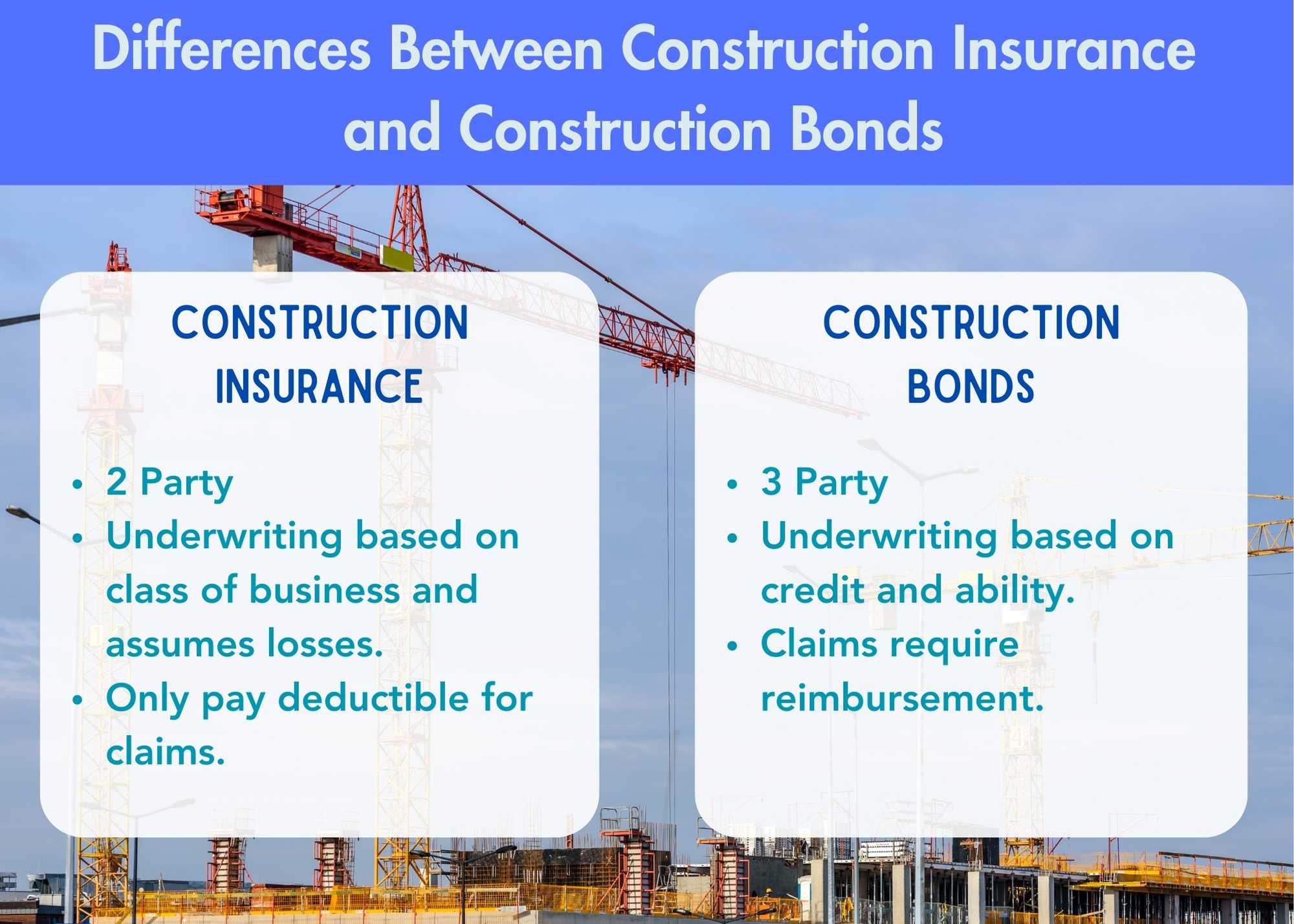

Insurance is a two party agreement for contractors. The contractor pays the insurance company a premium and in return, the insurance company promises to protect the contractor from claims and lawsuits brought against the contractor.

Conversely, construction bonds are a three party agreement. The contractor pays a premium to the bond company. In return, the surety bond company promises to protect a third party against a default by the contractor. This may sound minor, but it’s actually a major difference.

Summary Point: In construction insurance, the insurance company’s commitment is to the contractor. In construction bonds, the bond company’s commitment is to a third party.

Underwriting is very different for construction insurance and construction bonds. Construction insurance underwriting looks at the type of work that a contractor performs, their loss history and the historical losses for that type of business. The insurance underwriter then tries to determine the amount of losses that the contractor will have and charges a price for those losses along with costs and profit for the insurance company.

Conversely, construction bond underwriting involves looking at the credit, character and capacity of the contractor known as the 3Cs. This underwriting looks at the contractor’s financial strength and abilities to complete the work. The underwriter assumes the contractor will not suffer any losses or they would not write construction bonds for the contractor.

Summary Point: Construction Insurance assumes a certain amount of losses for the contractor and those losses are included in the price. Construction Bonds assumes no losses.

Claims happen in construction insurance frequently. The insurance carrier investigates the claim and pays for damages. The contractor is typically responsible for a deductible and the insurance company handles the rest.

In Construction Bonds, claims are rare. The bond company will also investigate claims. If the construction bond company pays a claim, they will then seek to be reimbursed by the contractor under the indemnity agreement. A construction bond claim could easily cause a contractor to go bankrupt.

Summary Point: Claims are common in construction insurance. The contractor is only responsible for a deductible in most cases. In construction bonds, claims are uncommon and the contractor will be asked to reimburse the bond company for the entire amount of the claim.

With several major differences, why is there so much confusion between construction insurance and construction bonds?

One of the major reasons contractors get confused is because both construction insurance and construction bonds are governed by the same licensing requirements. Usually, a company only needs a property and casualty insurance license to sell both products. This is really a failure of the government. Most property casualty insurance agents and brokers know very little about construction bonds. Similarly, most construction bonds experts are not experts in construction insurance. However, in order to make more money, brokers typically try to sell both products to contractors. Not only does this create confusion, it is a disservice to the contractor.

Just as the same brokers and agents write both construction insurance and construction bonds, the insurance carriers are often the same as the surety bond companies and vice versa. There are several reasons for this. Insurance companies have found construction bonds to be a profit center over the years and a good way to make a return on their capital. It is also easy to market to agents and brokers by selling both products.

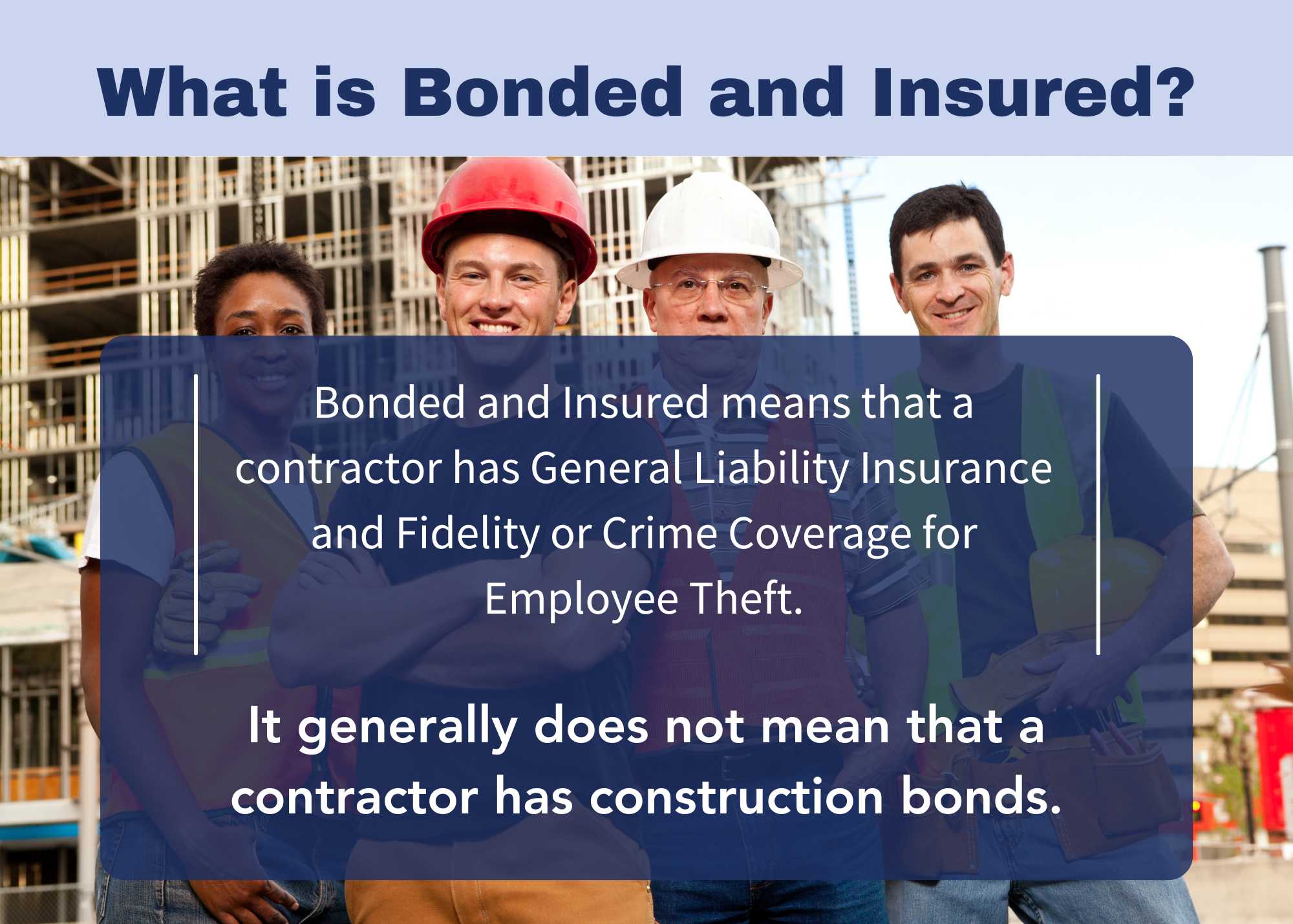

Another reason for confusion is the old term “Bonded and Insured”. In times past, the term “Bonded and Insured” was important to customers. The phrase meant that the contractor had insurance against damages and was “bonded” against acts of theft against the customer. For example, an electrical contractor needed to have a fidelity bond in place to protect against his employees stealing a customer’s property while working there. Today, fidelity bonds still exist, but many customers have coverage for crime and theft included in their insurance policy. The term should not be understood as meaning to have insurance and construction bonds, although it is commonly applied in this manner.

Bond versus insurance in construction is an important topic for all contractors to understand. Almost all contractors need construction insurance and most commercial contractors will also need construction bonds. These two products have very different meanings and purposes and contractors will need to understand what is required before entering into a contract or bidding on a project.

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.