Notary Bonds are a requirement to be an appointed Notary Public in most states. Learn more about what these notary bonds guarantee, who they protect, how to get one and what they cost.

A Notary Public is someone appointed by a state to give an impartial witness or acknowledgement of the execution of legal documents. Notaries are responsible for verifying that the person signing documents is the actual individual and in some cases, appeared physically in front of them. Notaries must generally keep a journal of all documents they notarized including the individuals, dates and times.

Most states require that the individual apply for the position. Usually, the person must pass a background check showing that they have not been convicted of any crimes involving dishonesty. In some states, notary applicants must also pass an exam showing that they know the laws and requirements of a notary.

Most states require a notary to keep a Notary Journal of all transactions. It is common to require the notary to document dates, names of signing pirates and the type of transaction notarized. Many states require notaries to keep these journals for a period of 10 years or longer and require the notary to provide the journal for examination upon request by the state.

It is common in many states to have two different types of notary appointments, including regular notaries and electronic notaries.

Electronic Notaries are notaries that can notarize documents online or over the internet. Unlike traditional notary services, individuals do not normally have to appear in person to have documents witnessed by an online notary. However, other types of verification are required.

Electronic Notaries must take different training and pass different licensing requirements in many states. However, some states still maintain the same requirements for both licenses.

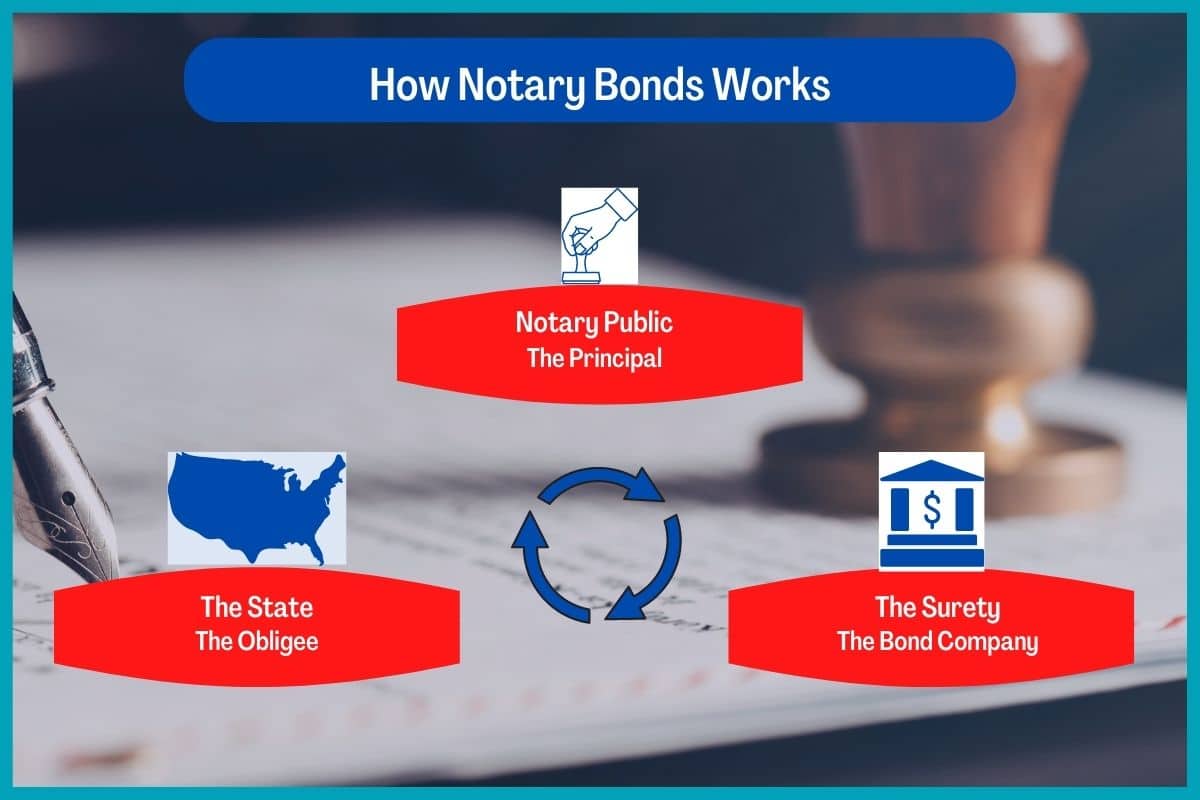

As part of the licensing and appointment process, most states require that notaries obtain a notary bond. The amounts of these notary bonds vary by state and range from $1,000 to $25,000.

Notary Bonds protect the users of the notary’s services against mistakes, errors and negligence made by the notary in performing their official duties. If a notary’s mistake negatively impacts a party, they can make a claim against the notary bond. However, the bond amount is the most the Notary Bond Company must pay. This is referred to as the Bond’s Penal Sum. Notary Bonds are considered a type of License Bond.

Most notary bonds are instant issue with no credit underwriting. Notaries can go online and purchase a bond instantly with very little information. Visit our State Surety Bond Page to purchase a state specific notary bond.

The cost depends on the amount of the notary bond. However, Notary Bonds are very inexpensive. Most Notary Bonds cost about $10 - $20 per year of protection.

Notary Bonds are generally written for the same length of time as the Notary's appointment in each state. Although this varies by state, a 4-year term is common.

Usually, the best way to make a claim against the notary bond is to contact the Secretary of State in the jurisdiction that the notary services took place. The State can get in contact with the surety bond company. Make sure to have the notary’s name, date services were rendered and a description of the problem.

Claims against notary bonds are very rare. However, notary bonds require the notary to sign an indemnity agreement. This means that if the surety bond company pays a valid claim, they can seek reimbursement from the notary. Notaries can read more about indemnity here.

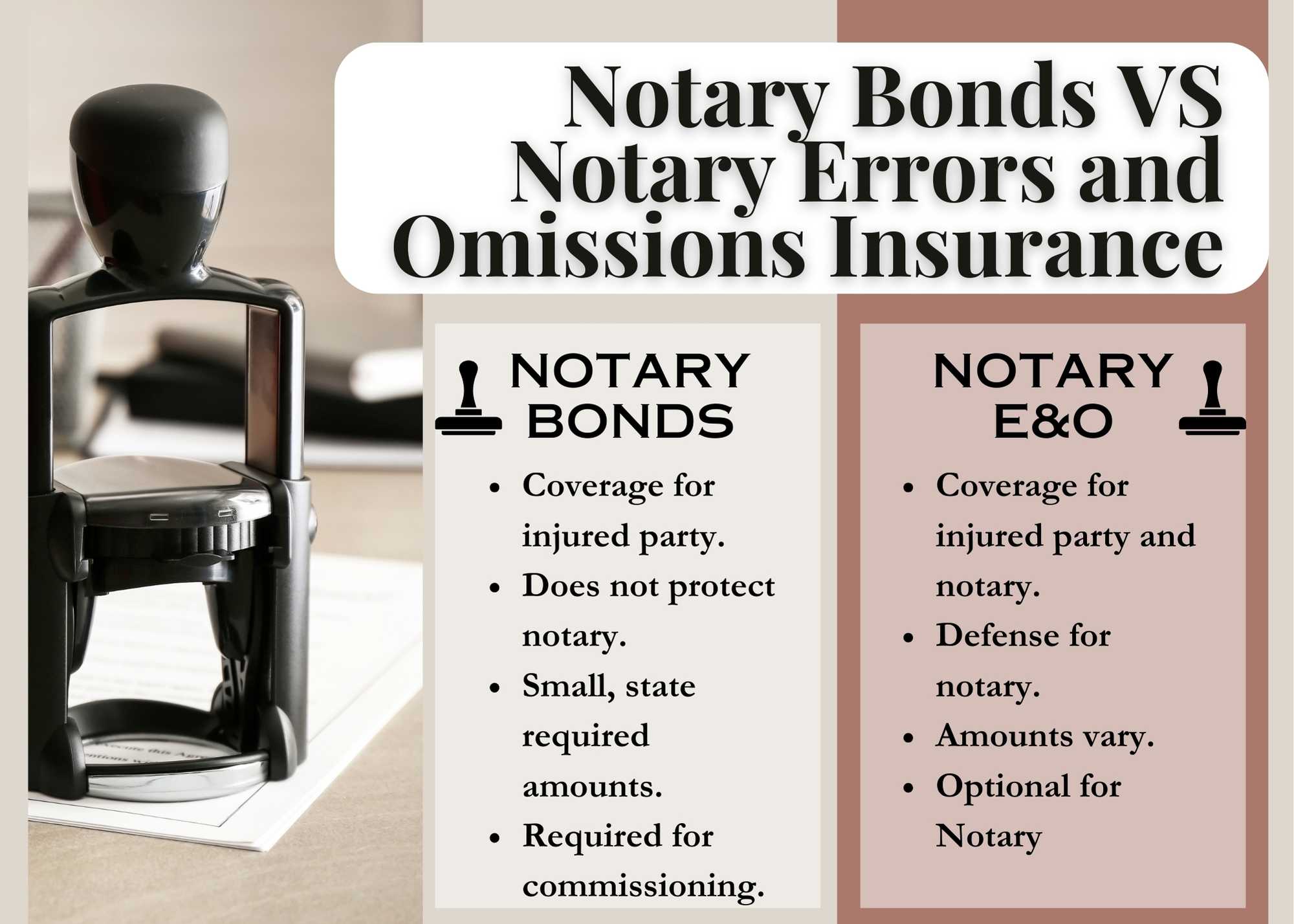

Errors and Omissions (E&O) insurance is a type of insurance that notary publics may choose to carry in addition to their notary bonds. E&O insurance provides an extra protection in the event that a notary makes a mistake in the notarization process. While a notary bond is designed to protect the party using the notary service, notary E&O insurance protects the notary from additional lawsuits that could be brought against the notary.

Notary E&O insurance usually provides a limit of coverage. More importantly, it can include coverage for defense costs that the notary may be responsible for without the coverage. This insurance is usually voluntary but can offer significant benefits to the notary public. While small limits are sometime included with a notary bond, it is often wise to purchase additional limits. Notary E&O insurance is usually very inexpensive.

Notary Bonds are required by most states in order to be appointed as a notary. These bonds are very easy to get and inexpensive. However, notaries should be careful to avoid claims against these bonds. Notaries can learn more about surety bonds on our Surety Bond page. Contact Axcess Surety anytime for all your Notary Bond and other Surety Bond needs.

Find State Specific Notary Bond Information by Clicking on the State Below.

Nebraska

New Hampshire

New Jersey

New Mexico

New York

North Carolina

North Dakota

Ohio

Oregon

Rhode Island

South Carolina

South Dakota

Tennessee

Utah

Vermont

West Virginia

Wyoming

Axcess Surety is the premier provider of surety bonds nationally. We work individuals and businesses across the country to provide the best surety bond programs at the best price.